Analysis

June 13, 2025

Survey says: Market hit with another blast of tariff whiplash

Written by David Schollaert

If you’re feeling a sudden jerk and a case of tariff whiplash coming on, you’re not alone.

The unexpected nature of Trump’s latest wrinkle on tariffs is doing a number on the overall marketplace. And steel is no exception, causing reactive changes in pricing and buying, even if they might lack fundamentals.

First, a look in the review mirror

We saw this play out once already. Momentum accelerated at the start of the year, and the threat of tariffs ignited demand. In February, mills began pushing higher prices, supported by tariffs.

Hot-rolled (HR) coil prices responded, increasing by nearly $300 per short ton (st) in just about nine weeks. And lead times, which had been slipping and nearing 4.5 weeks, stretched out to about six weeks by early March.

But the bump was short-lived. Once buyers covered near-term needs, concerns shifted to uncertainty around some of those same tariffs. Buying tailed off, and demand pulled back. HR prices then ticked down $110/st over 10 weeks, and lead times decreased to 4.2 weeks, on average.

A case of déjà vu?

The Trump administration doubled Section 232 tariffs on imported steel to 50% on June 3.

We clearly saw an inflection point in our latest survey data with the announcement of a tariff “double-stack.” Yes, more uncertainty, mayhem, and some early panic buying have come because of higher tariffs on steel.

There’s been an immediate shift: Prices and lead times are up, mills stopped cutting deals, and buyers’ sentiment plummeted to near pandemic levels. But it’s all against the backdrop of a much softer market than what we saw during a previous Section 232 buying frenzy in Q1.

The steel roller coaster is indeed an up-and-down ride not made for the faint of heart.

Don’t just take my word for it. Check out the full results, available to premium members here. There’s a lot in there, so do go take a look. But I’ll mark some highlights with a sampling of comments from survey respondents.

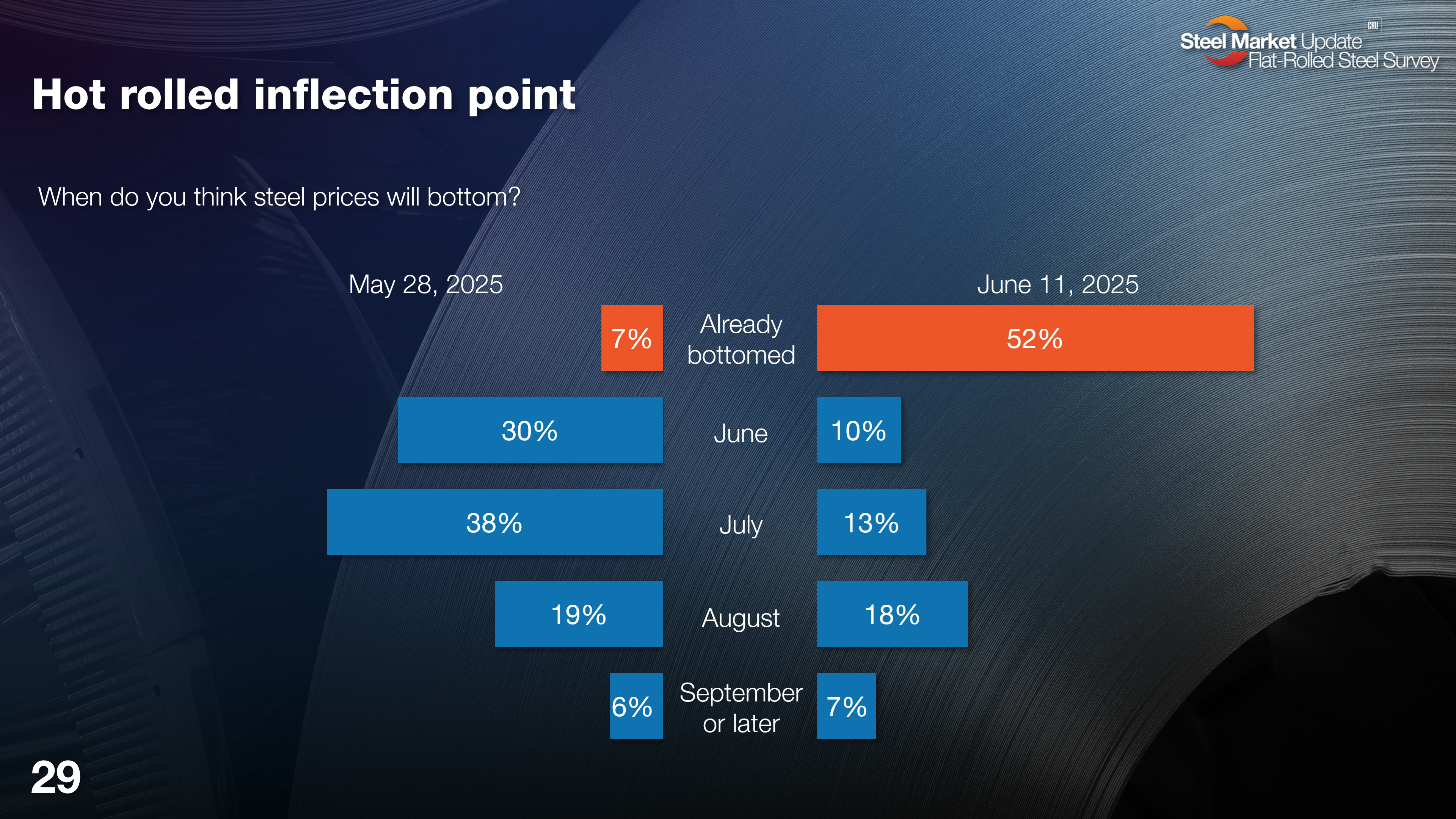

Survey says the bottom’s come and gone

Just two weeks ago, the wisdom of the crowd said that prices wouldn’t bottom until July or later. At the time, HR prices were averaging. $840/st. After the pricing whipsaw in the wake of doubled tariffs, more than half (52%) of survey respondents say we’ve already bottomed. There are still some, however, that might feel the lack of underlying demand may not support the present price shift.

(Editor’s note: You can click on any of the charts below to expand them. Note, too, that the numbers in the bottom left-hand side of the tables indicate which page you can find them on in the survey slide deck.)

Here is what some of them had to say:

“Tariff renewal just reset the new bottom until mills’ behavior blows things up.”

“Due to new tariffs, domestic prices are bound to increase.”

“Orders were placed over the last two weeks, but only pulling forward demand. Mills will struggle to fill their July order book.”

“I might be in the minority here, but I think pricing will still head lower from here. The 50% announcement was welcomed with a collective ‘shrug of the shoulders’ from the market.”

“The new tariffs changed the game – again.”

“Demand looks very soft, trade uncertainty won’t help.”

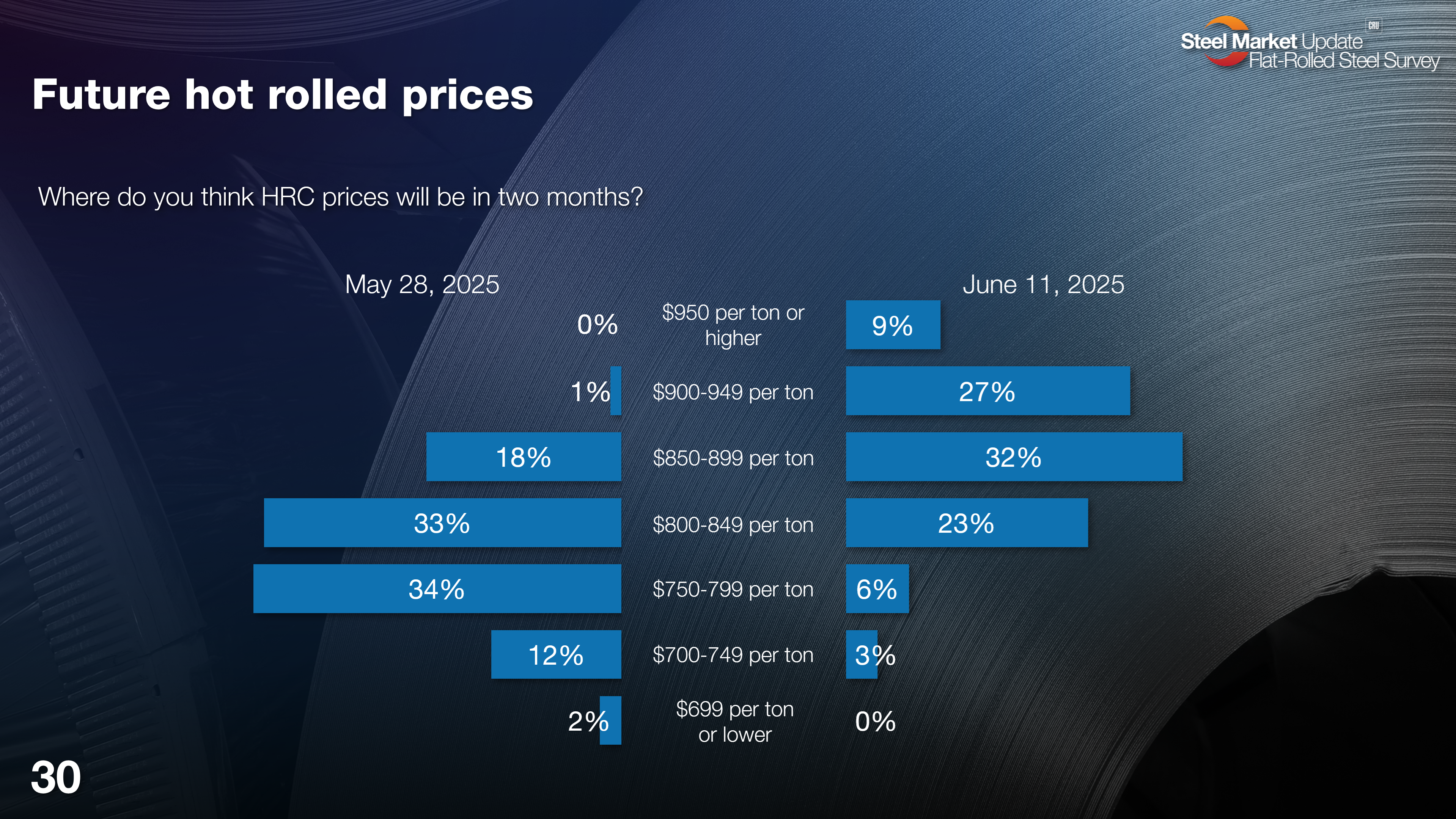

A pricing rally or hiccup?

While prices have responded to some recent and reactive buying, some think there’s room for a pricing rally, but most are not buying it.

A small minority (9%) of survey respondents think prices will exceed a recent high of $950/st from mid-March. More than a quarter think prices will see a run of more than $100/st over the next month or so. But still, more than half believe prices will be roughly where they are now come August.

A few comments:

“Tariff uncertainty and import curbs will provide the mills with sufficient leverage to keep pricing elevated.”

“Lack of competitive imports, especially from Canada and Mexico, will drive up prices.”

“The doubling of Section 232, I think, stopped the slide, but only for a while. Overall demand is still too poor out there.”

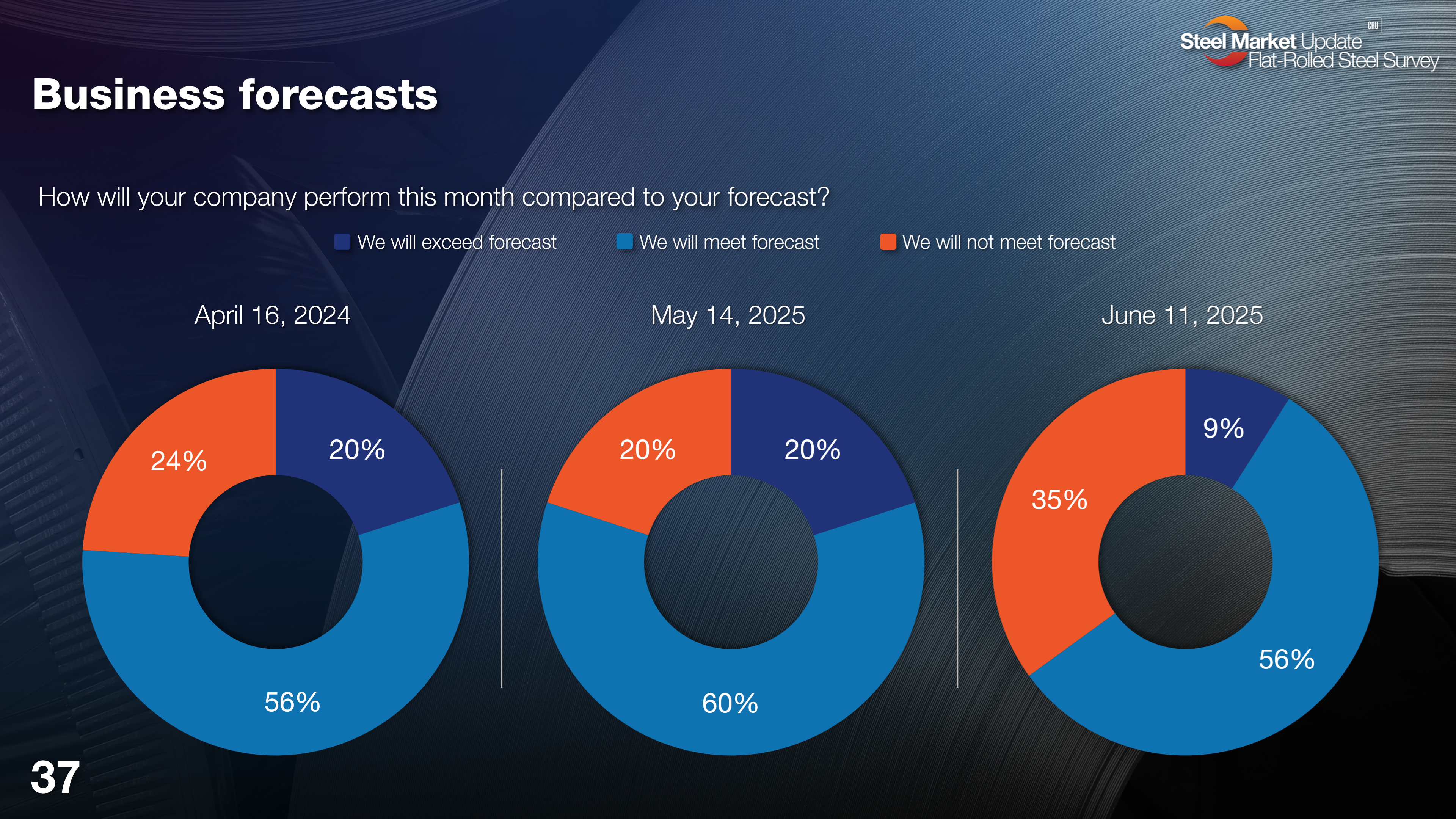

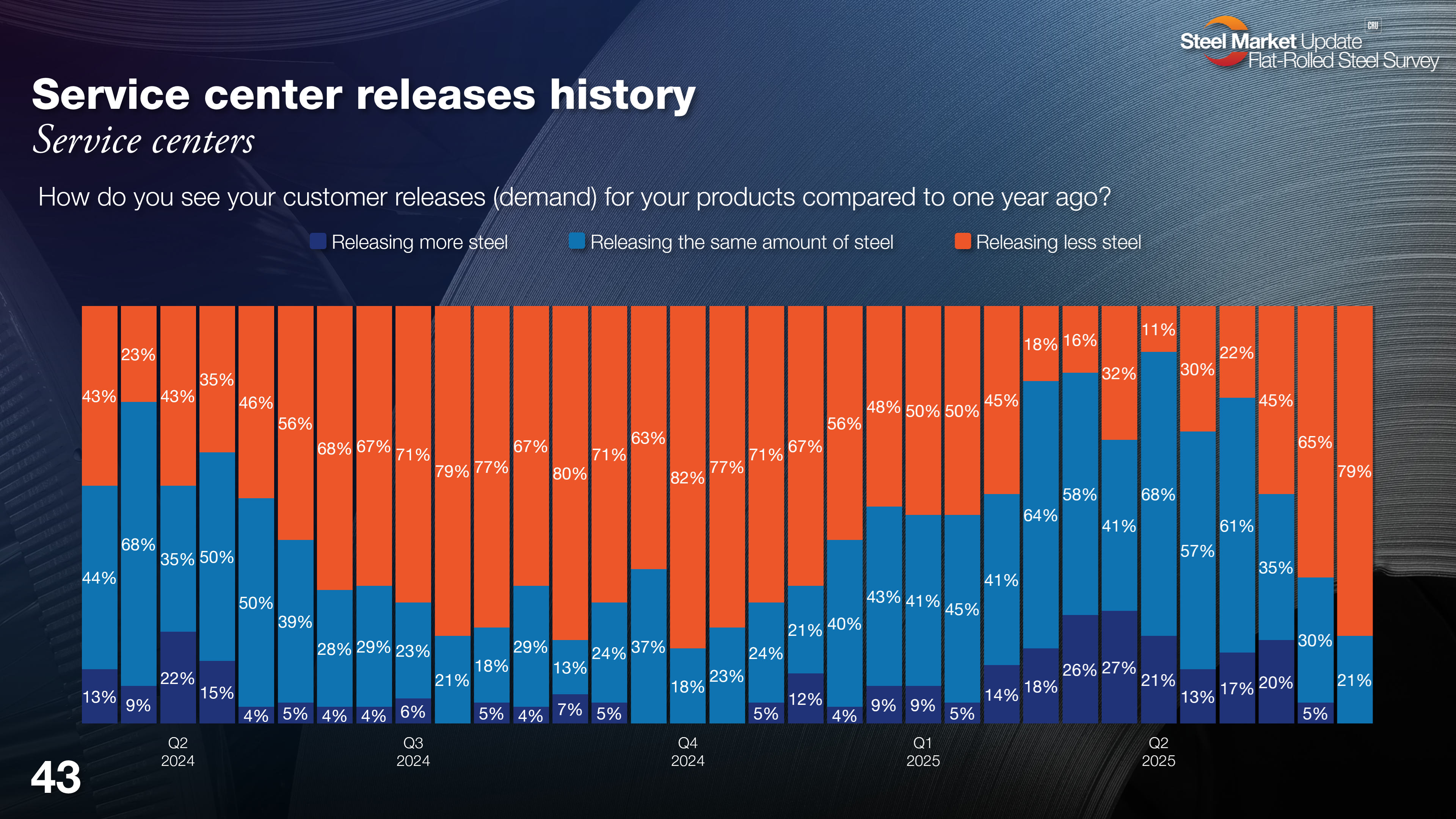

But are there cracks in the foundation?

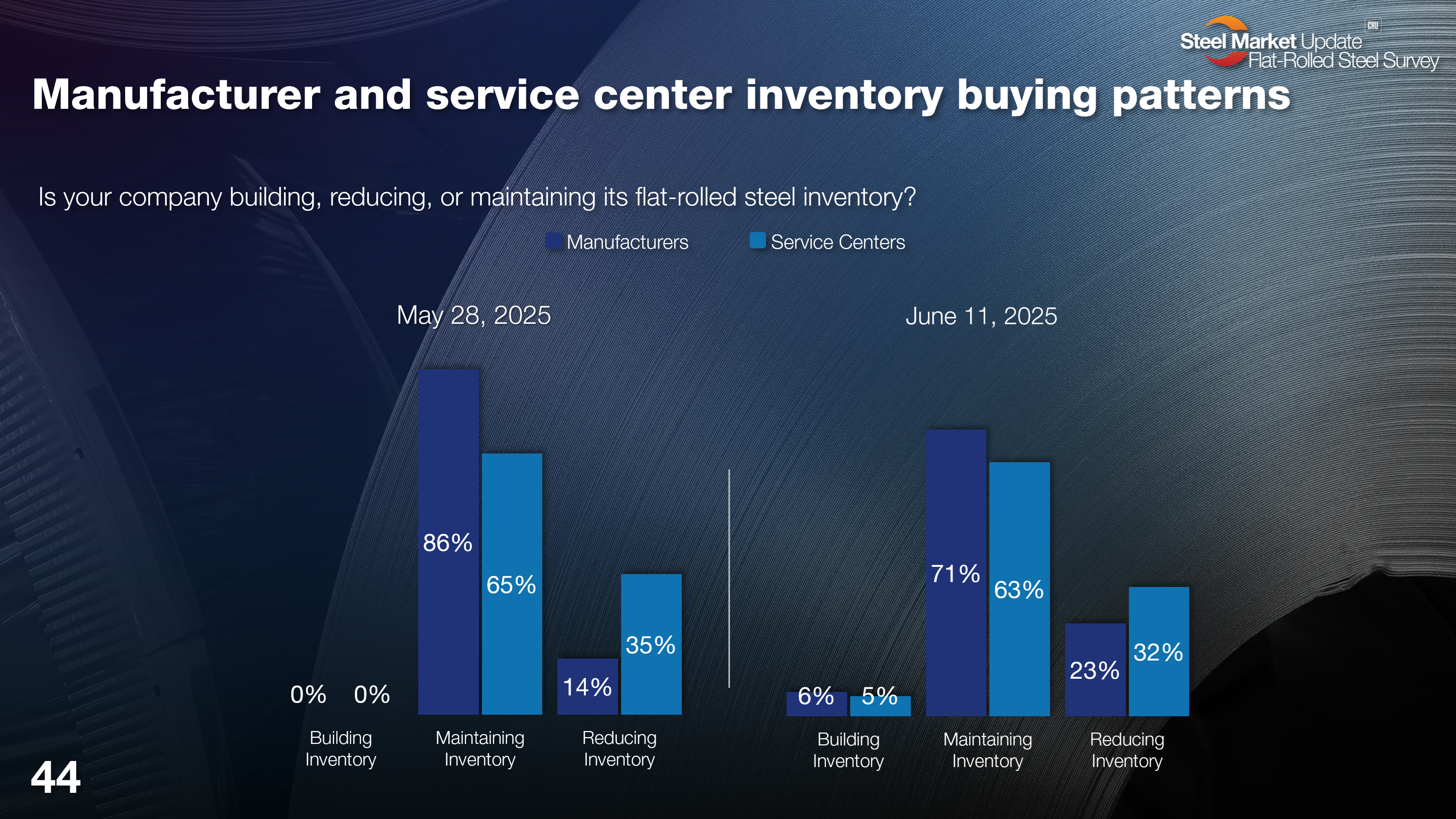

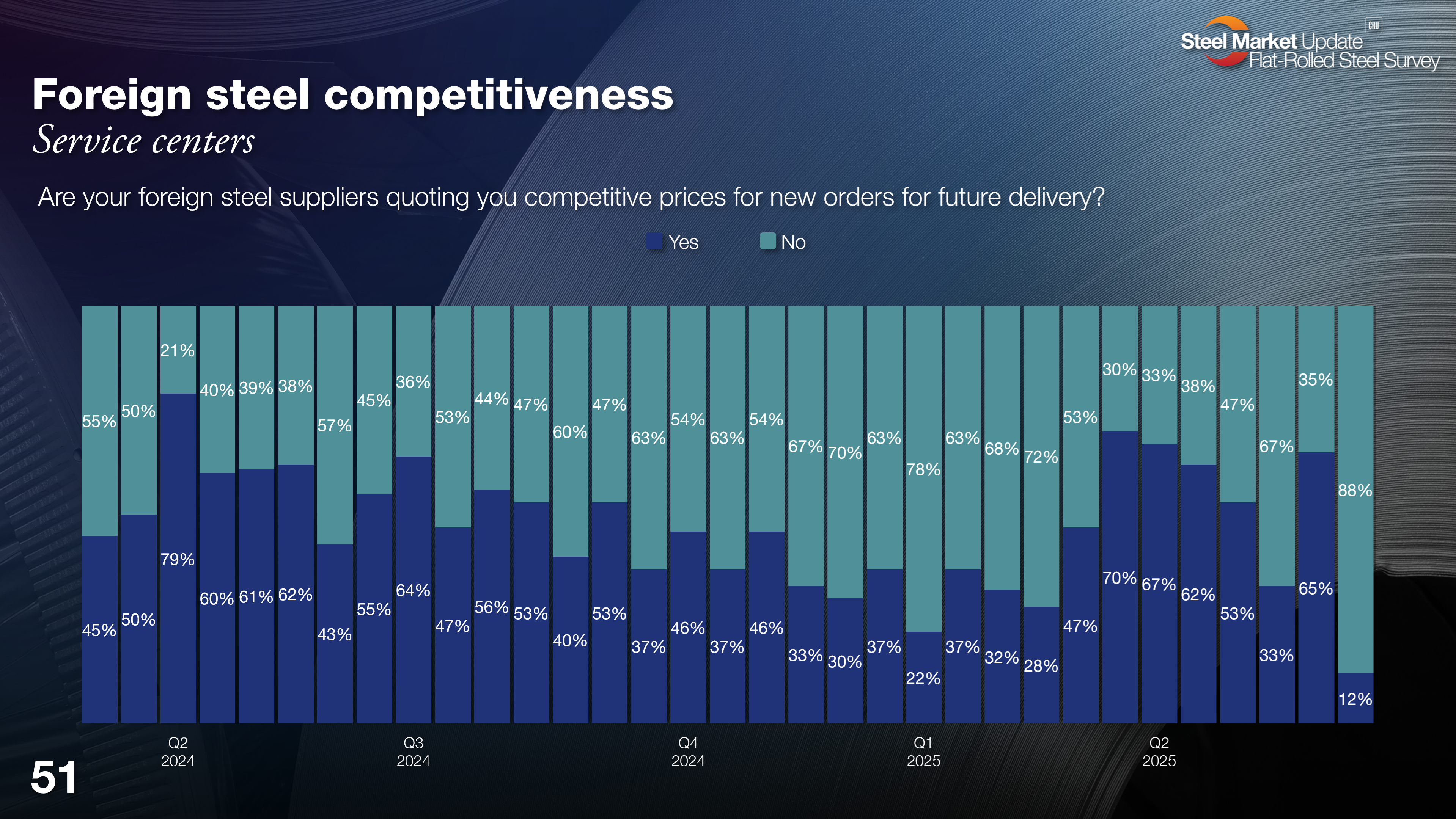

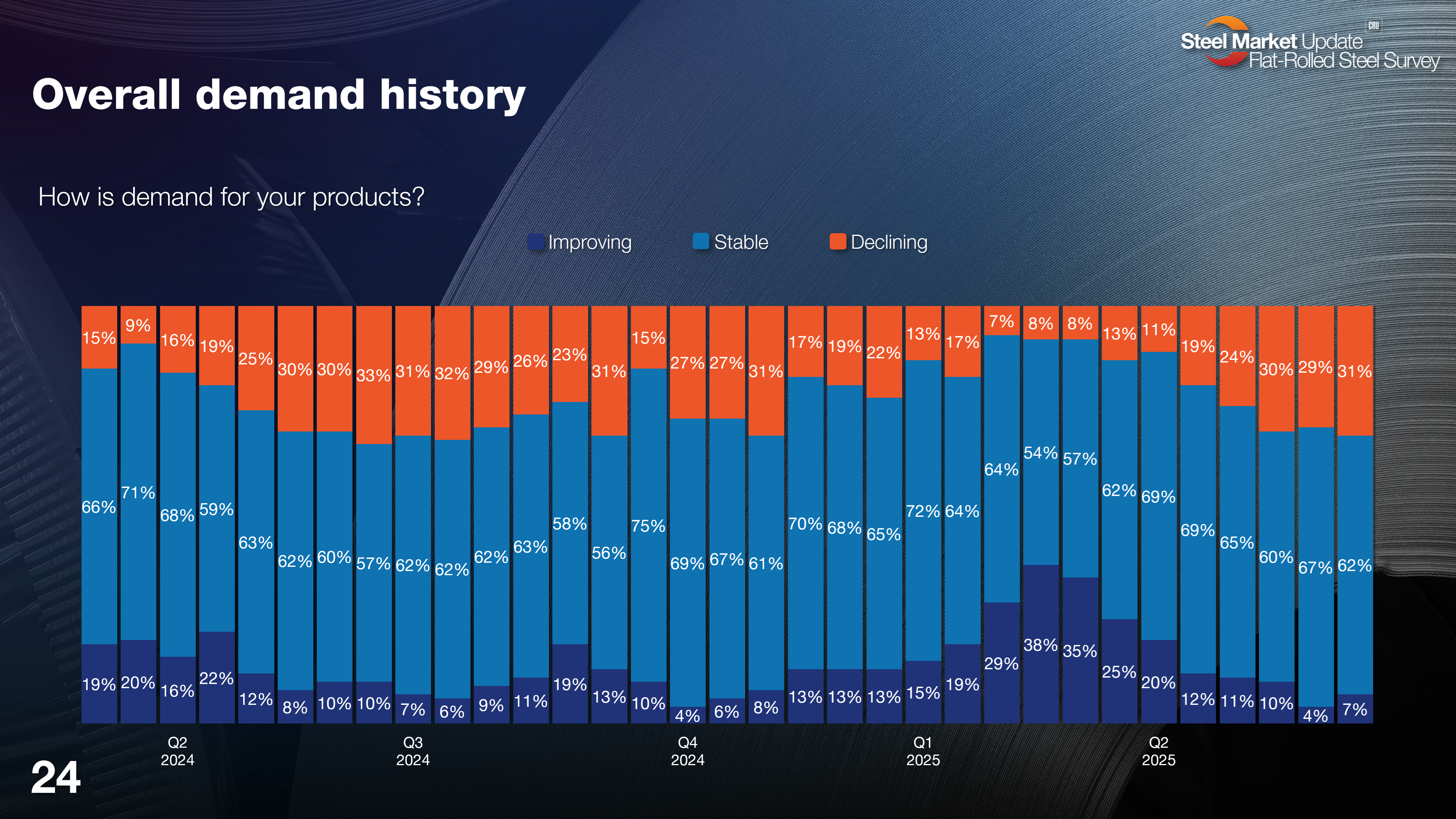

Despite the clear shift since the 50% tariff announcement, many aren’t meeting forecast, nearly 80% of service centers are releasing less steel than they were a year ago, and few are building inventory. All are detailed in the following three charts.

What else? Looks like there isn’t much import competition for now. Nearly 90% say imports aren’t competitive with the 50% Section 232 tariff. When it was 25%, most still said imports were competitive. And though it’s too early to tell, demand might be getting worse.

Still, it’s not clear if this could indeed be a sharp but extended price reversal. Still, should buyers really start building back inventories before the shock of 50% tariffs on imported steel in earnest hits the market, we could be in for another wild ride.

Time will tell, and we’ll know soon enough.