Prices

November 11, 2021

Hot Rolled Futures: Market Retracement – Gradual or Quick? Or Sideways?

Written by Jack Marshall

The following article on the hot rolled coil (HRC), scrap and financial futures markets was written by Jack Marshall of Crunch Risk LLC. Here is how Jack saw trading over the past week:

Hot Rolled

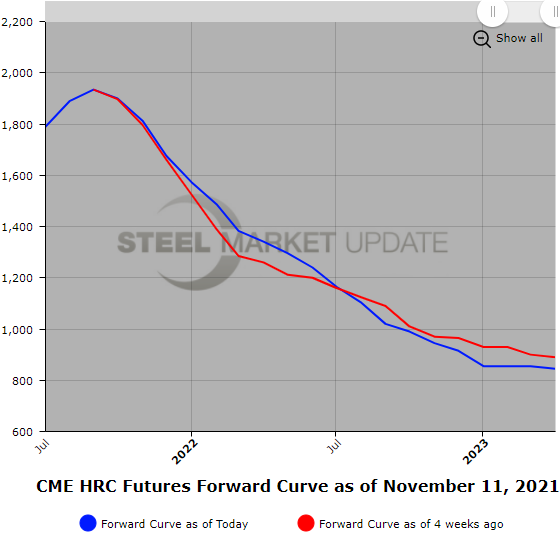

Spot HR has declined each of the last three Wednesday’s for a total loss of $86/ST. Spot HR has lost $140/ST since peaking at the end of September. During this new trend in physical HR pricing, the HR futures curve shape has shifted significantly as Q1’22 and Q2’22 prices have risen $105/ST and $57/ST and Q3’22 and Q4’22 prices have declined by $50/ST and $77/ST, leaving the shape of the curve in Cal’22 more steeply backwardated as the quarter-versus-quarter spreads have widened out. Q1’22 HR vs Q4’22 HR moved out from $350/ST to $531/ST. Today’s HR Jan’22 settlement of $1,573/ST is $658/ST higher than HR Dec’22 settlement of $915/ST.

Open interest is moving up marginally. Since the 5,500 lots of October Futures rolled off dropping open interest to 37,723 lots, we have seen a gain of roughly 1,400 contracts. With the recent change in price direction, HR futures volumes have been a bit softer due to a slight downtick in hedging as participants hold off. Market participants continue to wait for clearer signals regarding the stability of HR spot pricing, HR spot availability going forward, contract negotiations, and pricing impact of steel imports. Will the price trend lower pick up steam or will it retrace gradually? How will the COVID factor impact U.S. HR?

Below is a graph showing the history of the CME Group hot rolled futures forward curve. You will need to view the graph on our website to use its interactive features; you can do so by clicking here. If you need assistance with either logging in or navigating the website, please contact us at info@SteelMarketUpdate.com.

Scrap

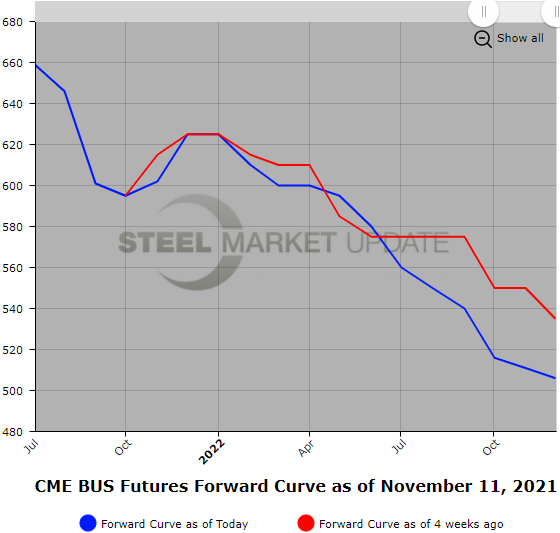

BUS futures settlement for November at just north of $602/GT was pretty much in line with market expectations. Recent increased focus on metallics along with some recently announced consolidation in the scrap space and Congress’ new infrastructure stimulus package should generate some buzz. Early expectations are for BUS to rise by at least another $20/GT for December. Both pig iron and export 80/20 prices have been supportive. Since Nov. 1, BUS settlement prices have on average for Cal’22 declined by roughly $26/GT, likely related to lower volume of transactions as we go into year-end along with recent strong demand for shred.

Below is another graph showing the history of the CME Group busheling scrap futures forward curve. You will need to view the graph on our website to use its interactive features; you can do so by clicking here.

Editor’s note: Want to learn more about steel futures? Registration is open for SMU’s Introduction to Steel Hedging: Managing Price Risk Workshop to be held Nov. 2-3. You can get more information by clicking here.