Product

June 6, 2021

Michael Cowden Speaks About Steel Prices, Scrap & China

Written by Michael Cowden

I want to thank the National Association of Steel Pipe Distributors for giving me a chance to open their summer conference in Denver last week.

I spoke about – what else, these days – steel prices. During the Q&A afterward and on the sidelines of the event, it was clear people were worried about (a) passing higher costs (for coil in the case of welded tube producers) along to their customers, (b) high inventory costs and (c) the potential for inventory values to plummet when prices eventually head down again.

It’s not my job to make forecasts. And I don’t envy those tasked with doing so. But I can at least flag things worth keeping a close eye on. And here are two I’d pay close attention to in the weeks and months ahead: (1) domestic scrap prices and (2) steel prices in Asia.

One is bullish for prices. The other might not be.

Scrap

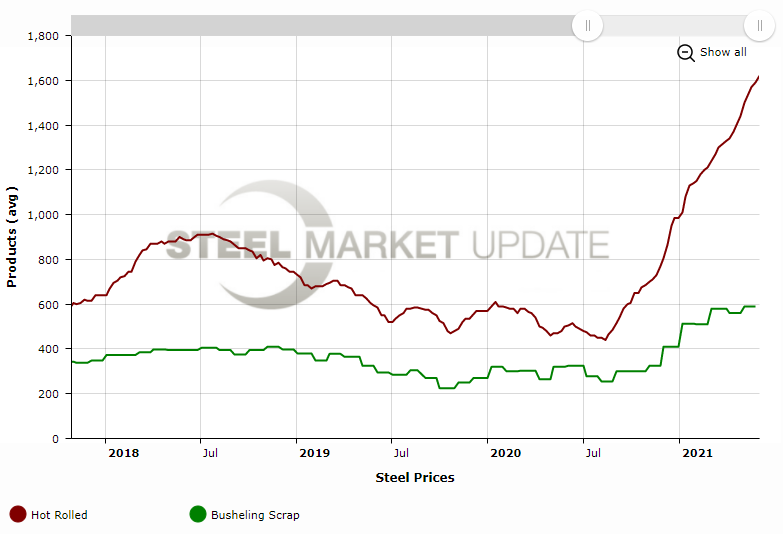

Let’s start with the chart above. The red line is hot-rolled coil prices. The green line is scrap.

I remember back in 2018 when HRC prices went above $900 per ton for the first time since 2008. Scrap prices merely held their ground in comparison. It was a frustrating experience for scrap suppliers. But there was at least some explanation. Section 232 tariffs and quotas were imposed on steel, not on raw materials.

I also remember, back when I started covering flat-rolled steel, being told that hot-rolled coil typically stayed in a relatively narrow bandwidth of $500-700 per ton. It never went too far below that because mills started losing money. And it never went too high above that, or else imports would flood in and send prices lower. I was told to keep an eye out for such “mini-cycles.” It seemed like good advice at the time.

Not any longer. None of us have seen a market like this before. And that $500-700 per ton price range for HRC I was told about would more accurately describe prime scrap prices these days.

Is it possible that the link between HRC and scrap as we knew it is gone?

The chart above certainly suggests so. HRC prices average $1,620 per ton and prime scrap prices are $590 per gross ton – or $526.79 per short ton. Scrap prices haven’t settled yet for June. But let’s assume the rest of the U.S. market follows Detroit, which recently settled up $60 per gross ton, or $53.57 per short ton, on primes. And let’s assume – and this is a very generous assumption – that HRC prices remain unchanged next week.

Now for conversion costs. I remember being told eons ago that the cost to convert scrap to coil was approximately $150 per ton. I’ve been in this industry longer than I care to admit. And conversion costs are probably more like $200 per ton today given that electric-arc furnace (EAF) mills now make more sophisticated products, and given increased use of pig iron as well as scrap alternatives such as direct-reduced iron (DRI) and hot-briquetted iron (HBI). So let’s shoot down the middle and assume a conversion cost of $175 per ton

The result: Prime scrap prices are $580.36 per short ton, conversion costs are $175 per ton – and so hot metal costs are about $755.36 per ton. Which means mill margins are at approximately $864.64 per ton.

That makes margins during the peak of the Section 232 frenzy in the summer of 2018 look almost modest.

ARTICLE CONTINUES BELOW

{loadposition reserved_message}

HRC corrected downward toward scrap prices later in 2018 as the panic surrounding Section 232 faded. And the consensus probably remains that HRC will correct down again. Namely, that demand will cool and we’ll revert to a cost-plus environment.

But what about the possibility that scrap will correct upward?

I suggest that because a lot of new capacity is coming into the North American market. And, as our new capacity tables note, almost all of it is EAF-based. That means there is going to be a lot more demand for prime scrap, which, unlike obsolete grades, is not elastic to price.

In the case of obsolete grades, more will be collected if prices are high enough. But busheling scrap comes from industrial processes like stamping. And it’s not like automakers are going to stamp more parts if they don’t need them just because scrap prices are high.

Prime scrap potentially being in short supply matters because EAF mills in slow markets have set the floor for steel prices. And I’d venture that whenever things slow down next, that floor will be higher.

Also, look again at the spreads between scrap and HRC. You would think that at some point scrap suppliers might look at something like this and realize that maybe scrap is undervalued. Why wouldn’t stampers, so sensitive to costs, not notice that they’re not getting their money’s worth for their scrap?

And it’s not just EAF mills in the U.S. that are expanding. We are also seeing integrated mills converting to the EAF route: Think Algoma Steel in Canada or SSAB in Sweden, to take just a couple of examples.

The driver: More and more integrated mills are looking to get into EAF steelmaking to reduce their carbon emissions. Basically, it’s hard to square the Paris Agreement and the coking process.

Governments across the developed world are looking to reduce CO2 emissions. Some are putting a price on carbon and rolling out carbon border taxes. So it’s not just do-gooders driving this. There is a financial incentive to make this switch from integrated steelmaking – blast furnaces and coke ovens – to EAF steelmaking.

The upshot: U.S. mills might have a tough time sourcing prime scrap from Europe if more and more mills on the continent switch to electric steelmaking. And if China does so too, that could really lead to some shortages.

Could we see export restrictions on scrap? I don’t know. But it’s something worth thinking about.

So I think scrap prices are, long term, bullish for steel prices. But what about the nearer term?

Prices in Asia

This is the one that worries me the most. And CRU, SMU’s parent company, flagged it in a recent article that we ran in these pages.

Prices in Asia are cooling off. Is that because of China’s efforts to tame inflation? Is it because of increased capacity in Southeast Asia? Or is it a matter of the pandemic surging again in parts of Asia?

I don’t know. But what I do know is that U.S. prices typically follow those in Asia as they move down, with a bit of a lag. Is that two months, four months or eight months? That’s a question worth assigning an analyst. Because if prices in Asia see a sustained decline, presumably there is trouble on the horizon here in the U.S. as well.

It might be hard to see any signs of trouble in the West, broadly speaking. There is little evidence of trouble in Europe. Lead times are into the fourth quarter. And European imports, once Section 232 tariffs are taken into consideration, are theoretically more expensive than U.S. product.

There is a legitimate question about whether high prices might lead to demand destruction.

U.S. HRC prices are more than triple what they were a year ago. What does that mean for steel-intensive goods? Will consumers really agree to pay more than triple what they paid a year ago for a new grill? I sure wouldn’t.

But so far we’re just not seeing evidence of demand destruction in our survey results.

Again, I don’t know when prices might correct. And I think there is a good chance that it might not be for a while. I’ve written before that I think new EAF capacity is needed just to offset idled blast furnace capacity – and that any correction from new capacity alone might not happen until as far out as the first half of next year.

That said, the U.S. is hardly an island. And that’s why it’s worth keeping a very close eye on prices in Asia. Because Asia might be a precursor of what’s to come here.

As for the U.S., I think it’s safe to say that the first time the CRU prints lower, people will take notice. If it prints lower twice in a row, people will start to worry. And if it prints lower for a third consecutive time, there will be panic and pandemonium.

I know some of you might say this kind of thinking – this constant looking for tipping points – isn’t helpful. But with prices as high as they are, we’d be doing a disservice to the market if we didn’t suggest that our readers keep a sharp eye out on the indicators that matter.

By Michael Cowden, Michael@SteelMarketUpdate.com