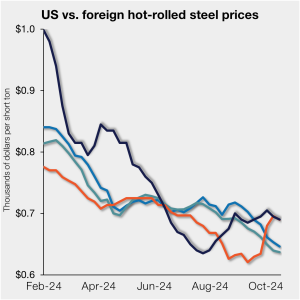

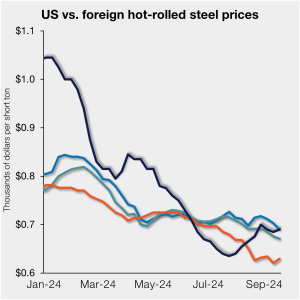

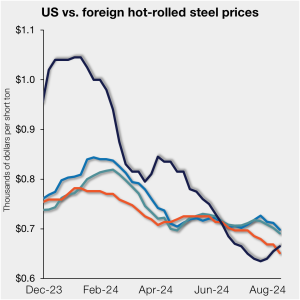

US, offshore HR prices trend lower together

US hot-rolled (HR) coil prices slipped again this past week, mirroring movement in offshore markets. This kept domestic tags marginally higher than imports on a landed basis.

US hot-rolled (HR) coil prices slipped again this past week, mirroring movement in offshore markets. This kept domestic tags marginally higher than imports on a landed basis.

Steel sheet prices mostly edged lower for a second week, while plate prices slipped for the third consecutive week.

After holding its weekly spot price for hot-rolled (HR) coil steady for three weeks at $730 per short ton (st), Nucor lowered the price this week by $10/st.

August steel imports totaled 2.38 million short tons (st) according to final data released this week by the US Commerce Departmen

US hot-rolled (HR) coil prices slipped this past week but remain marginally higher than offshore material on a landed basis.

Nucor’s consumer spot price (CSP) for hot-rolled (HR) coil is unchanged this week at $730 per short ton (st).

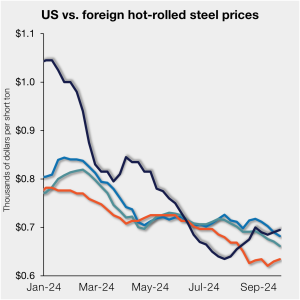

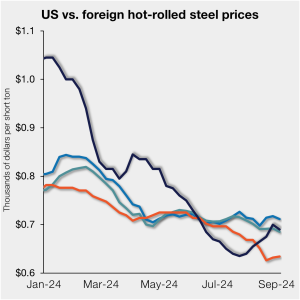

US hot-rolled (HR) coil prices moved slightly higher again this past week but remain marginally higher than offshore material on a landed basis. Since reaching parity with import prices in late August, domestic prices have been slowly pulling ahead of imports. This has been driven by a slight deviation in price movements – slow but […]

Nucor is holding its hot-rolled (HR) coil consumer spot price (CSP) at $730 per short ton (st) this week.

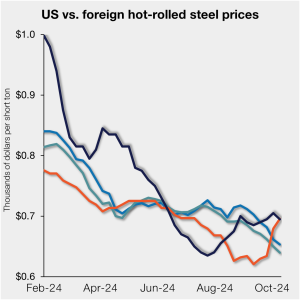

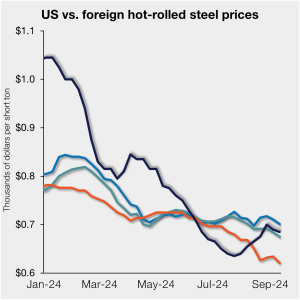

US hot-rolled (HR) coil prices inched up again this past week but remain just a touch more expensive than offshore material on a landed basis.

SMU’s steel price indices were mixed this week as the market seeks direction. All of our indices have fluctuated within relatively narrow ranges across September.

Nucor’s weekly consumer spot price (CSP) for hot-rolled (HR) coil increased $10 per short ton (st) from last week to $730/st as of Monday, Sept. 23.

The premium galvanized coil prices carry over hot-rolled (HR) coil continues to shrink, according to SMU price indices.

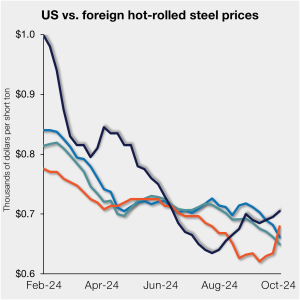

US hot-rolled (HR) coil prices edged up this past week and remain modestly more expensive than offshore material on a landed basis. Since reaching parity with import prices in late August, domestic prices have been slowly pulling ahead of imports. The move has been driven largely by declines overseas.

Cleveland-Cliffs is seeking $750 per short ton (st) for hot-rolled coil. That’s $20/st above where the steelmaker had been. It’s also $30/st above Nucor, which is at $720/st this week. We've seen prices increase incrementally this week. SMU's HR price, for example, stands at $690/st on average, up $5/st from last week. The questions now are whether a number well above $700/st will stick, whether other mills will follow Cliffs, and whether there is enough demand to support higher prices.

Cleveland-Cliffs aims to increase prices for hot-rolled (HR) coil to $750 per short ton (st) effective immediately. The move represents a price hike of $20/st from the Cleveland-based steelmaker's previously published price of $730/st.

Steel Dynamics Inc. (SDI) expects lower third-quarter earnings on the heels of “meaningfully lower” prices at its flat-rolled steel operations. The Fort Wayne, Ind.-based steelmaker expects Q3’24 earnings of $1.94 to $1.98 per diluted share, according to figures released on Monday. That’s down from $2.72 per share in Q2’24 and down from $3.47 per share in Q3’23.

Nucor’s weekly consumer spot price (CSP) for hot-rolled (HR) coil is unchanged from last week.

The price spread between hot-rolled coil (HRC) and prime scrap widened again in September, according to SMU’s most recent pricing data.

US hot-rolled (HR) coil prices edged down slightly this past week but remain at a slight premium to offshore material on a landed basis.

SMU’s steel price indices showed mixed signals for a second consecutive week. Our hot rolled, cold rolled, and plate price indices inched lower from last week, as the galvanized index held steady and Galvalume's ticked higher.

Nucor has raised its weekly consumer spot price (CSP) by $10 per short for hot-rolled (HR) coil to $720/st.

US hot-rolled (HR) coil prices were largely flat over the past week, remaining higher than tags for offshore material on a landed basis for a second consecutive week.

SMU indices moved higher on cold rolled products this week, while galvanized prices were flat. Our indices for plate, hot rolled, and Galvalume all edged lower.

Dan Needham has been with Nucor for 24 years, and he said the key to that longevity has been the company’s culture.

The price spread between hot-rolled (HR) coil and prime scrap widened slightly in August but remains in territory not seen since late 2022, according to SMU’s most recent pricing data.

Sheet prices trended sideways to modestly up this week in a market that appears to be in “wait-and-see” mode.

Fall is coming in North America, and with it, steel mills' regularly scheduled fall maintenance outages.

Steel buyers continue to report short mill lead times for both sheet and plate products, according to SMU's latest canvass of the market. Lead times for hot-rolled and plate products marginally increased from our late July survey, likely due to limited restocking in anticipation of upcoming mill outages for scheduled maintenance.

US hot-rolled (HR) coil prices are nearly even with prices for offshore material on a landed basis as domestic tags continue to inch up.

The European Commission has initiated a trade case investigating allegedly dumped hot-rolled coil imports from Egypt, India, Japan, and Vietnam. The European Steel Association (EUROFER) filed the complaint in June, according to an Aug. 8 notice in the Official Journal of the European Union.