Market Segment

March 23, 2023

HRC Imports Gain Appeal Given Rising US Sheet Tags

Written by David Schollaert

The appeal for imports of hot-rolled coil (HRC) continues to grow as US prices move higher in response to repeated mill tag hikes. The price advantage domestic HRC had enjoyed over offshore just last month has swung negative at an accelerated rate, according to SMU’s latest foreign vs. domestic price analysis.

![]() The most recent pricing notice – issued by Cleveland-Cliffs nearly two weeks ago, targeting a base price of $1,200 per ton ($60 per cwt) for HRC – is still making its way into the domestic market, albeit at a slightly slower pace than in recent weeks.

The most recent pricing notice – issued by Cleveland-Cliffs nearly two weeks ago, targeting a base price of $1,200 per ton ($60 per cwt) for HRC – is still making its way into the domestic market, albeit at a slightly slower pace than in recent weeks.

US HRC had held a price advantage over foreign hot band for 16 consecutive weeks. But that trend has turned completely negative over the past five weeks as domestic HRC prices continue to rise at a much faster clip than tags abroad.

Domestic hot band is now nearly 23% more expensive than foreign material. That premium is wider than last week, when domestic HRC was ~21% more costly than imported product.

US prices had been cheaper than foreign prices for the three regions we follow (Asia, Italy, and Germany) since the beginning of November after adding freight costs, trader margins, and applicable tariffs. That changed with US HRC prices rising $335 per ton since the beginning of February. US prices have since shot up by $265 per ton thus far in March.

Domestic HRC held, on average, an $18-per-ton advantage over imported hot band as recently as mid-February. That has flipped to a $255-per-ton disadvantage this week as US prices have continued to trek higher.

SMU uses the following calculation to identify the theoretical spread between foreign HRC prices (delivered to US ports) and domestic HRC prices (FOB domestic mills): Our analysis compares the SMU US HRC weekly index to the CRU HRC weekly indices for Germany, Italy, and eastern and south-eastern Asian ports. This is only a theoretical calculation because costs to import can vary greatly, influencing the true market spread.

In consideration of freight costs, handling, and trader margin, we add $90 per ton to all foreign prices to provide an approximate CIF US ports price to compare to the SMU domestic HRC price. Buyers should use our $90-per-ton figure as a benchmark and adjust up or down based on their own shipping and handling costs. If you import steel and want to share your thoughts on these costs, we welcome your insight at david@steelmarketupdate.com.

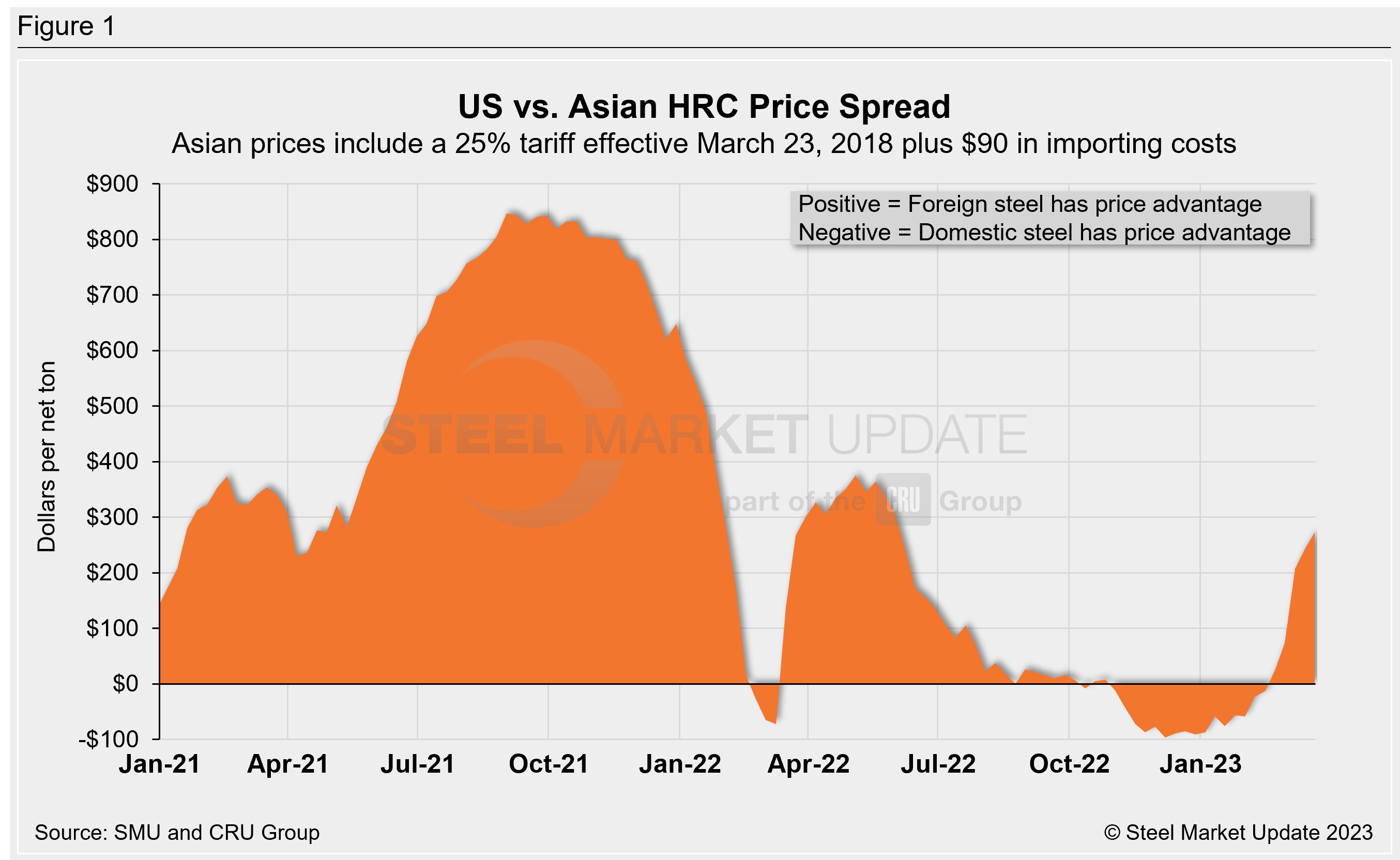

Asian Hot-Rolled Coil (East and Southeast Asian Ports)

As of Thursday, March 23, the CRU Asian HRC price decreased by $5 per ton from a week ago to $621 per net ton ($685 per metric ton), but was up $14 per ton from levels one month prior. Adding a 25% tariff, and $90 per ton in estimated import costs, the delivered price of Asian HRC to the US is $867 per ton. The latest SMU hot-rolled average is $1,140 per ton, up $25 per ton from our previous price update, and up $265 per ton compared to our price one month ago.

US-produced HRC is now theoretically $273 per ton more costly than steel imported from Asia. This is a reversal from just six weeks ago, when domestic HRC had a $13-per-ton advantage over HRC from Asian markets.

Just two months ago, we saw a $76-per-ton spread advantage for US HRC, among the biggest price advantage domestic HRC has had over Asian HRC in recent years.

The widest price advantage for Asian hot band was recorded nearly 16 months ago: $847 per ton in September 2021.

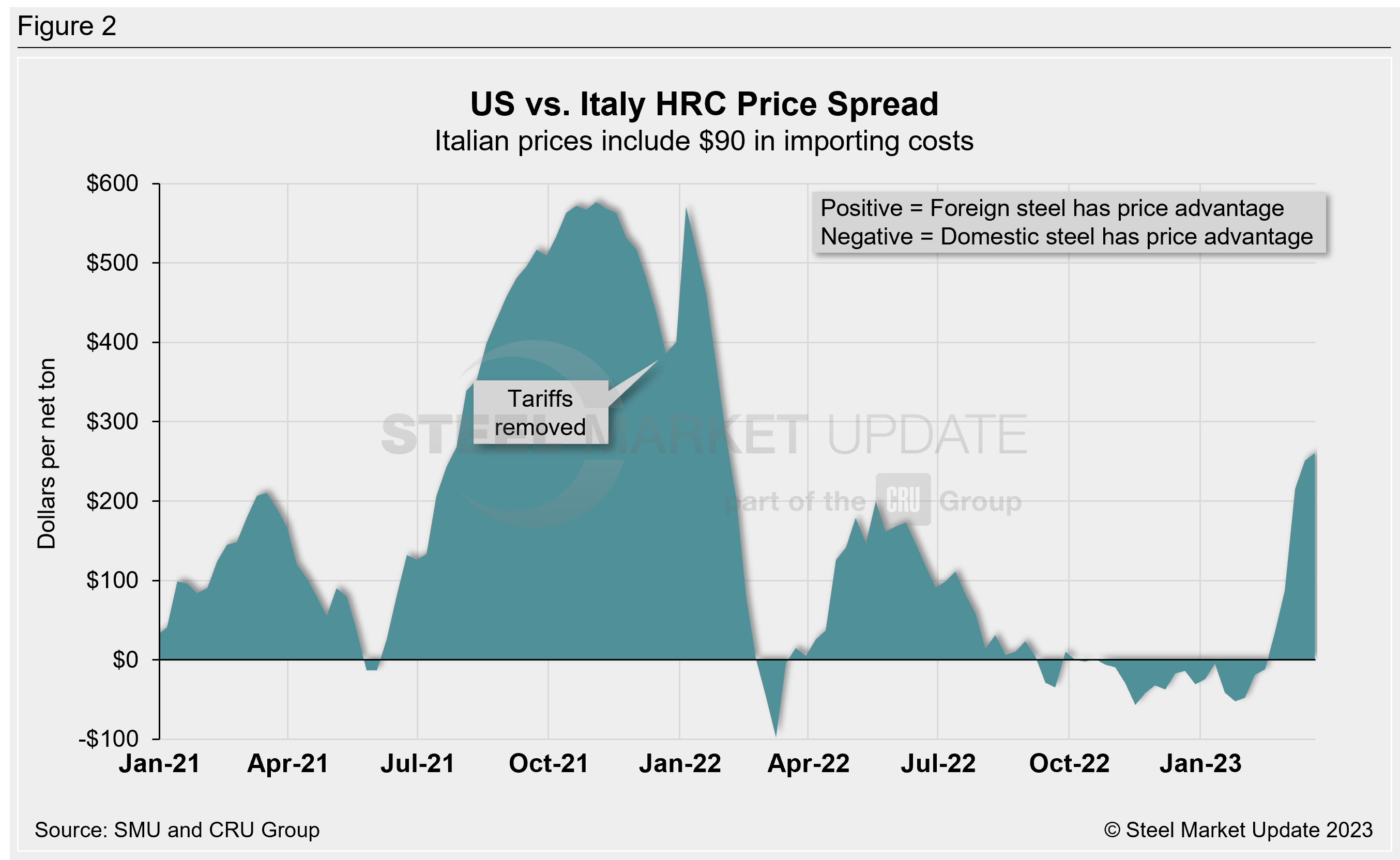

Italian Hot-Rolled Coil

Italian HRC prices increased by $16 per ton WoW to $790 per net ton ($870 per metric ton) this week, and are $40 per ton higher month-on-month (MoM). After adding import costs, the delivered price of Italian HRC is approximately $880 per ton.

Domestic HRC is now theoretically $260 per ton more expensive than imported Italian HRC. That spread is up $9 per ton WoW and represents a nearly $264-per-ton reversal compared to five weeks ago when US HRC was $12 per ton cheaper than Italian product. As recent as Jan. 25, US HRC was in theory $52 per ton cheaper than imported Italian hot band.

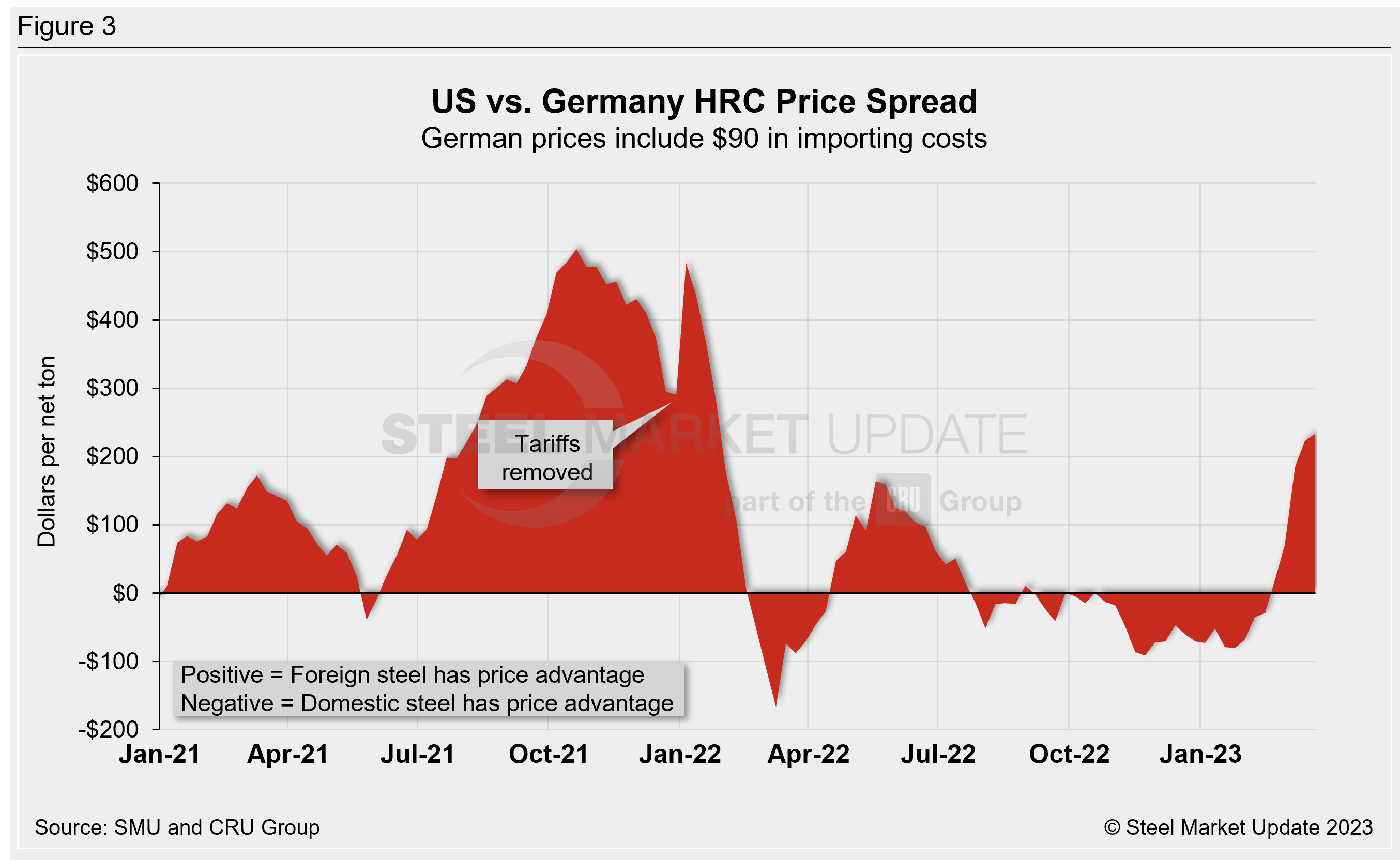

German Hot-Rolled Coil

CRU’s latest German HRC price rose by just $15 per ton WoW to $817 per net ton ($900 per metric ton) and is up $50 per ton MoM. After adding import costs, the delivered price of German HRC is roughly $907 per ton.

Domestic HRC is now theoretically $233 per ton more expensive than imported German HRC. That’s a swing of $262 per ton given that US hot band held a $29-per-ton advantage over domestic hot band in mid-February.

US HRC had held a price advantage over German product for all but three weeks since late July.

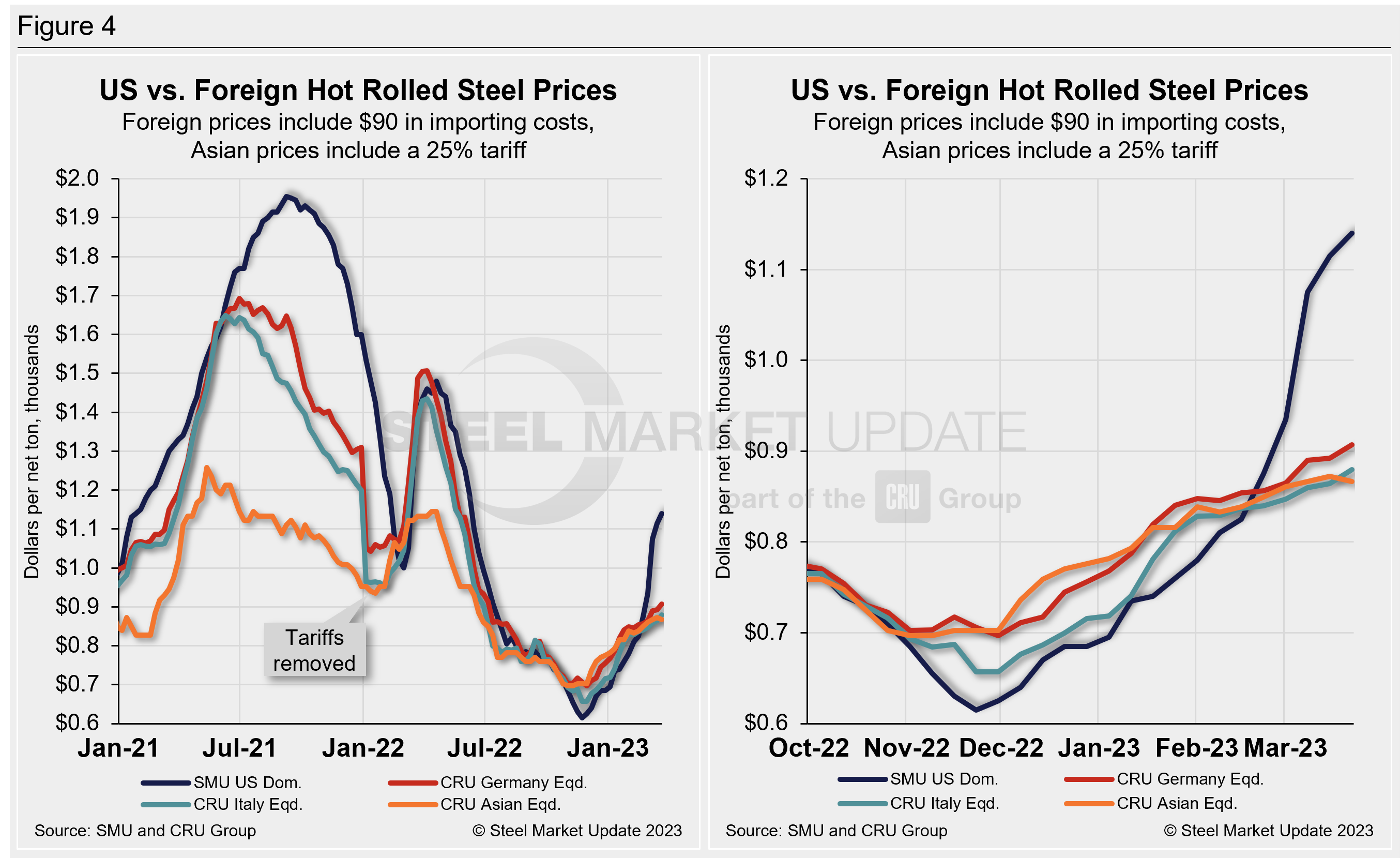

Figure 4 compares all four price indices and highlights the effective date of the tariffs. The chart on the left shows historical variation from Jan. 1, 2021, through present. The chart on the right zooms in to highlight the recent decoupling of US and offshore HRC prices.

Notes: Freight is an important consideration in deciding whether to import foreign steel or buy from a domestic mill. Domestic prices are referenced as FOB the producing mill, while foreign prices are CIF the port (Houston, NOLA, Savannah, Los Angeles, Camden, etc.). Inland freight, from either a domestic mill or from the port, can dramatically impact the competitiveness of both domestic and foreign steel. It’s also important to factor in lead times. In most markets, domestic steel will deliver more quickly than foreign steel.

Effective Jan. 1, 2022, the traditional Section 232 tariff no longer applies to most imports from the European Union. it has been replaced by a tariff rate quota (TRQ). Therefore, the German and Italian price comparisons in this analysis no longer include a 25% tariff. SMU still includes the 25% Section 232 tariff on foreign prices from other countries. We do not include any antidumping (AD) or countervailing duties (CVD) in this analysis.

By David Schollaert, david@steelmarketupdate.com