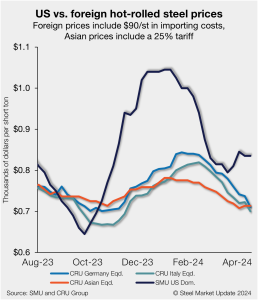

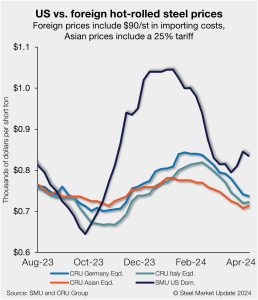

Cliffs to post monthly spot HR price, starts with $850/ton

Cleveland-Cliffs said its base spot hot-rolled (HR) coil price will be $850 per short ton (st) with the opening of its June order book. The company made the announcement in a press release and in a letter to customers on Friday.