Analysis

March 3, 2024

Final thoughts

Written by Michael Cowden

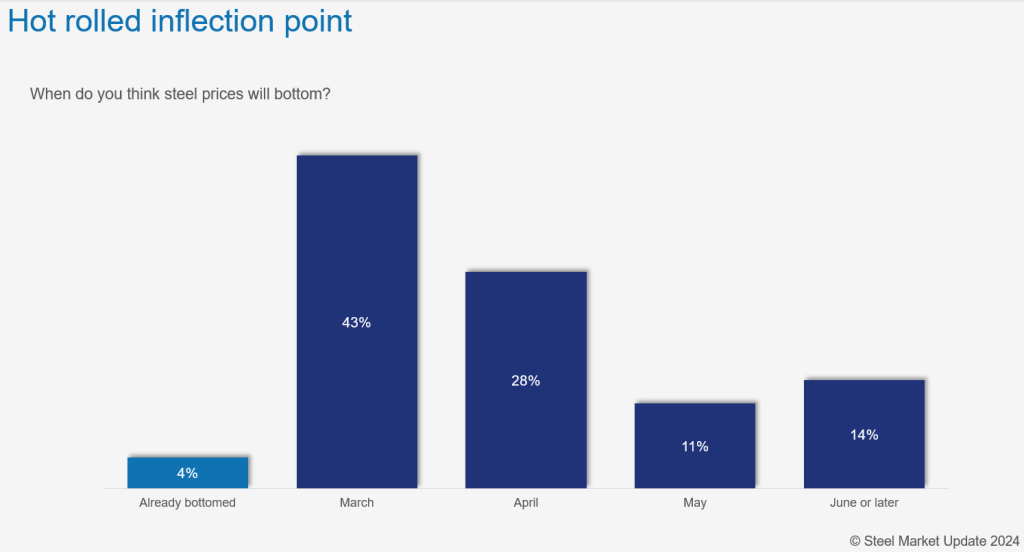

A clear consensus has emerged among respondents to SMU’s latest steel market survey that hot-rolled (HR) coil prices will bottom this month or in April.

Is a sheet price bottom near(ish)?

Seventy-five percent of respondents to our latest survey think that prices will find a floor before May as the chart below shows:

Here is what some of them had to say:

“You will wait as long as possible if you are saving a few $1,000 per truckload each week by waiting.”

“With soft scrap market, solid stock levels, and demand that is OK, it appears we will see weakening for a few more weeks.”

“I expect a bottom in March. Prices are coming down too quickly to continue to.”

“Prices dropping very quickly. They will hit bottom soon if this pace continues.”

“There is good demand and less foreign coming in than people think.”

“They have not yet bottomed out, but should by mid-March, followed by a slight increase in April when inventories are replenished.”

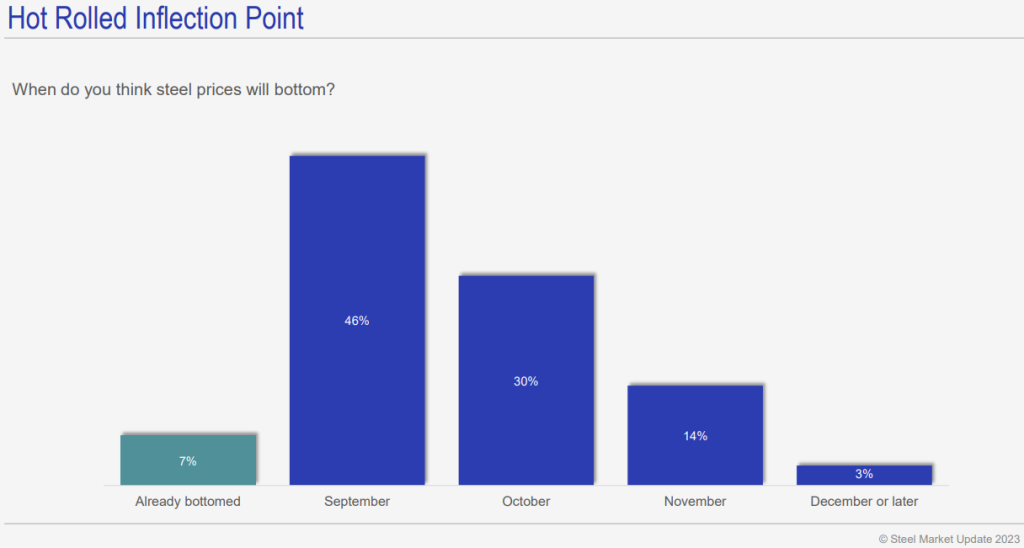

Some of you have asked me whether our survey respondents are good at predicting market inflection points.

You could make the case that they’re pretty good at predicting things over the short-term. Look at this survey result from late August 2023.

Seventy-six percent predicted that prices would bottom in September or October. As it turned out, prices bottomed out in late September, and so that was the right call.

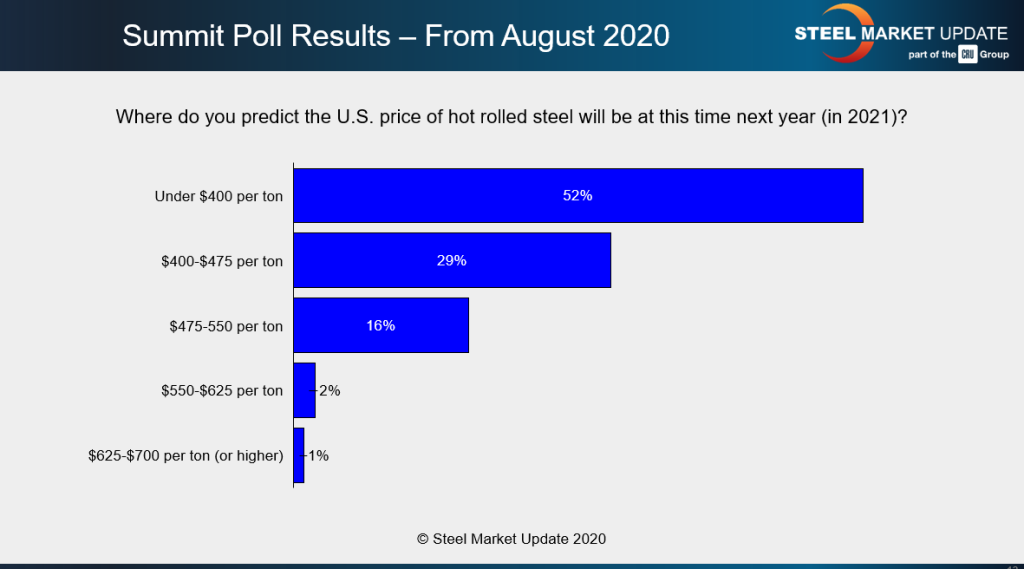

What people aren’t so great at is predicting long-term moves. Here is one from (virtual) Steel Summit in August 2020:

HR prices at the time were in the pandemic-induced $400s per short ton (st). Few saw the snapback in demand coming. And no one was anywhere close to predicting that HR prices would be closer to $2000/st in August 2021.

So, back to the current market. Assuming that survey respondents are reasonably good at predicting short-term price cycles, what are some reasons that might support a March/April bottom?

Spring outages

Several of you have noted in the survey or in individual calls or emails to me that there are a raft of roughly week-long maintenance outages coming up this month and next at EAF sheet mills. Others have noted that an integrated mill is going through a series of “rolling” week-long outages at its mills.

Similar routine outages last fall contributed to a sheet price spike. But when supply is abundant and lead times contracting – as we saw in January when Algoma had a major outage – the market tends to shake off lost production, even when it’s unplanned.

Could we see something in between those two extremes this spring – with outages helping the market to establish a floor but without a price spike like we saw last fall? I think that’s worth considering.

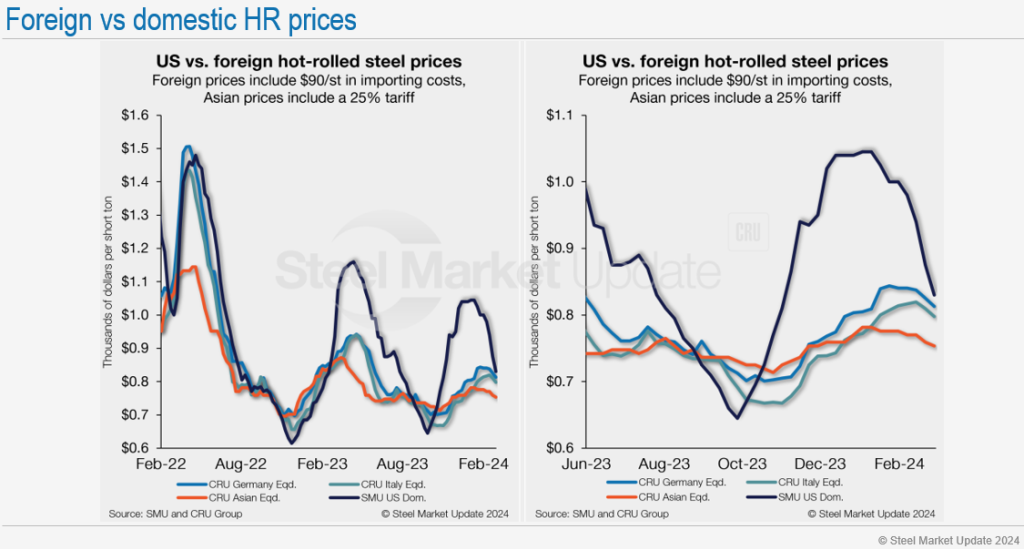

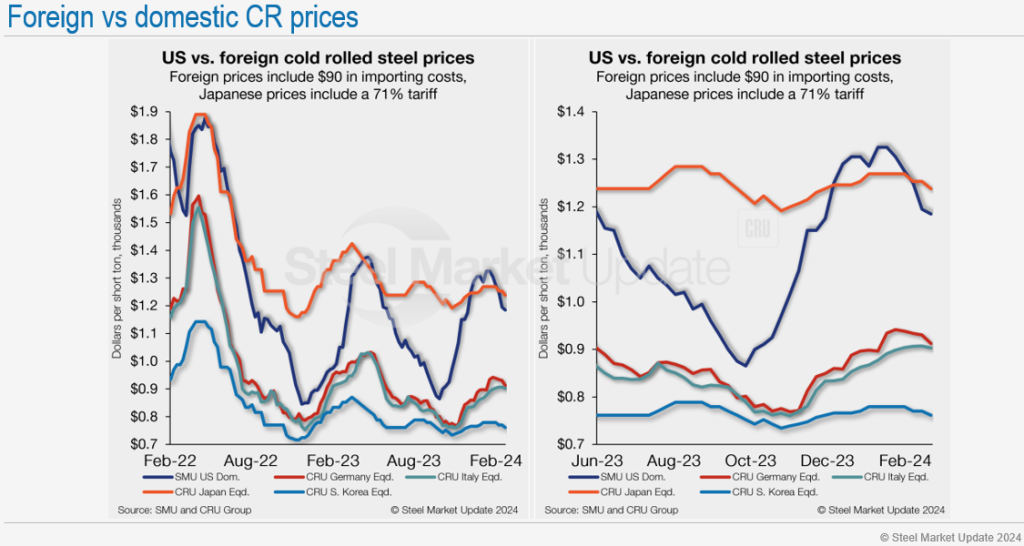

A tale of two import markets: HR vs CR/coated

Many of you also expect US prices to stabilize on lower imports in the months ahead. The chart below goes a long way toward explaining why people expect import volumes to decline:

Sheet imports reached a 16-month high of nearly 900,000 metric tons (mt) in January, according to preliminary data from the US Commerce Department. That was their highest point since nearly 975,000 mt in August 2022.

February data are not complete yet. But it appears figures for last month – while not low – will be below January volumes. That said, a lot might depend on which market you’re in. If current trends hold, we’ll see lower HR import volumes in February vs. January.

That’s not the case for coated products. The chart below helps explain why that’s so:

That’s cold-rolled prices. I’m also using it as a rough proxy for the difference between US and foreign galv and Galvalume base prices.

As I noted, February data are not complete yet. But coated import volumes are already higher in February than in January. So, while HR imports might have peaked, coated import volumes are still climbing.

That makes sense. It roughly matches what we often see on the price side – namely, that cold-rolled and coated products tend to follow HR lower on a bit of a lag.

Let’s also remember that the spread between domestic HR and domestic CR/galv base prices is really, really wide. That spread in the US in recent years had been approximately $200 per short ton – which was already higher than the HR/CR spread abroad. And with HR prices declining faster than prices for tandem products in January and February, that spread has exploded to $300 per ton.

But that gap could close quickly. New domestic coating capacity is ramping up or soon will be. And some of you tell me that you’re getting competitive quotes on galv for as little as a few truckloads. And/or you tell me that you’ve had mills call you, unsolicited, to see if you might be interested in buying.

Long-term, it’s good that the US might have a more robust and competitive base of flat-rolled steel suppliers. Short-term, unsolicited calls typically mean that prices will continue to fall.

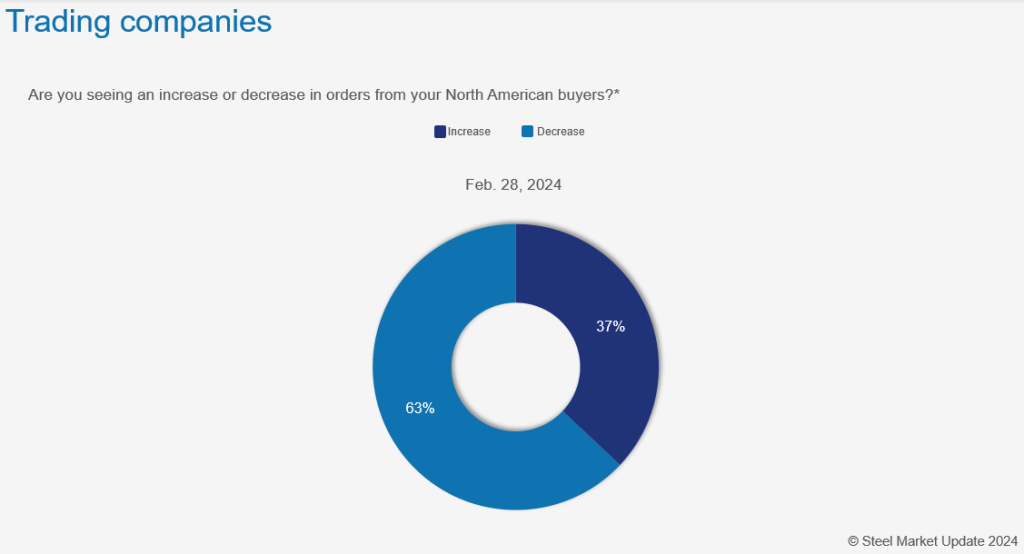

Lower summer import volumes

That might explain why trader sources say that domestic buyers are decreasing import orders:

“The (import) price is discounted from domestic mills. But people are afraid of where the market will be in six months,” one survey respondent said.

I’ve heard similar sentiment expressed by other market participants. Basically, that import volumes, while high now, could taper off significantly this summer.

All of that supports the idea that prices could bottom in late March or April – or as lead times stretch into May.

Demand is still stable, right?

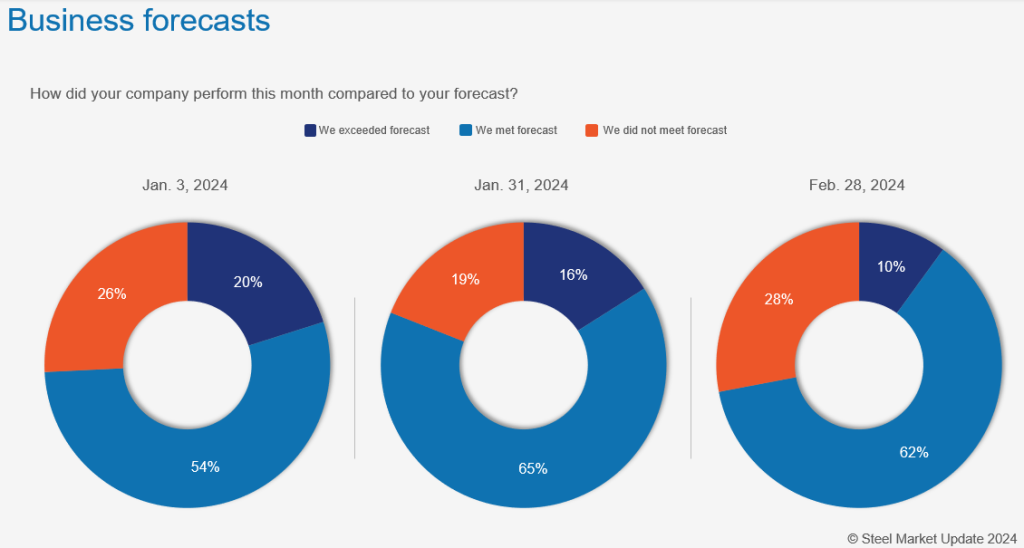

If there is one fly in the ointment, it’s this: We’ve seen a little bit of an uptick recently in the number of people who tell us they are not meeting forecast:

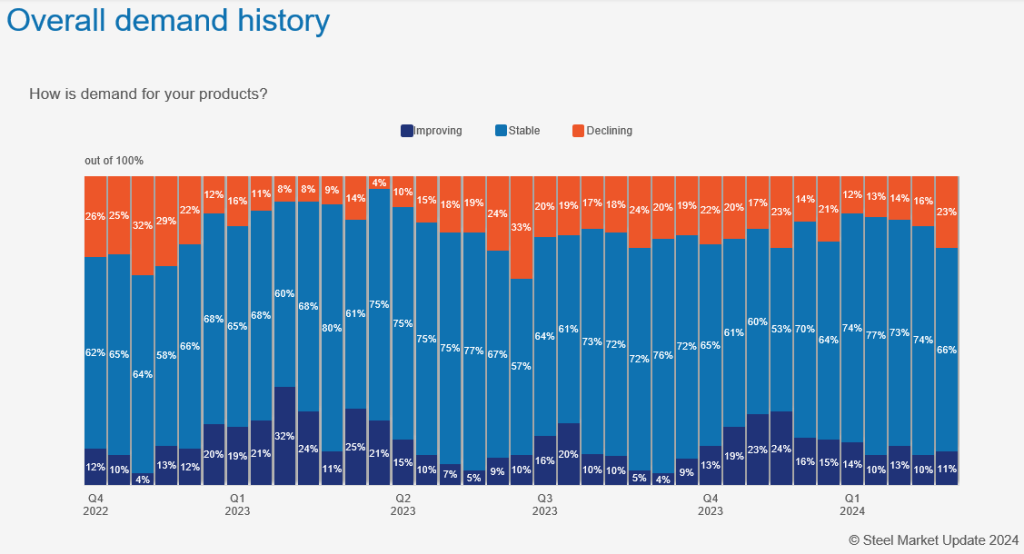

We saw a similar result when we asked people about overall demand:

I wouldn’t read too much into one survey result. But we’ve also seen a mild uptick in bearish comments lately. Here are some examples:

“We have faced a challenging month in securing orders, so we will not meet the forecasted number.”

“We’re seeing demand fall off and orders delayed.”

“February definitely slowed down for us.”

To be clear, most people continue to say that demand is good and that they’re meeting forecast. Some noted that activity remains brisk despite falling spot prices or that construction is starting to pick up in earnest.

That said, I’d keep an eye on responses about business forecasts and overall demand in our next few surveys. If things go back to normal, then I think predictions about a March/April bottom make sense. If we see any sustained signs of demand slipping, then it might be a little while longer until a bottom is reached.

That’s my two cents. What are you seeing out there?

SMU Community Chat

Worthington Steel President and CEO Geoff Gilmore will be the featured speaker on the next SMU Community Chat on Wednesday, March 6, at 11 am ET.

The live webinar is free for anyone to attend. A recording is available only to SMU subscribers. You can register here.

We’ll talk about how the first few months of operating Worthington Steel as a standalone company have gone. We’ll also discuss the current steel market and the outlook for the key end markets the company serves. And we’ll take your questions too, so think of some good ones and bring them to the Q&A on Wednesday!