Prices

July 3, 2025

HR Futures: Financial players bullish on price, physical market participants not

Written by Joshua Toney

As you head into the long weekend, here is a recap of where things stand in hot-rolled (HR) coil futures along with some key datapoints.

Nucor increased its consumer spot (CSP) for hot-rolled coil (HRC) to $910 per short ton (st), up $10/st from last week. Backwardation persists in the forward HRC, with front months refusing to cross the $900/st level. The anchor CRU index print on Wednesday is a key cause for relative strength in July ‘25. But heading into Aug. ‘25-Oct. ’25, we see an average decline of ~$15/st per month.

The tariff backdrop is lending support to mill pricing power. But the price spikes from tariff headlines over the last several months have been muted compared to past price spikes. (The pandemic in ’20-21 and Russia’s full-scale invasion of Ukraine in ’22, for example.)

One key consideration is net positioning in CME futures. It had been on the ascent in 2025 until a rapid cut of exposure in June ‘25. As of June 24th, Commitment of Traders (COT) data points indicate that physical participants reduced length by 2,260/st while maintaining net long.

Managed money also sits on the long side of the market and added 8,940/st. Swap dealers’ primary positioning is in spreads. However, they added 6,180st to their short positioning. Other reportable positions sit net short and added 10,660st to their shorts. We can interpret that managed money still has expectations of price strength while physical participants are running closer to a balance on a net basis.

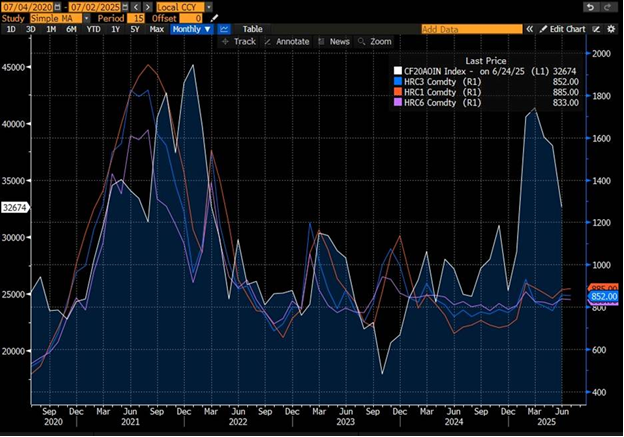

CME HRC M1, M3, M6 and CFTC net positioning

On the forward-looking side, mill margins are at healthy levels above $400/st on average. That’s partly because busheling scrap has dropped on a dollar basis from the $500 per gross ton (gt) prices seen earlier this year. Capacity utilization, according to the American Iron and Steel Institute (AISI) is at a healthy 79.1%.

Forecasted consumption upticks from new mill capacity heading into Q3 should be supportive for scrap pricing and, in turn, demand. Turkish import levels have been rangebound for HMS 80:20. I would put chances of an export price push on cut grades at limited.

Disclaimer

The views and opinions expressed in this column are solely those of the author, Joshua T. Toney, Principal of Corsair Elements LLC. This material is provided for informational and educational purposes only and does not constitute investment, trading, legal, or financial advice. Corsair Elements LLC is not registered with the Commodity Futures Trading Commission (CFTC) or the National Futures Association (NFA). Nothing contained herein constitutes a solicitation or recommendation to buy or sell any commodity interest, futures contract, swap, or other financial instrument. Readers should consult their own professional advisors before making any financial decisions.