Rig count update: US count dips, Canada flat

Oil and gas drilling activity in the US edged lower last week, while the Canadian rig count held steady at a six-month high.

Oil and gas drilling activity in the US edged lower last week, while the Canadian rig count held steady at a six-month high.

This month’s column on the markets could be a response to the question of last month, “Are the forward curve prices on Aug. 7 high enough to price in trade case risks?" The market’s answer has been a pretty resounding YES so far, I think.

Current steel mill lead time averages are a few days longer than levels seen one month prior, but remain near historical lows for both sheet and plate products.

Hybar CEO David Stickler and SMU Managing Editor Michael Cowden shared a candid conversation about Hybar's ambitious plans on Tuesday morning at the SMU Steel Summit, held in Atlanta this week.

Zekelman Industries has bought 5% of available shares of Canada’s Algoma Steel.

Swampy. Sticky. Mushy. Murky. These were all words galvanized buyers used this week to describe the current state of the US steel market.

Oil and gas drill rig activity in the US inched lower last week while holding steady in Canada, according to the latest report from oilfield services provider Baker Hughes.

US drill rig activity recovered last week after slipping the prior week, according to the latest data from Baker Hughes. But Canada’s counts edged down following a five-week run-up. Despite the decline, Canada’s rig count remains near a five-month high. US rigs In the week ended Aug. 9, the number of active drilling rigs in […]

Flat-rolled steel prices have begun inflecting up on the back of mill prices hikes over the past couple of weeks. It’s a notable shift after tags slid downhill for most of the year. (There was a slight bump upward in late March/early April before the decreases resumed.) And now, after reaching levels not seen since […]

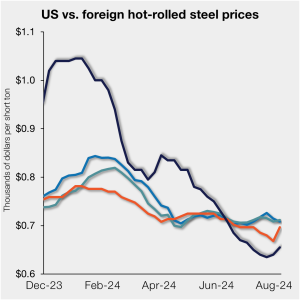

US hot-rolled (HR) coil remains cheaper than offshore material on a landed basis despite domestic tags inflecting upward lately. But the spread between domestic and foreign HR has tightened on the heels of price hikes by US mill over the past two weeks. (Visit SMU’s price increase calendar to keep track of the latest mill price announcements).

The company is in the process of being acquired by Cleveland-Cliffs in a deal valued at USD$2.5 billion.

Ryerson's earnings slumped in the second-quarter on-year but swung to a profit from the first quarter.

Longs producer and metal recycler CMC plans to open a new rebar fabrication plant in Akron, Ohio.

The US and Mexico announced measures on Wednesday to prevent tariff evasion and protect North America’s steel and aluminum industries.

First off, we hope everyone had a safe and happy July 4th holiday, with fireworks seen and BBQs attended. Many parts of the country are quite toasty at the moment, signaling that, yes, summer has indeed arrived. And looking at our most recent survey results, the summer doldrums have arrived as well.

US drill rig activity moved back up last week after drifting lower for four straight weeks. Meanwhile, Canadian counts slipped for the first time after a seven-week rally, according to the latest data from Baker Hughes.

Domestic steel shipments increased in May month over month but have fallen on-year.

US drill rig activity eased for the fourth consecutive week last week, while Canadian counts increased for the seventh week in a row, according to the latest data release from Baker Hughes.

US sheet prices continued to drift lower this week on lackluster demand, short lead times, and ample supply. SMU’s hot-rolled (HR) coil price now stands at $670 per short ton (st) on average, down $15/st from last week. Hot band is down $175/st from a recent high of $845/st in early April. It is also […]

US drill rig activity eased again last week, now down to levels not seen since late-2021, according to the latest data release from Baker Hughes. Canadian counts are moving in the opposite direction, inching higher for the sixth consecutive week to a three-month high.

US drill rig activity eased further last week, now down to a two-and-a-half-year low according to the latest update from Baker Hughes. In contrast, Canadian counts inched higher and are now at a three-month high.

Trading activity for the CME HRC futures contract has been sporadic so far in June, with a few days seeing transacted volumes exceed 25,000 short tons (st), but overall activity remains muted. This follows a pattern that emerged over the course of May.

Steel Market Update’s Steel Demand Index moved up 2.5 points last week, though it remains in contraction territory and at one of the lowest readings in nearly a year, according to our latest survey data.

Total steel exports rebounded 6% in April, rising to 842,000 short tons (st) according to the latest US Department of Commerce data.

Sufficient inventories resulting in softer demand continued to drag down US longs prices this month. Furthermore, lower scrap prices in May added to the downward pressure and expectations for June scrap are turning increasingly bearish. Import interest was also limited, particularly as competition among domestic producers rose.

Domestic steel shipments ticked up month over month (m/m) in April but were down year over year.

S drill rig activity held steady last week, remaining near two-year lows according to the latest update from Baker Hughes

The US OCTG Manufacturers Association (USOMA) announced that the US Customs and Border Protection (CBP) agency made an initial affirmative determination of duty evasion practices.

US drill rig activity eased further last week, receding to levels last seen at the start of 2022 according to the latest update from Baker Hughes

Steel Market Update’s Steel Demand Index fell five points to a 12-month low and moving further into contraction territory, according to our latest survey data.