Market Data

July 15, 2025

SMU Price Ranges: Prices slip despite tariffs as iffy demand weighs on market

Written by Brett Linton & Michael Cowden

US sheet and plate prices were flat or lower this week, as reduced import volumes were offset by so-so demand.

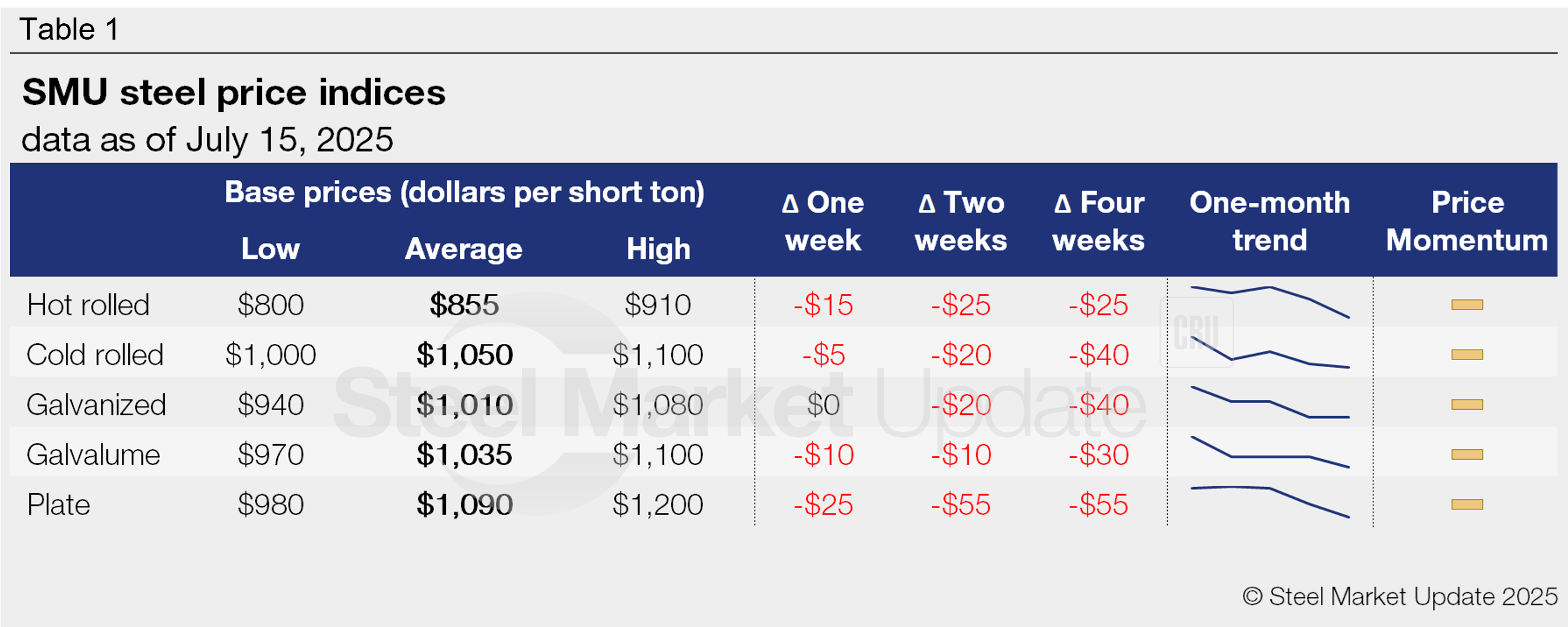

SMU assessed hot-rolled coil at $855 per short ton (st) on average, down $15/st from last week.

Our cold-rolled price stands at $1,050/st on average, $5/st lower compared to last week. Galvanized prices were unchanged at $1,010/st. And our Galvalume price slipped $10/st to $1,035/st.

SMU’s plate price is at $1,090/st on average, down $25/st vs. a week ago.

Our momentum indicators remain at neutral.

What they’re saying

Section 232 tariffs rising to 50% have raised the floor for domestic pricing by increasing the price of imports. And the prospect of higher tariffs on certain raw materials – notably pig iron from Brazil – could firm that floor, some market participants said.

But others pointed to mills running well below their rated capacity as an indication that demand continues to disappoint. They said mills might even move up fall maintenance outages if activity does not improve.

Yet few predicted that prices would crash, as they did last July. They said the market was largely in balance – with lower supply roughly in balance with lower demand.

“None of the mills are begging. They’d rather take an outage earlier rather than lower prices,” one service center source said.

“We’re waiting and wondering what might cause it to pop and go up. And we’re not noticing that the floor has already gone up,” said another.

Some notes on our price ranges

The high end of our HR range, $910/st, represents Nucor’s list price. Most sources assessed HR prices to be in mid-800s per ton. Some noted that prices in/around $800/st were available to larger buyers or from mills looking to attract business.

A few buyers predicted that prices in the $700s/st could come back into the market. But others said there was no compelling reason for domestic mills to do that on day-to-day business – especially with less import competition and in the face of potentially higher raw material costs.

On the galvanized side, our price range was wider than usual. That’s because a significant gap has developed between hot-rolled galvanized and cold-rolled galvanized, something that tends to happen in weaker markets.

Refer to Table 1 (click to enlarge) for our latest price indices and trends.

Hot-rolled coil

The SMU price range is $800-910/st, averaging $855/st FOB mill, east of the Rockies. The lower end of our range is down $30/st w/w, while the top end is unchanged. Our overall average is off $15/st w/w. Our price momentum indicator for hot-rolled steel remains at neutral, meaning we see no clear direction for prices over the next 30 days.

Hot rolled lead times range from 3-6 weeks, averaging 4.5 weeks as of our July 10 market survey.

Cold-rolled coil

The SMU price range is $1,000–1,100/st, averaging $1,050/st FOB mill, east of the Rockies. The lower end of our range is down $20/st w/w, while the top end is up $10/st. Our overall average is down $5/st w/w. Our price momentum indicator for cold-rolled remains at neutral, meaning we see no clear direction for prices over the next 30 days.

Cold rolled lead times range from 5-8 weeks, averaging 6.4 weeks through our latest survey.

Galvanized coil

The SMU price range is $940–1,080/st, averaging $1,010/st FOB mill, east of the Rockies. The lower end of our range is down $20/st w/w, while the top end is up $20. Our overall average is unchanged w/w. Our price momentum indicator for galvanized steel remains at neutral, meaning we see no clear direction for prices over the next 30 days.

Galvanized .060” G90 benchmark: SMU price range is $1,018–1,158/st, averaging $1,088/st FOB mill, east of the Rockies.

Galvanized lead times range from 5-8 weeks, averaging 6.4 weeks through our latest survey.

Galvalume coil

The SMU price range is $970–1,100/st, averaging $1,035/st FOB mill, east of the Rockies. The lower end of our range is down $20/st w/w, while the top end is unchanged. Our overall average is down $10/st w/w. Our price momentum indicator for Galvalume steel remains at neutral, meaning we see no clear direction for prices over the next 30 days.

Galvalume .0142” AZ50, grade 80 benchmark: SMU price range is $1,238–1,368/st, averaging $1,303/st FOB mill, east of the Rockies.

Galvalume lead times range from 5-7 weeks, averaging 6.3 weeks through our latest survey.

Plate

The SMU price range is $980–1,200/st, averaging $1,090/st FOB mill. The lower end of our range is down $20/st w/w, while the top end is down $30/st. Our overall average is off $25/st w/w. Our price momentum indicator for plate remains at neutral, meaning we see no clear direction for prices over the next 30 days.

Plate lead times range from 3-8 weeks, averaging 5.2 weeks through our latest survey.

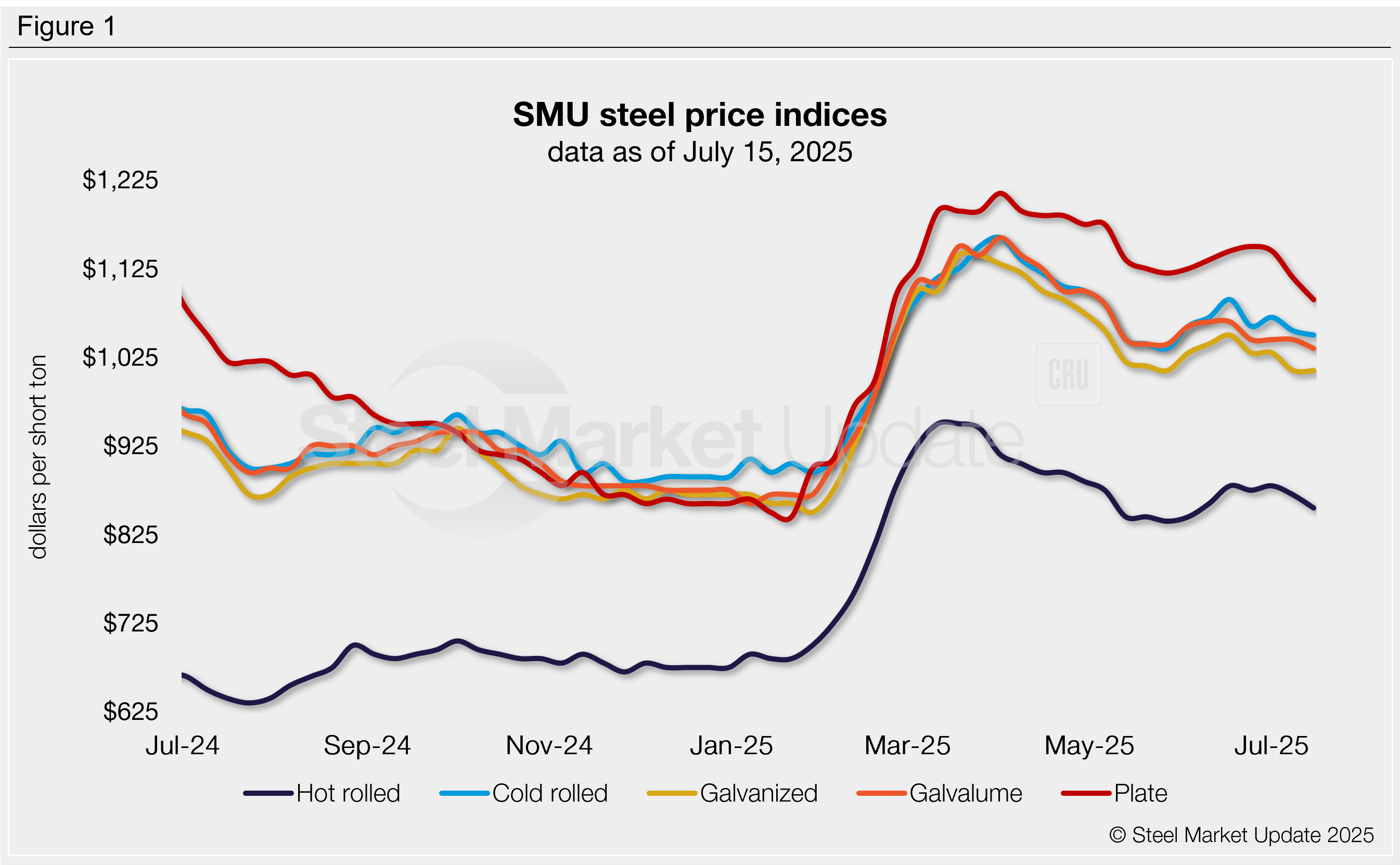

SMU note: Above is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume, and plate price history. This data is also available on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@steelmarketupdate.com.

Brett Linton

Read more from Brett Linton