Final Thoughts

August 8, 2024

Final thoughts

Written by David Schollaert

Flat-rolled steel prices have begun inflecting up on the back of mill prices hikes over the past couple of weeks.

It’s a notable shift after tags slid downhill for most of the year. (There was a slight bump upward in late March/early April before the decreases resumed.)

And now, after reaching levels not seen since November 2022 ($635 per short ton), hot-rolled (HR) coil prices moved up $20 per short ton (st) to $655/st in our last check of the market on Tuesday, Aug. 6.

Despite the upturn in prices, the direction of other indicators remains mixed. HR lead times have been holding around 4.5 weeks on average since mid-June. But buyers are finding mills somewhat less willing to negotiate lower prices, according to our last full market survey.

The modest decline in the number of mills willing to cut deals came after increase announcements by Nucor and by Cleveland-Cliffs. We’ll be curious to see whether negotiation rates continue to go down in the weeks ahead following those price hikes.

And while prices have finally turned upward, SMU’s Buyers’ Sentiment Index has dipped back down to levels not seen since the Covid-19 pandemic. But take that with a grain of salt. Sentiment was terrible in August/September 2020 – even as lead times and prices were stabilizing and showing early signs of recovery.

On the raw materials front, predictions are mixed as to where prime scrap prices will land this month. A solid majority expect sideways again in August, according to our survey. But some think that prime will move higher. It’s just a matter of days before we’ll know where scrap has settled.

Will HR prices rally or will they stabilize at a slightly higher level? A solid number of you (nearly 88% in last week’s survey results) expect prices will range between where they are now (approximately $650/st) and $750/st come Q4.

Here’s some of the other data we’ve been looking at.

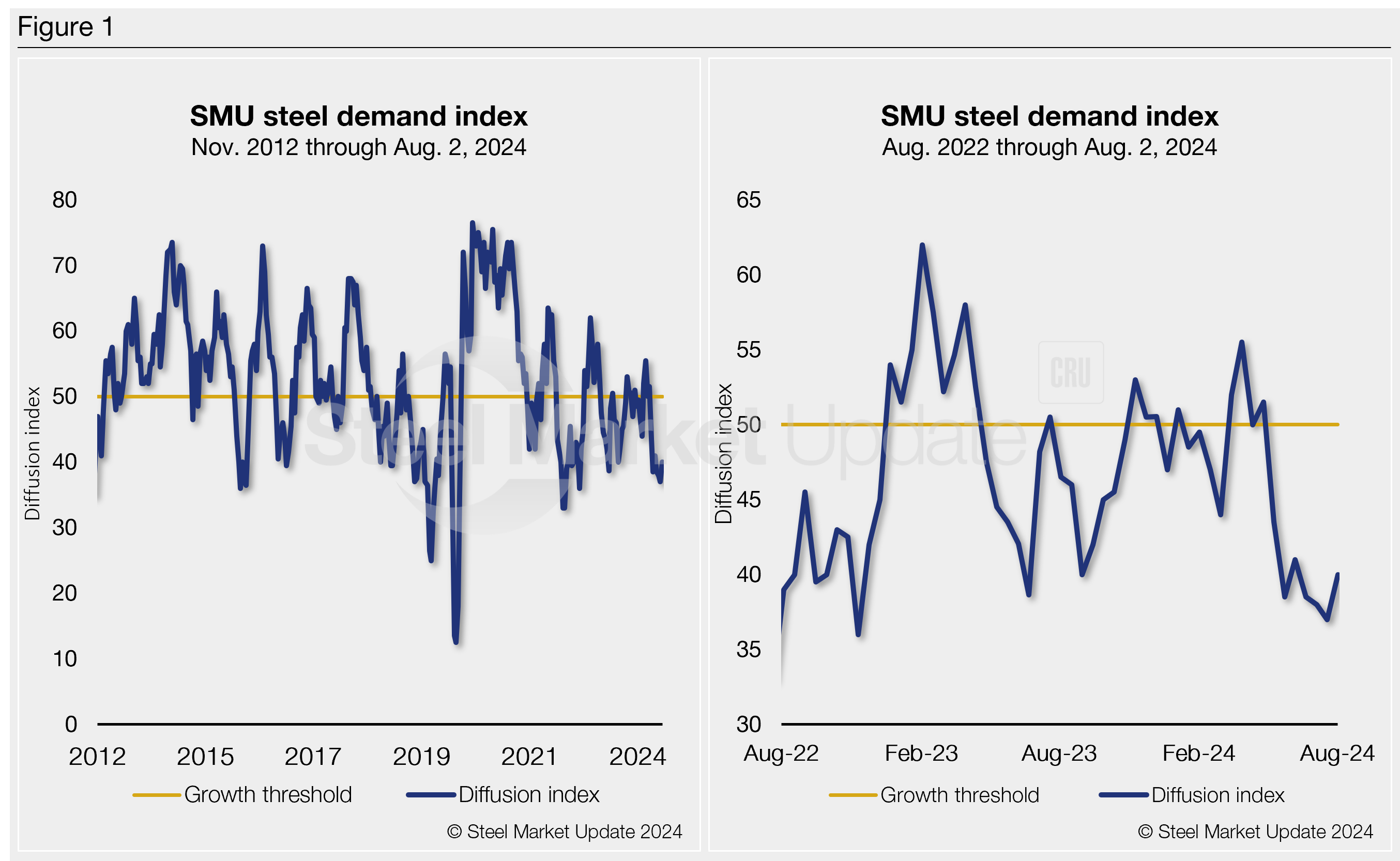

Steel demand index

SMU’s Steel Demand Index has been in contraction territory since early May. The index – now at 40 – is up three points from a reading of 37 in late July, its lowest mark since July 2022.

The index, which compares lead times and demand, is a diffusion index derived from the market surveys we conduct every two weeks. An index score above 50 indicates rising demand, and a score below 50 suggests declining demand. Detailed side by side in Figure 1 are historic data and the latest Steel Demand Index.

Our index has been in contraction territory for the better part of the past year. The index has had some small bumps into growth. But they’ve mostly been short lived and in the wake of mill price hikes. Generally speaking, it has been down more often than not over the past 18 months.

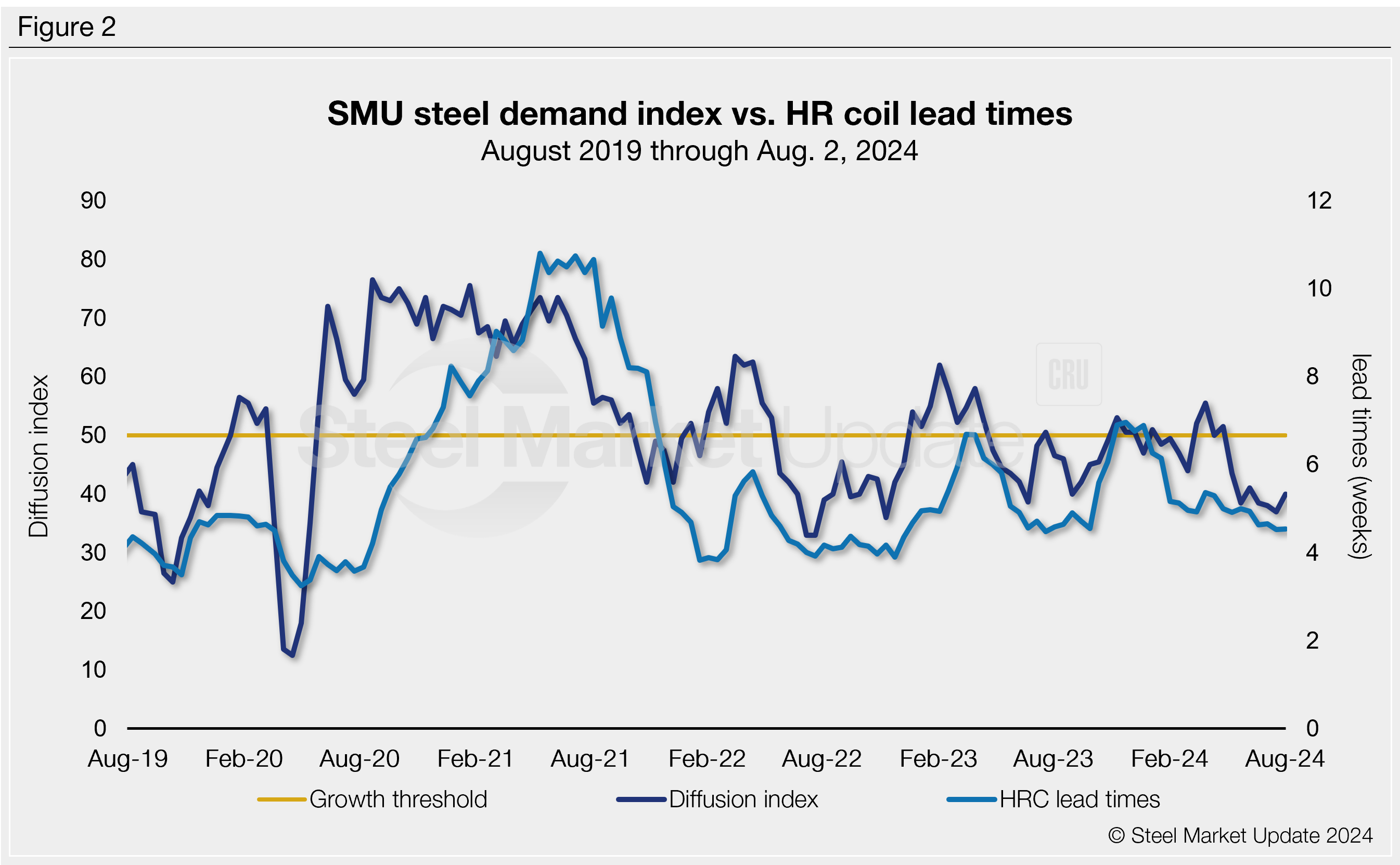

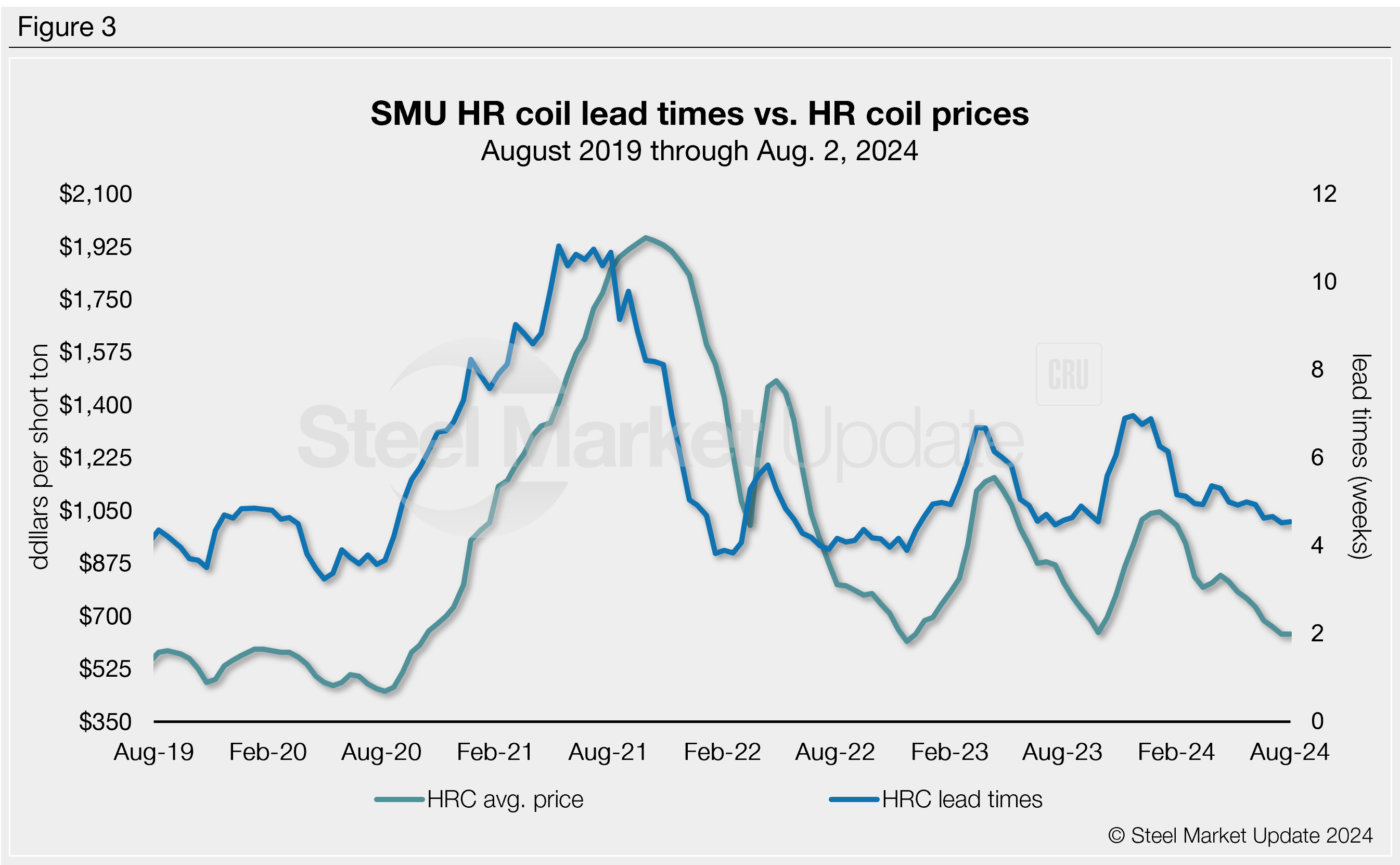

Why should you pay attention to SMU’s demand diffusion index? It has for years preceded moves in steel mill lead times (Figure 2). And SMU’s lead times have themselves been a leading indicator for flat-rolled steel prices, particularly HRC (Figure 3).

What to keep tabs on

Lead times should remain in focus. If demand is indeed soft, will they remain largely unchanged? Or could we see them extend on the back more order activity over the last couple of weeks?

What about the steel buyers who make up the bulk of our survey respondents? How are their businesses doing? More than 35% of respondents in our last survey said they missed their business forecasts in July. Only ~5% exceeded forecasts last month. Also, more than three-quarters of service centers said they were releasing less steel than a year ago. Will things improve this month?

We have seen early signs that service centers are at least holding the line on prices. Only 40% of service centers reported lowering prices in our last survey – a reaction to mill price hikes. That’s a significant shift from the nearly 85% who were cutting prices in mid/late July. But only 4% of service centers reported increasing prices last month. Will see see that number increase in August?

And what does all of this mean for contract negotiation season? Will lackluster prices and less-than-stellar demand continue? Or have we finally turned a corner on demand? Let me know what you think!

SMU Steel Summit

We’re just about two weeks away from the start of the 2024 SMU Steel Summit, and it promises to deliver big once again.

We’re happy to report that the mobile networking app is now live. Download it in Apple or Android app stores and start networking with more than 1,300 (and counting) industry leaders today!

We look forward to seeing you on Aug. 26-28 at the Georgia International Convention Center (GICC) in Atlanta. You can learn more about the Summit and our agenda here. And you can register here.

And as always, your business is truly appreciated by all of us at Steel Market Update.