Prices

October 28, 2021

HRC Futures: October Declines by $34, Downtrend Emerging

Written by David Feldstein

Editor’s note: SMU Contributor David Feldstein is president of Rock Trading Advisors. Rock provides customers attached to the steel industry with commodity price risk management services and market intelligence. RTA is registered with the National Futures Association as a Commodity Trade Advisor. David has over 20 years of professional trading experience and has been active in the ferrous derivatives space since 2012.

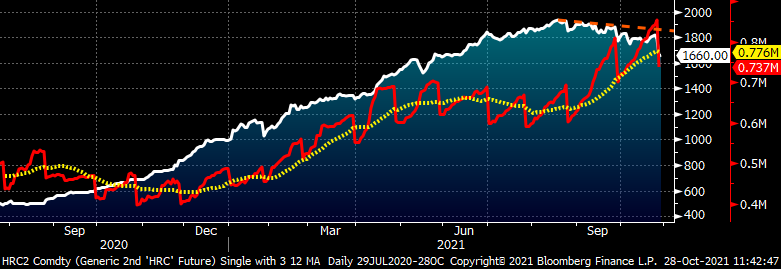

In the chart below of the rolling 2nd month Midwest HRC future (now December), the red line represents total open interest (O.I.) across the 36 months of HR futures and the yellow dotted line is O.I.’s 22-day moving average. O.I. is the total number of contracts trading on the exchange, in this case, per day. The sharp drops in O.I. occur when the front month expires. O.I. fell from 854k tons to 737k last night because of October’s expiration, which settled down $34 at $1,900/st. It was the first monthly decline since August 2020.

Rolling 2nd Month CME Hot Rolled Coil Future $/st

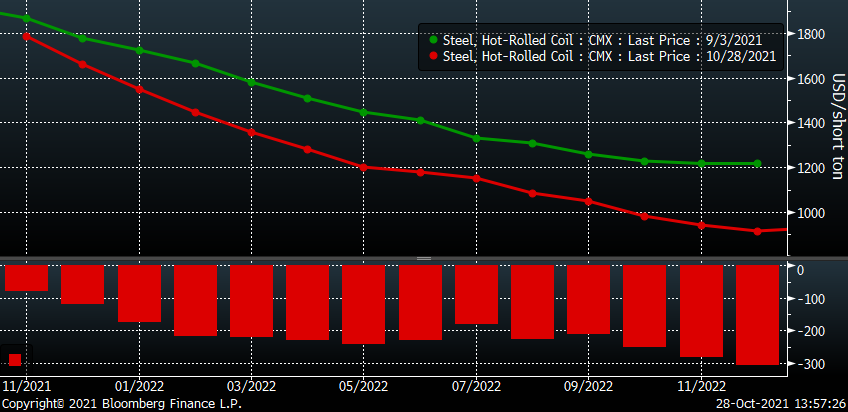

For the October CME HRC future and months that follow it, Sept. 3 was the peak. The chart below shows the settlement prices on Sept. 3 (green) and today (Oct. 28 red) with the histogram in the lower panel showing the price change over that time. Since Sept. 3, November fell by $80/st, December $120, January $175 and the rest of ’22 through October by roughly $200.

O.I. exploded to new all-time highs in September while the curve fell dramatically as aggressive sellers entered the market. This group appeared to be primarily comprised of service centers hedging inventory and import deals. Throughout October, open interest has expanded further to yet another record high. However, the curve saw much less volatility with the December ’21 to March ’22 contracts gaining $30-$40/st, while May ’22 to December ’22 declined by $25-$90/st. October’s trading appears to have been fueled by buyers looking to hedge Q1 ’22 at prices sharply discounted to spot.

CME Hot Rolled Coil Futures Curve $/st

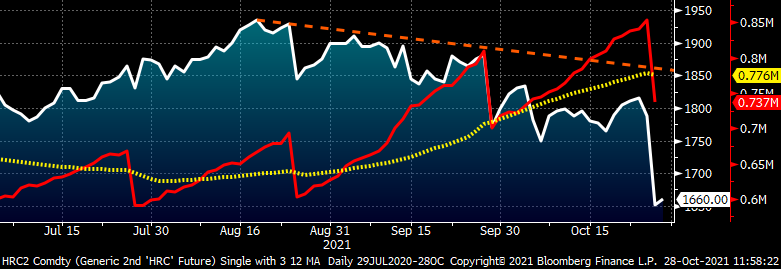

The curve flipped from contango (upward sloping) to backwardation (downward sloping) late last September as the October ’20 contract rallied to $590. As the market marched higher through this past August, the backwardation became steeper, though it never broke its uptrend. That has changed as the market has crested and rolled over into a downtrend.

Since, the rolling 2nd month CME HRC future peaked on Aug. 18 at $1,935, it has continued to trend lower while open interest has surged. Expanding open interest plus a downtrend equates to a technically strong bear market. The sharp decline from $1,800 to $1,651 is the result of the roll forward from the November contract to the December future. With the curve sharply backwardated to the tune of $150-$110 per month through March, it can be assumed this is going to keep happening and the downtrend in the rolling 2nd month HR future will continue for a very long time. That is unless something happens that ignites another price spike.

Rolling 2nd Month CME Hot Rolled Coil Future $/st

Coming into 2021, this chart of HR imports looked to have bottomed after six years of decline. The AD/CVD trade cases and Section 232 tariffs were effective at squashing imports. The import release valve that typically kept domestic prices tethered to global prices was out of commission. However, that has changed, and imports have continued higher month after month. Interestingly, import license data has underestimated the actual hot rolled tons imported in each of the past four months. September’s license data indicated 277k short tons of HR imports, a noticeable MoM decline of 103k. However, September’s actual HR imports posted earlier this week were 440k, an increase of 60k MoM and the highest total since 2015. Considering the massive spread between domestic and global prices growing throughout the year, coupled with drawn-out (mill) contract negotiations, imports can be expected to continue at these levels, perhaps going higher still, well into the first half of ’22.

HRC Imports st

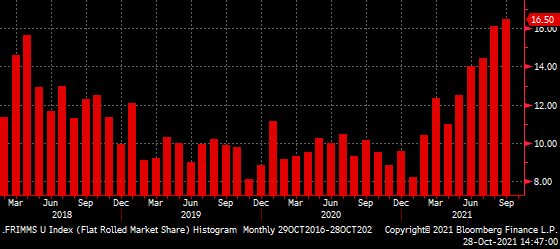

The following chart is an estimation of U.S. imports’ market share of domestic flat rolled sheet and strip consumption. It shows imports have been taking market share from domestic mills in recent months, which has coincided with growing service center inventory and falling mill lead times. All of this as new domestic production capacity is just around the corner.

Flat Rolled Imports Market Share

The pre-COVID rule of thumb was imports started taking market share once the domestic premium was over $100. With the import market’s revival, global prices become a beacon for where prices are headed. Chinese hot rolled prices collapsed in October with the SHFE January Chinese HR future falling $100 so far this month to $700/st, $50 of which occurred Tuesday! While Chinese steel isn’t directly imported to the U.S. due to the massive 200%+ duty, prices in China influence price direction in Asia and Europe, which can export to the U.S. and where prices have been falling for months. Point being, watch China’s price closely.

Active (January ’22) SHFE Chinese Hot Rolled Coil Future $/st

Chinese steel production has declined dramatically in recent months while the price of iron ore has collapsed. How much of the decline in production is due to China’s attempts to clean up air pollution ahead of the Winter Olympics, their energy shortage or their shaky property market is uncertain for now. How much further these issues weigh on their economy and how much of that weighs on the global economy also remains unknown. However, the real-time data provided by the crash in iron ore and decline in production then followed by a $100/st decline in hot rolled so far in October should be looked at as a major warning sign.

Rolling 2nd Month SGX Iron Ore Future $/mt

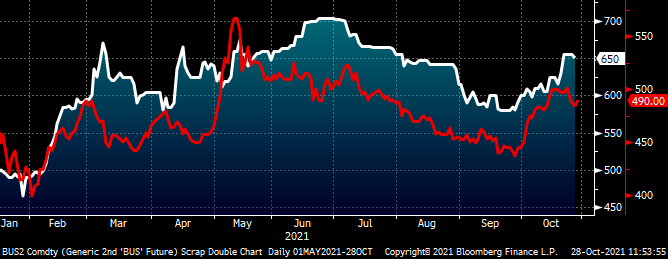

Interestingly, both busheling and Turkish scrap prices have bucked ore’s weakness, having rallied since both products’ most recent settle was at their respective lowest levels since April ($583.43/gt for October busheling and $439.88/mt for September Turkish Scrap).

Rolling 2nd Month CME Busheling & LME Turkish Scrap Futures

There doesn’t seem to be much debate about the future direction of domestic flat rolled prices, but rather by how much and how quickly they slide. The CME HRC futures curve has priced in these expectations. The question is how accurate the curve’s current pricing is relative to the actual prices we will see in each respective month. This is indeed a million dollar question if I’ve ever seen one.

Disclaimer: The content of this article is for informational purposes only. The views in this article do not represent financial services or advice. Any opinion expressed by Feldstein should not be treated as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of his opinion. Views and forecasts expressed are as of date indicated, are subject to change without notice, may not come to be and do not represent a recommendation or offer of any particular security, strategy or investment. Strategies mentioned may not be suitable for you. You must make an independent decision regarding investments or strategies mentioned in this article. It is recommended you consider your own particular circumstances and seek the advice from a financial professional before taking action in financial markets.