Prices

June 25, 2025

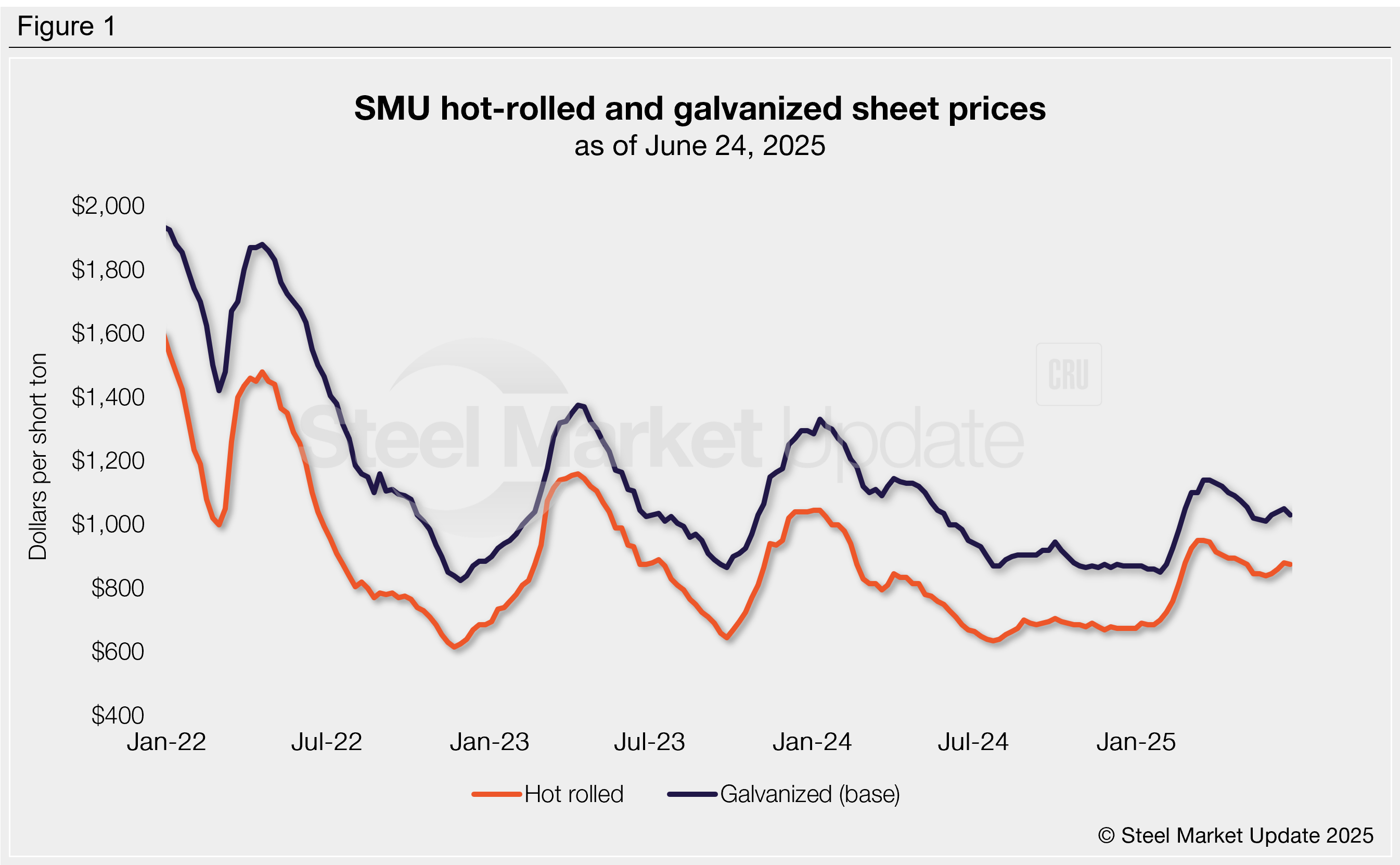

Hot rolled vs. galvanized price gap tightens further

Written by Brett Linton

The premium galvanized coil carries over hot-rolled (HR) coil has narrowed further since our May update, shrinking for the third consecutive month. As of June 24, the spread between these two products is just $5 per short ton (st) above the lowest level recorded in almost two years.

Recent trends

SMU’s average hot-rolled coil (HRC) price eased by $5/st this week to $875/st, the first week-over-week (w/w) decline since late May. Meanwhile, our galvanized index slipped $20/st w/w to $1,030/st (base), also the first weekly decline in three weeks. Prior to June, both HRC and galvanized prices had trended lower from late March through late May.

HRC prices today are 7% lower than they were three months ago but up 27% compared to the start of 2025, while galvanized prices are down 10% and up 18%, respectively. Figure 1 shows the pricing relationship between these two products since 2022.

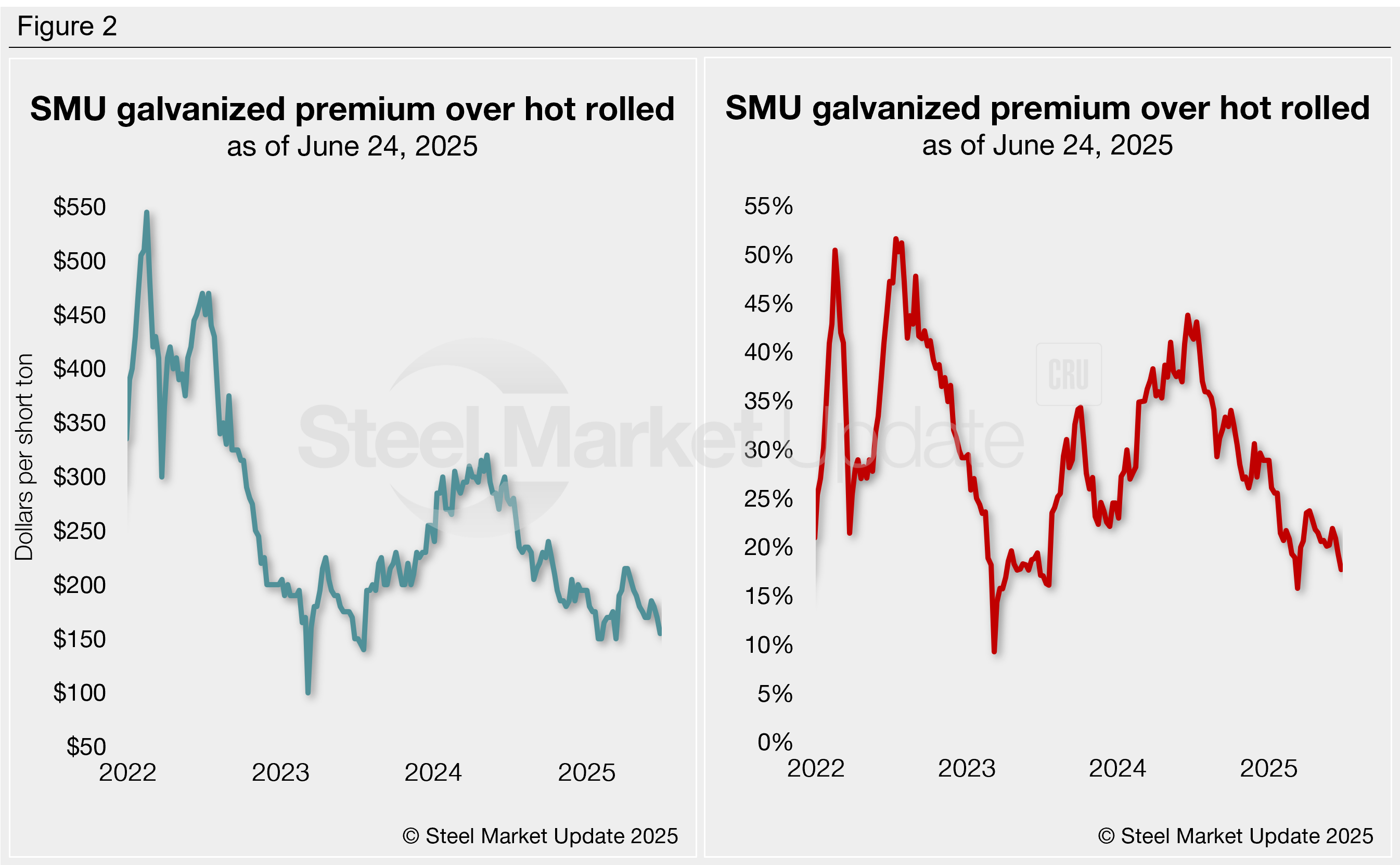

Galvanized premium shrinking

Currently, galvanized commands a $155/st price premium over HRC, marginally above the $150/st-low seen three times since mid-2023 (Figure 2, left). Spreads over the past month resemble those of February, March, and July 2023.

Around this time last year, we saw spreads between $270-300/st, though over the last 12 months it has averaged exactly $200/st. Historically, pre-pandemic spreads ranged mostly between $85-220/st during the 2010’s.

Another way to compare these products is to look at the galvanized premium as a percentage rather than a dollar value. The right graph in Figure 2 shows the hot-rolled/galvanized price spread as a percentage of the hot rolled price.

The percentage premium tells a similar story. It has shifted lower across the last year, falling to 18% this week. This is the second lowest percentage premium recorded in almost two years, just above the 16% low seen one week back in March.

This time last year the premium touched a near two-year high of 44%, an upwards trend generally witnessed since the March 2023 low of 9%. Compare this to the record high of 52%, which was seen in July 2022.