Analysis

July 27, 2025

Final Thoughts

Written by Michael Cowden

We had “Liberation Day” in April when President Trump first announced his “reciprocal” tariffs on other nations. And now we’re approaching what some of you are calling “Perspiration Day” – the Aug. 1 deadline that could see reciprocal tariff rates ratcheted up significantly for some nations.

Section 232 tariffs of 50% on imported steel and potential tariffs of 50% on metallics from Brazil have resulted in higher prices. Case in point: SMU’s hot-rolled (HR) coil price stands at $845 per short ton (st) on average. That’s $210/st above where we were in late July of 2024, according to our pricing records.

But while prices might be relatively high, lead times are short. And buyers tell us that mills are willing to negotiate lower prices to bring in spot business. In fact, what we call the mill negotiation rate is the highest in our 13-year history for that data series. (You read that right. Buyers say mills are more willing to negotiate lower prices now than they were during the pandemic in 2020.)

So, is this just a severe case of the summer doldrums? Will demand improve in the fall, as it often does? Or has uncertainty around tariffs and the economy created a more lasting impact?

Tariffs remain unpopular among steel consumers

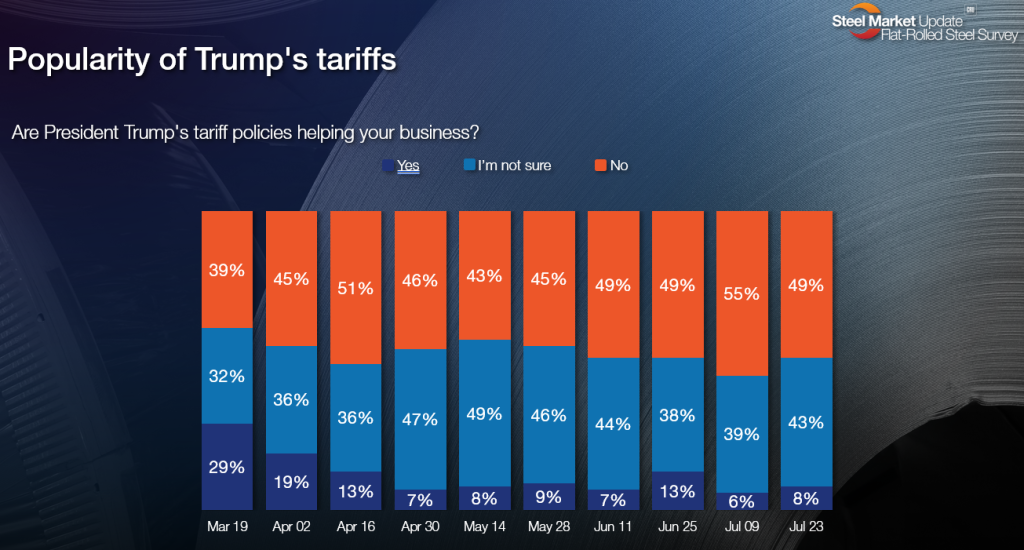

Some important steel and steel-related trade groups have come out in favor of Trump’s tariffs. But they remain broadly unpopular among steel buyers, according to our survey results.

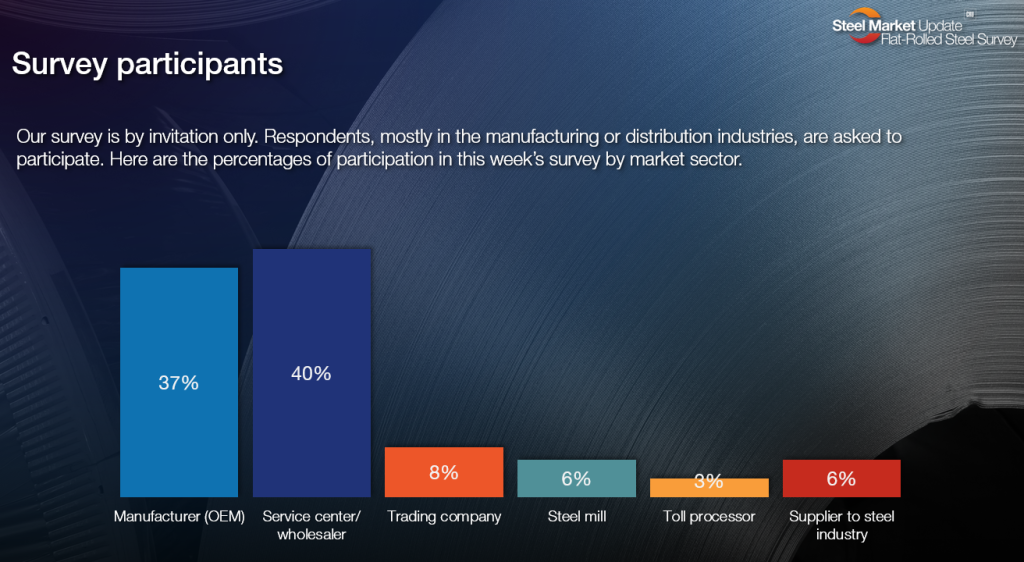

Let me first reiterate that point: Most of the people who participate in our surveys are steel buyers or steel consumers, as you can see in the chart below. So our results primarily represent their perspective.

(Editors note: All of the charts below come from our steel market survey. You can click on them to expand them. And you can find the full results of that survey here.)

As you can see in the next chart, Trump’s tariffs have only single-digit support among the people we survey – a result that has been fairly consistent since “Liberation Day” on April 2. Most people are either unsure of the impact of tariffs or say that they are hurting their business.

“Unprecedented” was the word that dominated survey results following the pandemic and Russia’s full-scale invasion of Ukraine. “Uncertainty” has become the word we hear again and again when it comes to Trump and tariffs.

Here are thoughts on the tariffs from some of our survey participants in their own words.

Let’s start with the few who think tariffs are helping their business:

“We are starting to see the effects of buyers resourcing many of their tube products due to tariff costs. Others have commented directly that they will be making parts – replacing parts they have been buying in China.”

“Onshoring continues, both in practice and in inquiries.”

“They’re hurting our competitors more.”

Here are comments from some of those who aren’t sure of the impact of tariffs on their businesses:

“They helped earlier in the year as the value of our inventory increased. But the uncertainty created by the trade negotiations appears to have negatively impacted demand.”

“Too early to really see what will come of it all.”

“To be determined.”

And, finally, here some comments from those who say tariffs are not helping their business. They were the most vocal group.

“The steel tariffs will allow U.S. mills to increase price. My Canadian mill more or less cancelled our 2025 agreement – stating they cannot eat the tariffs at 50%. It’s getting very real.”

“Increasing price and reducing business.”

“The policies create uncertainty, raise prices, and limit supply options.”

“They are hurting our business. Making our aluminum the highest priced in the world. This is not how you reshore manufacturing.”

“They are terrible and hurting our business.”

“A lot of uncertainty.”

“Hurting Canadian operations, and sales to US market are down.”

“They’ve created too much unease and uncertainty out there. We all like certainty, which we haven’t had for a loonngggg time.”

“Too much fluctuation for people to make decisions.”

“So far, based on less sales vs. ’24, I’d have to say they’re not yet helping our business.”

Then is what I’d almost call a separate subcategory – companies who say tariffs are hurting their business now but who expect benefits from tariffs later. Here are some comments from them:

“The tariffs are causing challenges now with the uncertainty they are creating. But we feel they will help us in the future.”

“Uncertainty in the short-term is difficult. Long-term they will be beneficial – but we need some demand to spark it.”

Stable prices amid uncertainty

I’ll turn to demand in a minute. But let’s first see where our survey respondents think prices will be in two months.

It’s summer. Lead times for hot-rolled are still in August. That’s true for some producers even when it comes to cold-rolled and coated lead times. And you tend to see discounting until lead times get more solidly into September.

We saw prices drop into the $500s/st for larger buyers this time last year. And there had been expectations in the spring that we might see something similar this year. (That said, the 2025 version was worried about HR falling into the low $700s/st.)

But the outlook for prices remains remarkably stable despite widespread concern about demand and tariffs.

Most survey respondents think sheet prices (I’m using HR as a proxy for other sheet products) will be roughly where they are now in the fall. Maybe a little higher or a little lower, depending on who you ask.

No one is predicting that prices will shoot above $1,000/st, which was a common response in Q1. Nor is anyone predicting that prices will fall into the low $700s/st, which was a common response before Trump announced 50% Section 232 tariffs in late May.

Here is what some of those respondents had to say:

$900-949…

“Inventory will become low, and customers will have to buy domestic and pay higher prices.”

“Lack of imports and increase in demand second half.”

“50% tariffs on Brazil (pig iron, etc.) will put upward pressure on steel prices.”

$850-$899…

“Domestic producers will run full as they displace imports.”

“Scrap prices will begin to push up spot prices in the next 30 days.”

“Higher tariffs and higher raw material costs should hold it up.”

$800-$849…

“Demand is not as good, and the mills will have to fill their August order book. However, that may change if scrap comes in as high as some think it will.”

“No great demand in the market right now.”

“Tariffs may influence pricing, but demand is still low – which makes pricing stable.”

$750-799…

“Supply imbalance, more capacity coming, lack of discipline on discounting.”

“We heard rumors of an increase that never materialized. We just view this market as pretty darn bleak.”

“Very weak demand.”

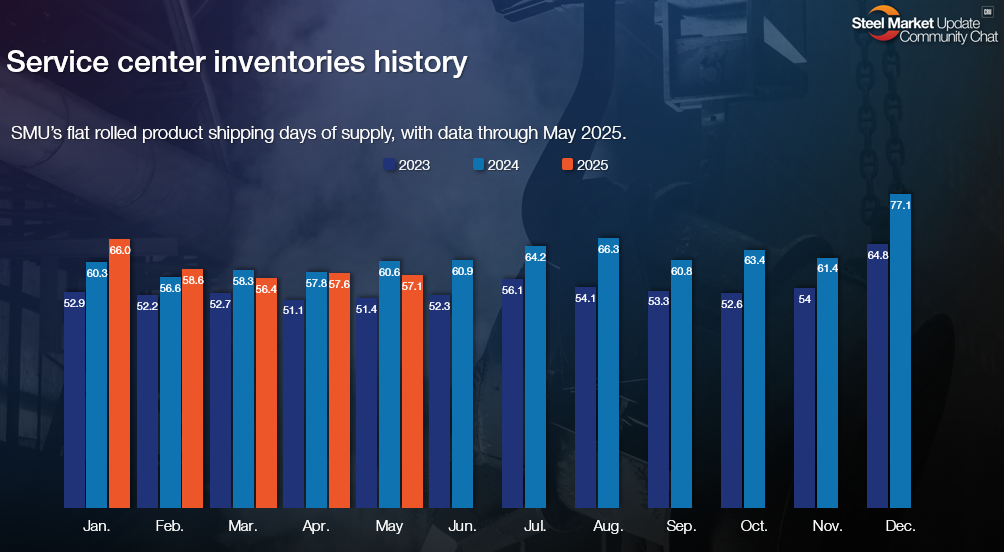

We’ve got survey data to support most of the arguments above. We saw that sheet inventories continued to tick lower in June – as you can see in the chart below.

We won’t release July data until Aug. 15. But I wouldn’t be surprised if inventories continue to move lower based on results like this.

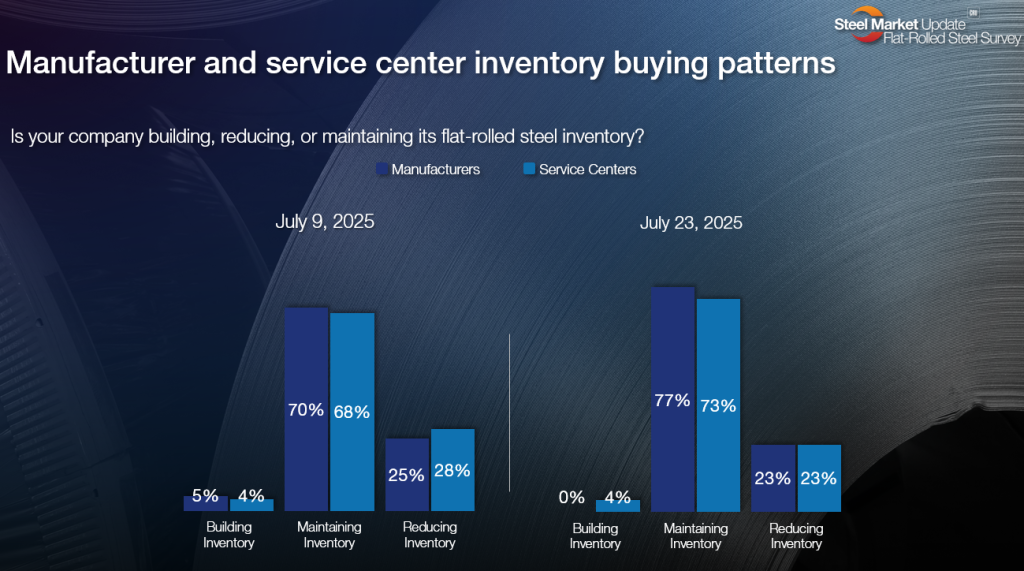

As you can see, more people are maintaining inventories, about 20-30% are reducing them, and very few are building stocks.

Meanwhile, imports are down. We saw flat-rolled steel imports in June hit some of the lowest levels since 2020 and the pandemic. While data for July isn’t complete, it doesn’t look like we’re set for an uptick this month, according to government figures.

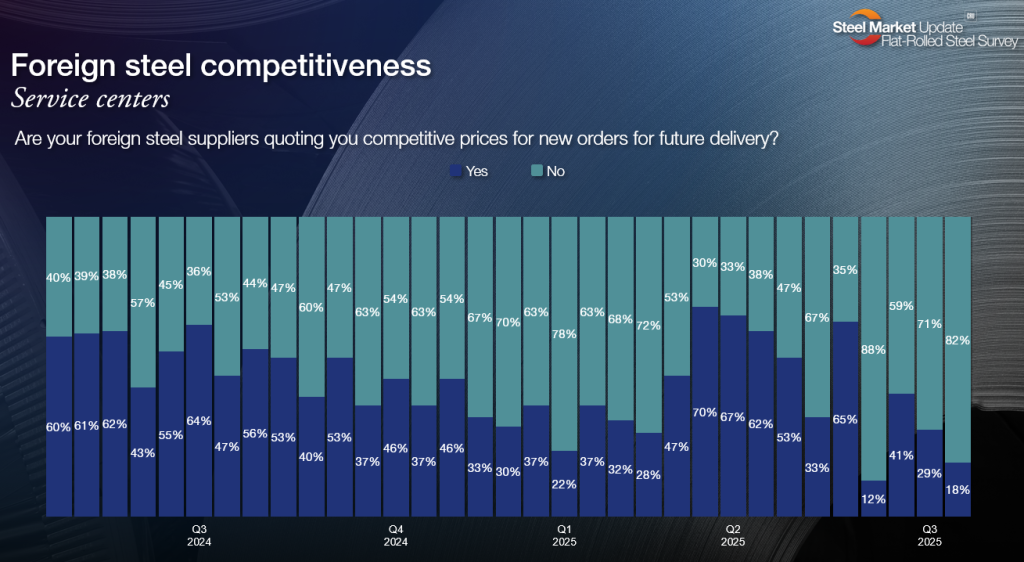

And I’d be surprised if imports increased much in late summer or fall with so many service center respondents telling us that import prices aren’t competitive:

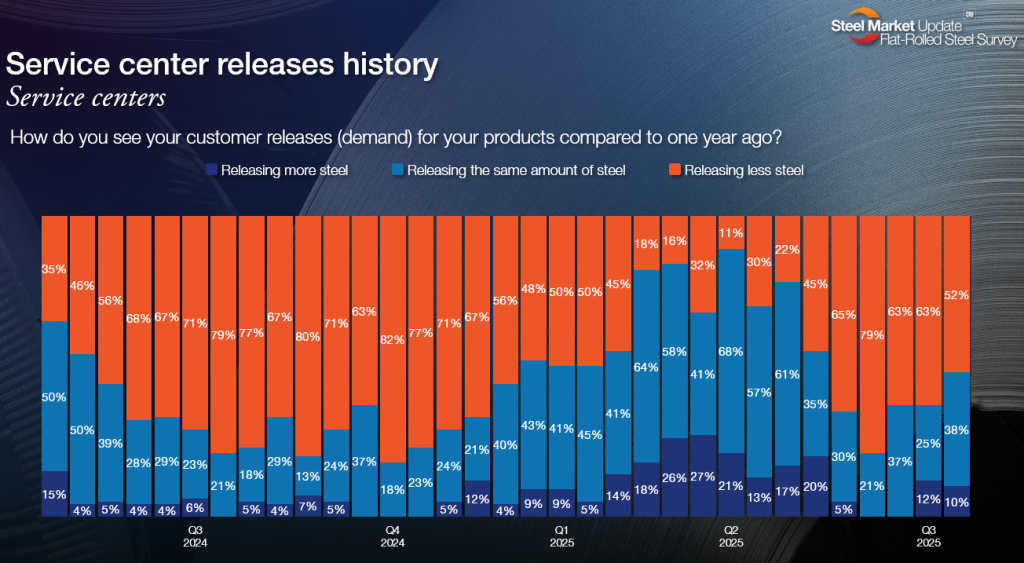

But, again, what about demand? Most service centers continue to tell us that they’re releasing less steel than a year ago. (And recall that last July was not a great time for steel.)

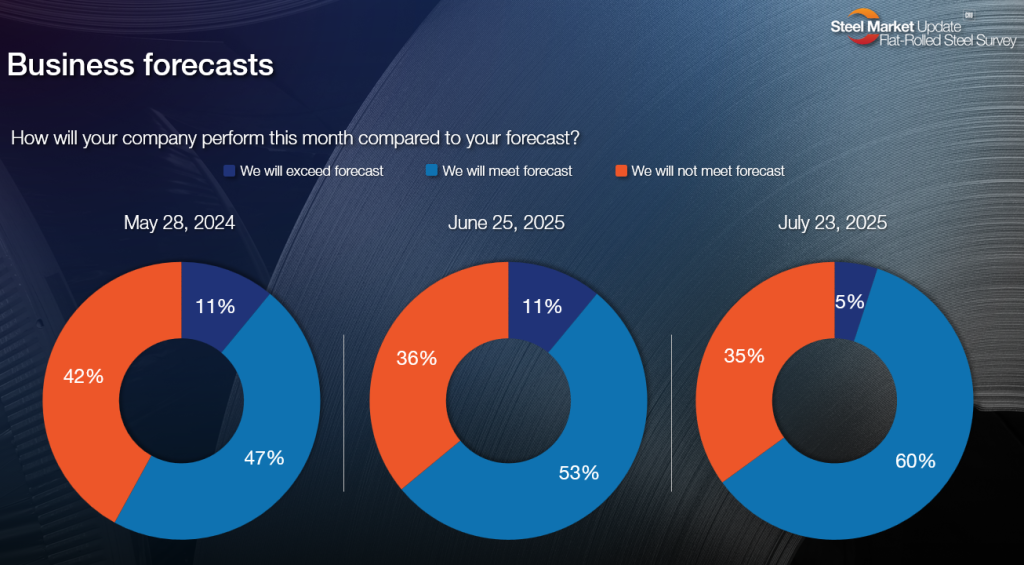

And while most people tell us that they’re meeting forecast, a significant numbers (~35-40%) in recent months tell us that they’re missing forecast.

Again, maybe we’re all wringing our hands too much about the summer doldrums. And maybe the tariff-related uncertainty will clear as more trade deals are hammered out. Or at least as people come to realize that tariffs are here to stay and find a playbook to match that new reality.

I’d like to think that lead times getting past Labor Day are the spark we need to see improved activity. And then there are the usual seasonal patterns. Demand typically improves in the fall just in time for mills to take fall maintenance outages, which should bolster prices.

We saw prices bump along a bottom for much of 2H’24. I’d like to think this year will be different. I wish I had more confidence in that conclusion. But one thing seems clear – even if demand doesn’t improve, tariffs have raised the floor for steel prices.

What about you? What do you think? You can let us know at info@steelmarketupdate.com. Or you can participate in our next survey. If you already participate, we truly appreciate your feedback. If you don’t, contact my colleague David Schollaert at david@steelmarketupdate.com. He can get you signed up.

SMU Steel Summit

We’re less than a month away from Steel Summit. And already nearly 1,200 people have signed up to attend.

You can see a list of the companies attending here. And you can check out the latest agenda here.

We were thrilled to announce last week that U.S. Steel President and CEO David Burritt will be speaking at event. He joins a list of executives, economists, and steel industry veterans who I’m sure you’ll learn a lot from.

We’ll also leave plenty of time for networking with 1,500 or so of your best friends in steel. If you haven’t signed up for one of the biggest events on the steel calendar, what are you waiting for? You can register here.