Analysis

April 19, 2026

Final Thoughts: Steel remains bullish despite concerns about higher fuel, freight costs

Written by Michael Cowden

Editor’s note: The article below presents some highlights from SMU’s most recent steel market survey. The page numbers in the charts below refer to where in the survey results deck you can find them. Our premium subscribers received this deck on Friday. It’s also available to them on our website here. If you’d like to upgrade from an executive subscription to a premium subscription, let me know at michael@steelmarketupdate.com.

The flat-rolled steel market looks poised for continued gains despite widespread concerns about higher fuel and freight costs stemming from the Iran War, according to SMU’s latest steel market survey.

As I noted last week, lead times remain extended, and mills aren’t willing to negotiate lower prices. Buyer sentiment, meanwhile, remains robust (the highest in 2.5 years!) despite those worries about rising transportation and logistics costs. (More on that in a minute.)

Meanwhile, service centers’ sheet inventories stood at their lowest point in March since June 2021, per data released to our premium subscribers last week.

Climbing a mountain with a moving peak

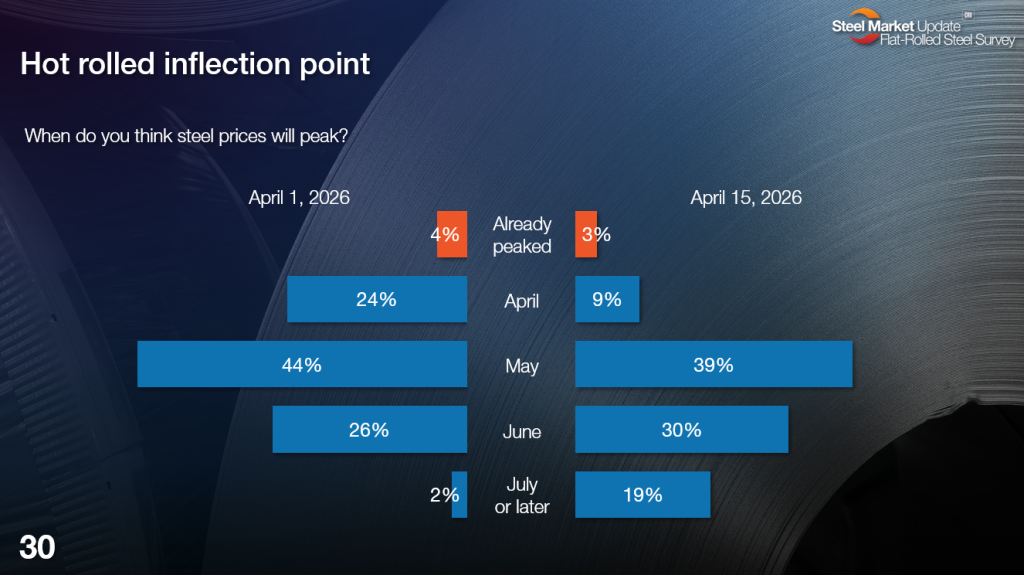

Combine those trends, and what’s the result? For starters, more people think the current rally in prices will last longer than what they predicted just two weeks ago, as you can see in the chart below.

Only 9% of survey respondents think prices will peak this month, down from 24% just two weeks earlier. And 19% think prices will keep rising into July or later, up from only 2% at the start of April. In other words, the trend of kicking the can on when the market will peak from one month to the next continues.

Here is what some survey respondents had to say, in their own words.

April

“Mills will try to push the envelope one or two more times. But economic uncertainty will set a limit.”

“There is not enough demand. Prices cannot remain this high.”

“The Iran War will increase raw costs for mills. But demand is slowing down due to cost pressures.”

“Not enough demand to support further increases.”

“Demand destruction.”

May

“I sure have been wrong about the longevity of this rally! I now think we’ve got a bit more run left. Sheesh.”

“There is more actual demand this spring than there has been in a year.”

“Demand destruction on the horizon.”

“Demand in Canada is well below average. If Canadian mills wanted to get pricing up, they should have done larger increases at the end of 2025.”

June

“Seems like prices can continue to rise through the second quarter based on stable demand and no more supply coming online in this period.”

“Tariffs appear rock solid for now. No reason to think otherwise.”

“Supply disruptions haven’t had their full effect.”

“I believe foreign will need to start arriving before mills move off their pricing.”

“Geopolitical issues and oil prices causing market apprehension.”

“All mills will have clarity on production, and imports will be known.”

“May or June, but more like June due to outages.”

“Demand will increase.”

“The market just keeps moving out.”

“Should stop climbing by summer.”

July or later

“Demand is they key factor. Inventory levels are dangerously low. Nothing to stop the upward movement right now.”

“Global news seems to indicate commodity prices will continue to increase.”

“Limited supply from imports and steady demand will keep prices increasing.”

“Late summer and back half of year demand will likely be strong.”

“Continued robust demand and an expectation of reduced geopolitical uncertainty.”

“Costs for most things are not going to keep going up.”

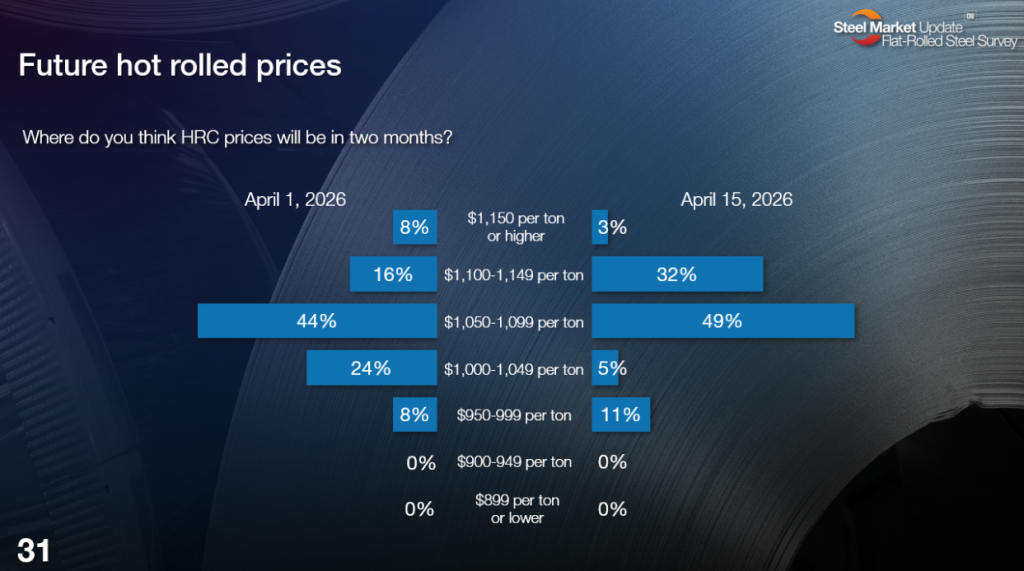

More see $1,100/st HR in store

Survey respondents also continue to revise upward their estimates on where hot-rolled (HR) coil prices will be two months from now:

Rewind to the beginning of the year, and the consensus was HR prices couldn’t go above $1,000 per short ton (st). Now, most people think HR prices will continue to inch higher from where they stand now. (Namely, $1,050/st in our last check of the market. We’ll update prices again on Tuesday evening.) And a significant minority (35%) think prices will be at or above $1,100/st by mid/late June.

Here is what some of them have to say:

$950-999

“We expect things to get right to $1,100 and then to fall back as summer approaches and post spring-outage season.”

“A price correction is coming. Will we create a new ceiling, or a new floor?”

“Weak demand in Canada.”

$1,000-1,049

“Up a little higher, then drifting down through the summer.”

“Scrap costs and supply will stabilize.”

“Educated guess on when the market will start moving down.”

$1,050-1,099

“Supply has not caught up. Service centers are low on inventory.”

“Energy pricing is going up and will keep prices elevated due to higher logistics costs.”

“Very slow increases over the next several weeks.”

“Nothing to stop the rise, and more maintenance outages being announced in the spring.”

“No sign of slowing down at the mills. They are still pushing out orders.”

“A lot of inflation and a lot of demand going on.”

“I don’t think the demand is strong enough to pass the $1,099 mark.”

“Geopolitical issues and oil prices causing market apprehension.”

“High levels of mill utilization, continued robust demand, and reduced geopolitical uncertainty.”

“One or two more upward moves.”

$1,100-1,149

“Nothing to stop the mills from continuing to increase prices.”

“We have another few months of increases. At least $60-80/ton more to come.”

“Demand is increasing.”

“Not enough competition.”

$1,150 or higher

“Demand is good.”

“Available capacity and lead times.”

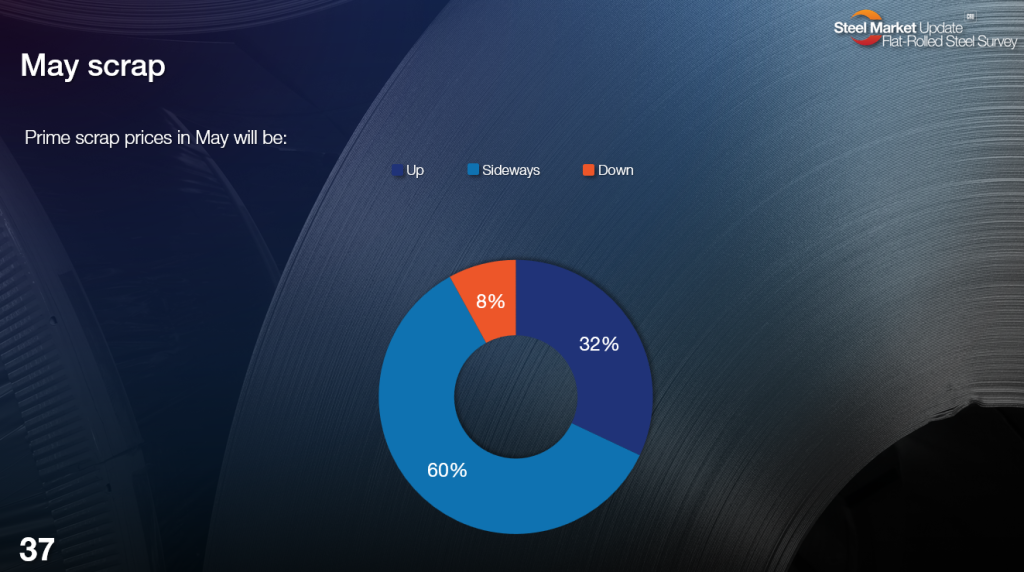

Scrap looking solid, service center inventories lean

Maybe it shouldn’t be a surprise people expect the price to be stable or higher. Especially since many also expect scrap prices to be stable or higher in May:

Such predictions follow SMU reporting on higher costs for Brazilian pig iron. The takeaway: The big gap between delivered pig iron costs and prime scrap prices could lead mills to lean more heavily on scrap next month – driving up demand and, at the very least, keeping prime prices sideways.

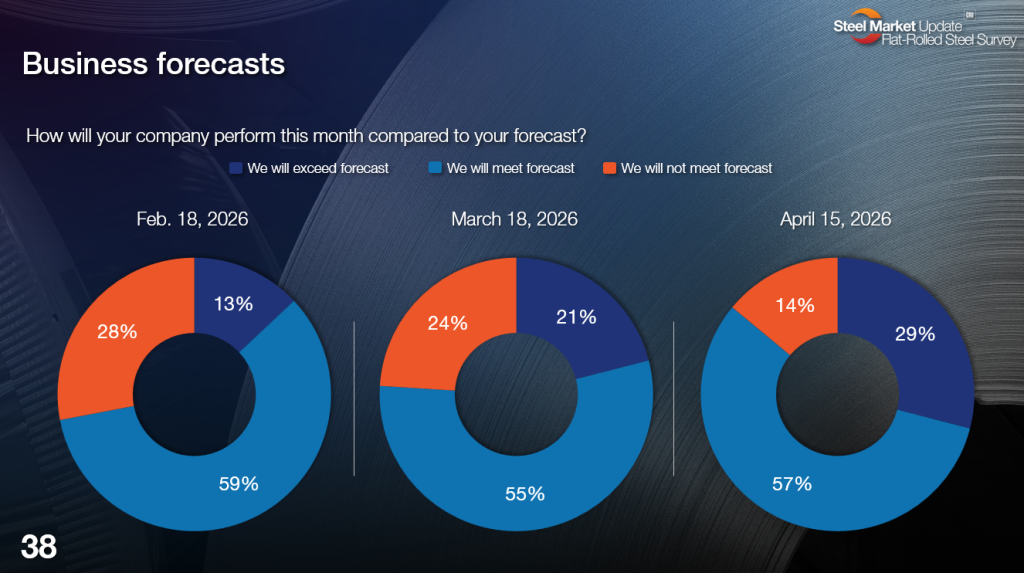

Also, as we’ve noted before, all the uncertainty we’ve seen (whether it’s tariffs or the Middle East) doesn’t seem to have had a noticeable impact on demand.

In fact, a growing number of people tell us they expect to meet or exceed forecast this month compared to prior months:

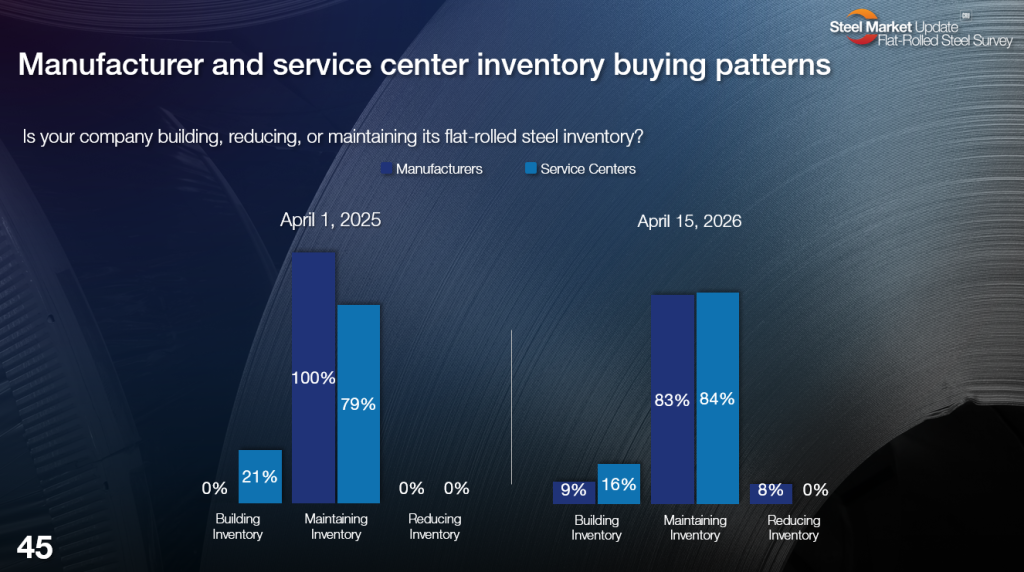

Given all of that, I’m a little surprised to see this result:

Namely, most steel consumers (83-84%) continue to tell us – as they have for months – they’re maintaining inventories and not building them.

Does that mean inventories could tick lower still this month, assuming demand holds up? It’s a question worth asking in an already tight spot market. Because, as noted in some of the comments above, and as I’ve heard from some of you directly, it’s possible inventories could get dangerously low if lead times remain extended, if demand holds up, and if cautious buying continues.

(Editor’s note: We released March service center inventory data to our premium subscribers last week. We’ll release April figures on or around May 15. And, again, contact me if you’re interested in upgrading from executive to premium.)

Fuel and freight move higher on the Iran War

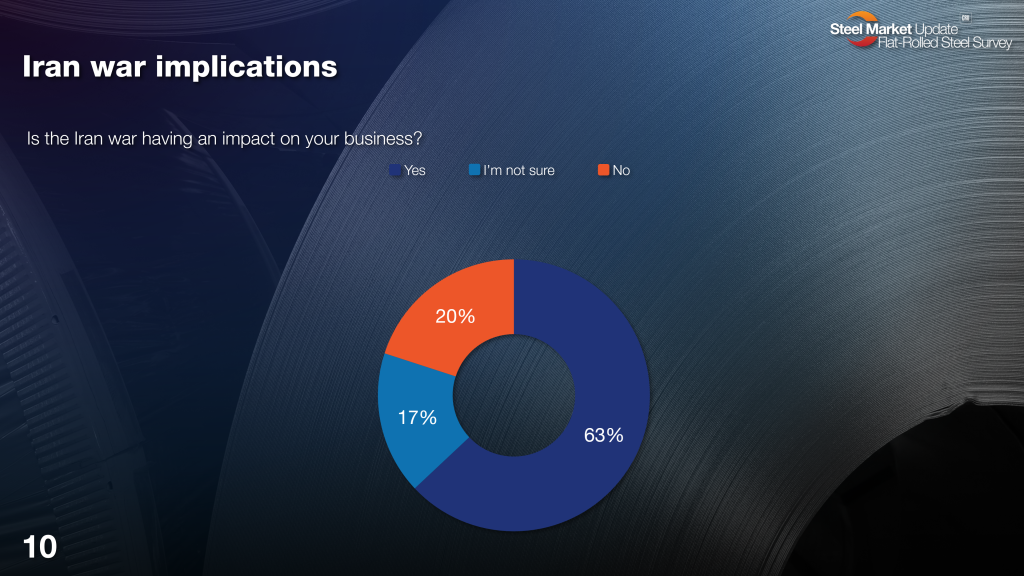

That’s not to say there isn’t a good reason for caution. Geopolitical uncertainty remains in the mix with the continued on-again, off-again talks with Iran over the Strait of Hormuz. Indeed, 63% of respondents said the Iran War continues to impact their businesses. That’s no small figure.

Here is what some of them had to say. I think you’ll notice an obvious theme. The main impact has been higher fuel and freight costs. There are also some concerns higher prices could eventually hurt demand.

Yes, the Iran War is impacting my business

“Transportation costs are killing us.”

“Freight. Also, it’s giving mills domestic protection – price protection – for now.

“It’s causing uncertainty.”

“Freight rates are skyrocketing.”

“Fuel costs are up.”

“High oil prices increase price pressure on commodities. Fuel prices add supply side upward pressure but could stifle demand.”

“Freight is starting to get a bit silly.”

“Freight costs.”

“Trucking surcharges due to fuel prices.”

“Freight costs and fuel surcharges.”

“Gas and freight costs.”

“Freight rates, for sure.”

“Freight and fuel costs.”

“Higher transportation costs.”

“Higher energy costs, higher aluminum costs.”

“The oil increase and increasing surcharges on all freight.”

“Raw material cost and logistics costs are increasing.”

“Just the overall jitters that go along with the conflict (minor impact).”

No, the Iran War is not impacting my business

“More impact on aluminum than steel.”

“No impact to our demand. But it did stop some import opportunities from the Middle East/Egypt.”

“It is just more ‘noise’ and giving folks another reason to not spend money!”

“Not yet. But as the economic effects continue, we will see more impacts.”

I didn’t include the “I don’t know” camp because their comments mirrored those in the “yes” camp – namely, higher fuel and freight costs. They’re just not yet sure what the impact of those costs will be on their businesses.

SMU-CRU VIP Briefing

Do you want to dive into the topics above in more detail? Then join me at the SMU-CRU Briefing – “Scouting the Market So You Don’t Have To” – on April 23 at the Swissotel in Chicago.

The event will start at 8:30 a.m. and wrap up at 12:30 p.m. We think you’ll come away with some “actionable” intelligence. And you’ll have plenty of time to meet with colleagues for a drink or three before the Metals Industry Scout Dinner in the evening.

Joining me will be CRU Research Principal Josh Spoores, Flack Global Metals Founder and CEO Jeremy Flack, Browns Gibbons Lang Managing Director Vince Pappalardo, BMO Managing Director Andrew Pappas, and SMU’s David Schollaert.

You can find out more and register here.