Market Data

June 6, 2024

SMU survey: Summer slowdown brings short to normal mill lead times

Written by David Schollaert & Laura Miller

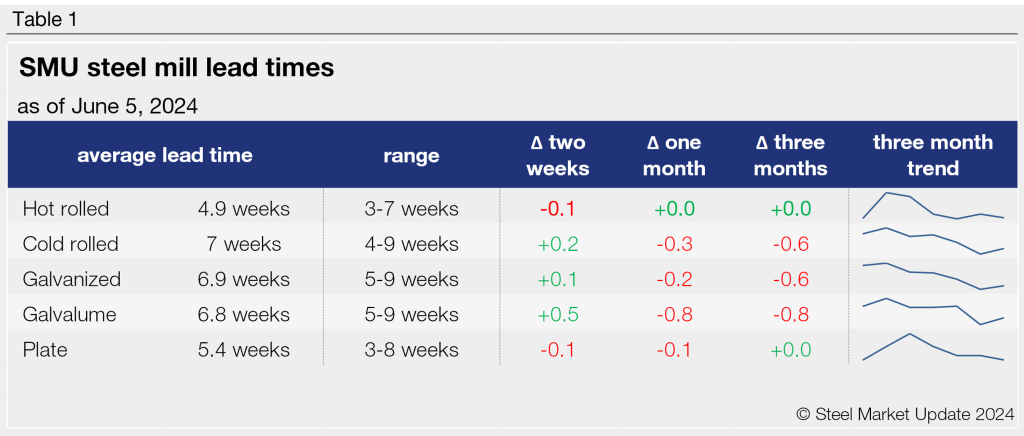

Movements in steel mill lead times were mixed this week, according to our latest steel buyers’ survey results. Service centers and manufacturers reported short to average production times, little changed from our last report.

The average lead times for hot-rolled (HR) coil and plate contracted slightly, while lead times for cold-rolled (CR) and coated products ticked up. Average HR lead times have been hovering close to five weeks since February.

Table 1 below details current lead times.

The majority of service centers and manufacturing companies we surveyed categorized current production times as normal (47%) or shorter than normal (47%).

“Lead times overall are normal, but longer than expected given the softness in the market,” one service center buyer commented.

As to where lead times are headed in a couple of months, more than two-thirds of respondents anticipate them to be flat two months from now. Still, 20% believe they will be extending and 13% contracting.

Multiple buyers cited weak demand and additional capacity coming online as reasons for flat or contracting production times.

As one buyer put it: “Demand is too weak, and the summer doldrums are upon us. Mill lead times won’t get any longer, especially if new capacity is going to be added.”

However, another purchaser said they “expect the mills to take action to balance supply (take it down), which will push out lead times.”

Still, another service center buyer noted that demand must eventually improve, which will lead to “healthier lead times.”

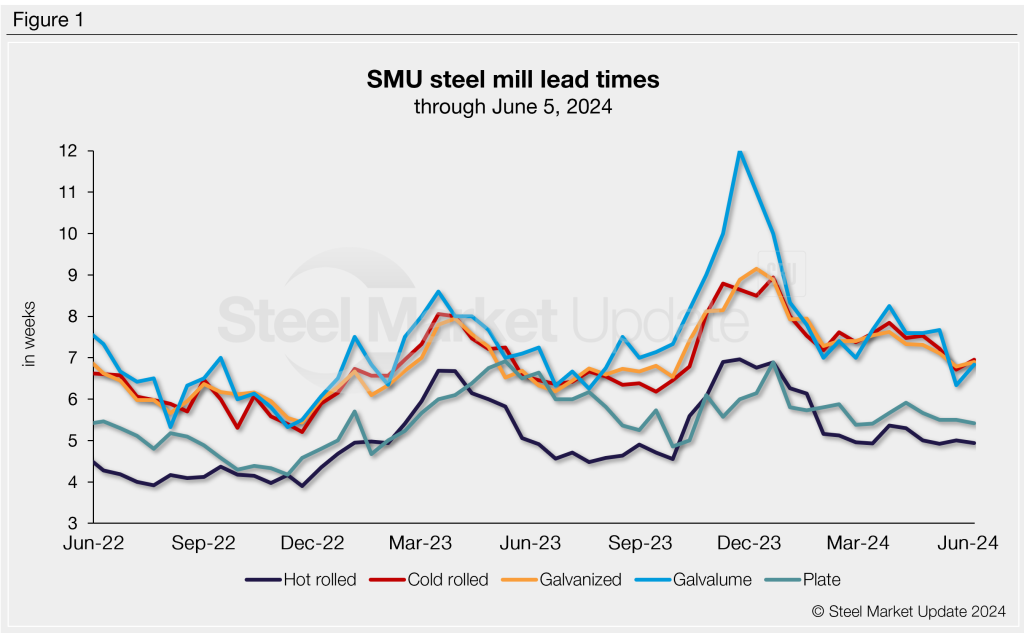

Figure 1 below tracks lead times for each product over the past two years.

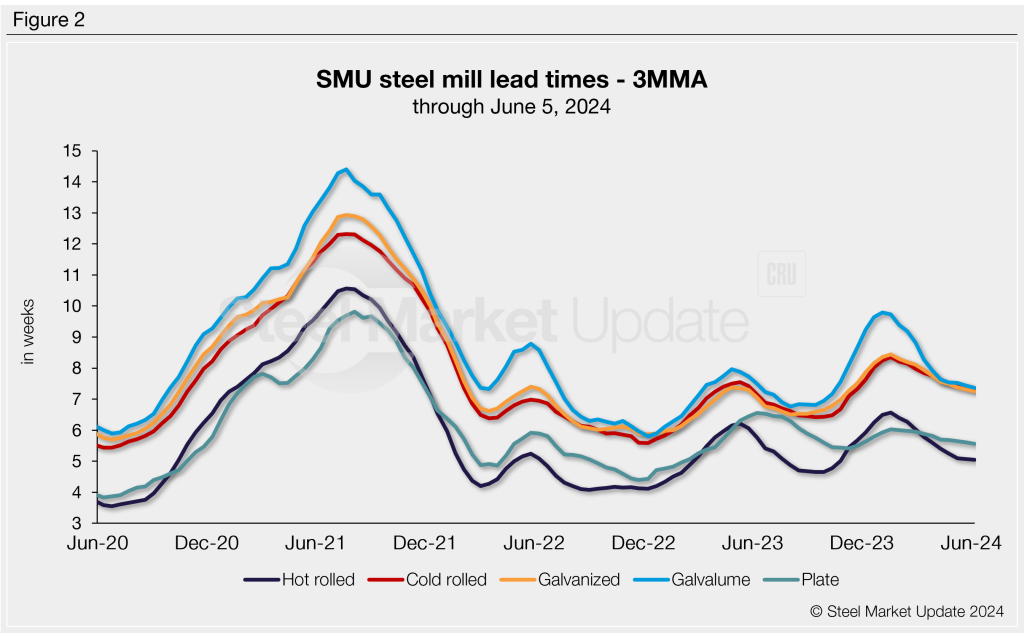

3MMA lead times

Looking at the three-month moving averages (3MMA) of lead times can smooth out the variability seen in our biweekly readings.

The 3MMAs show that lead times for sheet and plate products peaked in early to mid-January and have been trending lower since.

This week’s 3MMAs, at 5.05 weeks for HR coil, 7.34 weeks for CR coil, 7.25 weeks for galvanized sheet, 7.37 weeks for Galvalume sheet, and 5.56 weeks for plate, all contracted from two weeks prior.

Figure 2 highlights how lead times have been trending over the past four years.

Look for SMU’s next lead time update on Thursday, June 20.

Note: These lead times are based on the average from manufacturers and steel service centers participating in this week’s SMU market trends analysis survey. SMU measures lead times as the time it takes from when an order is placed with the mill to when it is processed and ready for shipping, not including delivery time to the buyer. Our lead times do not predict what any individual may get from any specific mill supplier. Look to your mill rep for actual lead times. To see an interactive history of our steel mill lead times data, visit our website. If you’d like to participate in our survey, contact us at info@steelmarketupdate.com.

David Schollaert

Read more from David Schollaert