Prices

July 18, 2025

Steel buyers ignore tariff noise amid slow summer market

Written by David Schollaert

Steel sheet and plate buyers report feeling a bit dazed and confused amid a relentless tariff news.

Section 232 tariffs have doubled to 50%. Reciprocal tariffs rates remain uncertain. But while prices have softened on even softer sentiment, tariffs have firmed the floor.

Sheet buyers continue to report that mills are talking price. And even smaller quantities can draw aggressively lower offers from certain producers, they said.

Sheet market

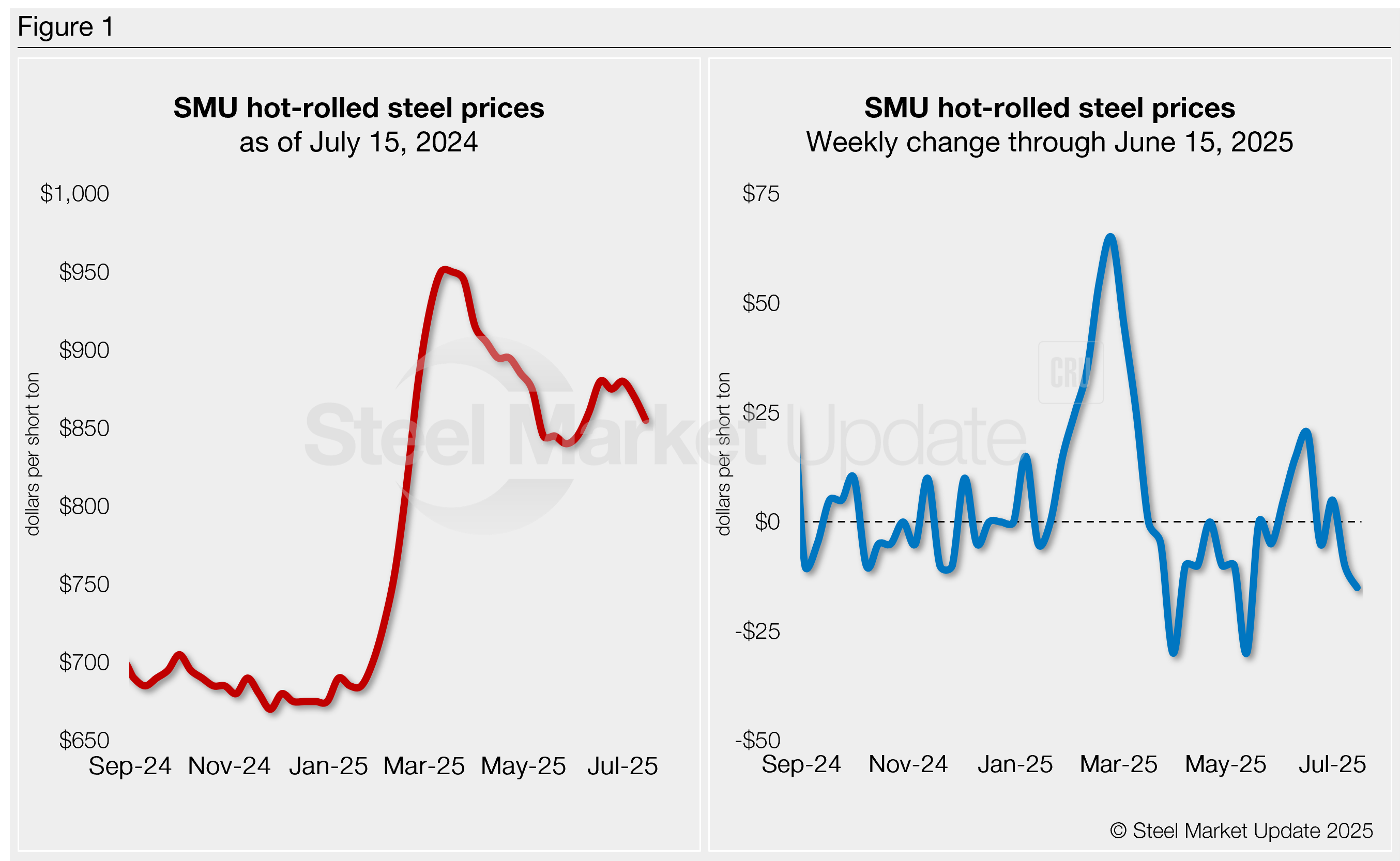

Section 232 tariffs at 50% are keeping imports out (for now). But they’re not sparking demand, sources told SMU. And while some sub-$800 per short ton (st) deals have been reported, the bulk of business remains in the low- to mid-$800s/st.

SMU assessed the spot price for domestically produced hot-rolled (HR) coil at $800-910 per short ton (st), with an average $855/st as of Tuesday, July 15. Hot band is down $15/st vs. the prior week and down $25/st since the start of July.

Buyers and distributors said their biggest headache is not prices but a constant barrage of tariff news. Some said they’re increasingly trying to tune it out.

“Right now, all the tariff news is just background noise,” said a Midwestern distributor. “We’re following close with customers and just trying to stay lean.”

Service centers sources also reported keeping inventories lean in response to ongoing uncertainty around the economy and tariffs. And with the typical summer doldrums in effect, buyers are in no rush to place big orders.

The result: Prices have remained within a relatively narrow band despite huge fluctuations in trade policy (see Figure 1). Hot band prices have averaged roughly $860/st since May, according to SMU’s interactive pricing tool.

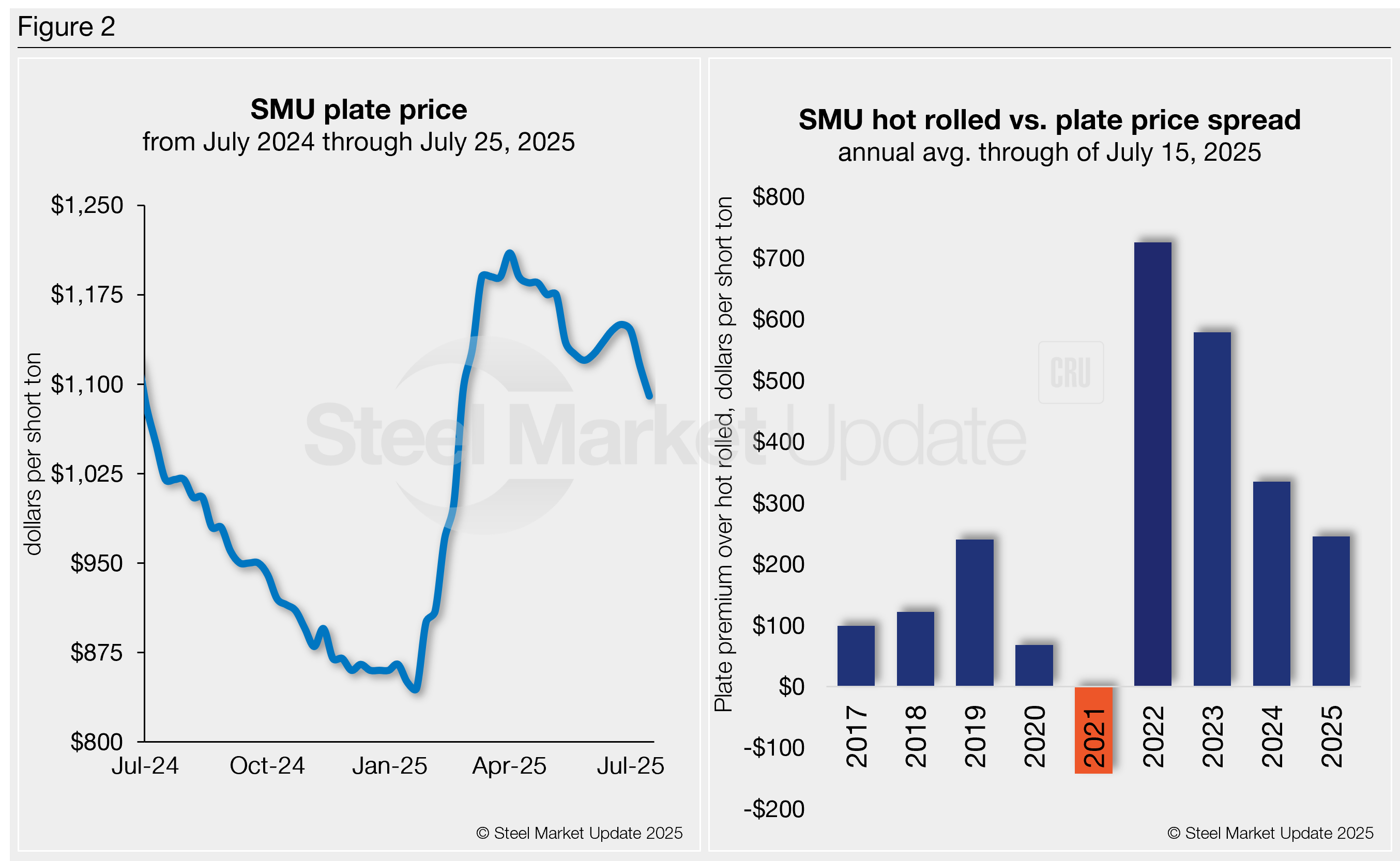

Plate market

Dynamics within the plate market have been similar to those in sheet. The consensus is that demand is tepid and there’s plenty of supply. Lead times have contracted, and order books have not filled as quickly as in past months.

While mills’ published prices have remained largely flat, buyers report continued discounting when it comes to actual transactions. Prices are generally about $150-200/st below mills’ list prices. And such steep discounts are available for even small spot tonnages, buyer sources said. They also noted big questions around demand.

SMU’s plate price stands at $1,090/st on average as of our Tuesday, July 15, check of the market (see Figure 2, left-side chart), down $25/st from the previous week. That marks the lowest level for plate prices since February. Prices have come off roughly $60/st over the past few weeks, per our pricing archives.

The average premium plate held over HR from 2017-2020 was $132/st. That all changed after the pandemic. The spread saw significant swings before ballooning to $970/st in the summer of 2022. It fell to a three-year low of $160/st in January. That spread has since started to widen but remains closer to pre-pandemic norms (see Figure 2, left-side chart).