Prices

September 20, 2018

Futures: HR, BUS, and USSQ Q4'18 Futures Trading Higher

Written by Jack Marshall

The following article on the hot rolled coil (HRC) steel and financial futures markets was written by Jack Marshall of Crunch Risk LLC. Here is how Jack saw trading over the past week:

Steel

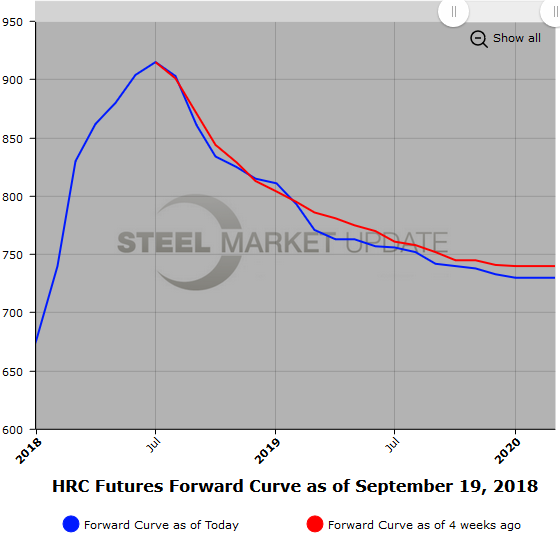

The HR spot market has continued to decline, however we have a bit of a divergence as the HR futures curve prices recover some of the recent backwardation we had in early September. Healthier prices could be a function of lead times starting to extend again after recent narrowing along with some anticipated mill outages expected. Uncertainty has left many firms likely with trim inventories and concern over the next buying cycle. Imports do not appear to be a factor yet as uncertainty trumps the price differential.

HR futures curve backwardation is becoming less steep in the near quarters. Sep’18 HR futures price has basically remained unchanged at $860/ST, but Q4’18 has been bought higher as the Sep’18 to Q4’18 spread has narrowed from approximately $57/ST to $36/ST since the beginning of the month. We have seen both the Q4’18 HR and Q1’19 HR average prices rise by $22/ST and $14/ST over that period, while the Q2’19 HR and Q3’19 HR prices have remained unchanged since the beginning of September ($760 and $750).

The latter half of Cal’19 futures prices reflect lower global steel price of imports plus the current tariffs. The latest 2H’19 HR settlement was just under $744/ST.

This week, just under 42,000 ST of HR futures have traded through the exchange with the bulk of the activity in Q4’18 and Q2’19. Futures Open Interest is just short of 340,000 ST.

Below is a graph showing the history of the CME Group hot rolled futures forward curve. You will need to view the graph on our website to use its interactive features; you can do so by clicking here. If you need assistance with either logging in or navigating the website, please contact Brett at 706-216-2140 or Brett@SteelMarketUpdate.com.

Scrap

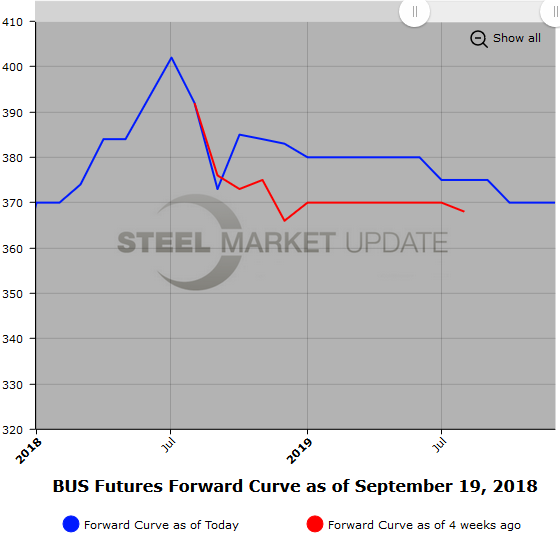

Prime scrap futures have been active this month after the September prices traded down $20/GT to just under $373/GT. Sentiment appeared to shift for October BUS futures as $384/GT traded in 6,000 GT and was followed by buying interest in Q4’18 BUS also at $384/GT in 5,000 GT per month. This brought the BUS forward curve prices up about $10/GT from the prior week’s settlements as the Q4’18 buying still rests above $382/GT. Also, 1H’19 traded higher as $380/GT traded in 500 GT per month. Higher prices could provide some opportunities for inventory hedges.

LME HMS 80/20 Steel Scrap has been a bit quieter with the near dates pushing $310/317/MT and the Jan’19 trading around $304/MT.

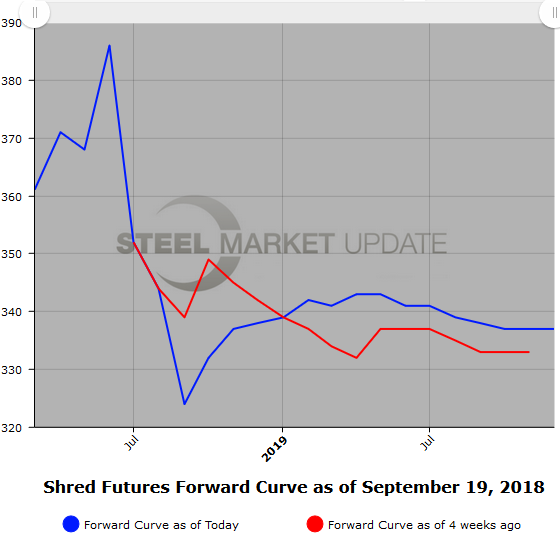

NFX USSQ U.S. Midwest Shred scrap has also started to push higher following the September AMM settlement ($320/GT). Oct’18 USSQ and Q4’18 USSQ are currently $330/GT bid following an Oct’18 USSQ trade at $330/GT in 4,000 GT last week. The Oct’18 trade was a $10 premium to the September settlement. Interests suggest some increased demand expectation for scrap going into Q4 and also Q1’19 from both domestic and international flows. The curve settlements for USSQ have a small contango going into the 1H’19 reflecting some seasonal supply concerns.

Below is another graph showing the history of the CME Group busheling scrap futures forward curve. You will need to view the graph on our website to use its interactive features; you can do so by clicking here.

We have started tracking USSQ shredded scrap futures, shown below. Once we have built a sizable database, we will add this data to our website.