CRU aluminum news roundup

A roundup of aluminum news from CRU.

A roundup of aluminum news from CRU.

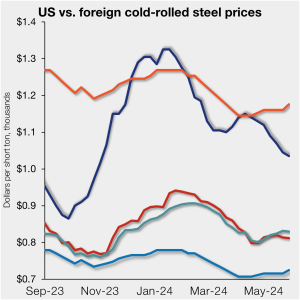

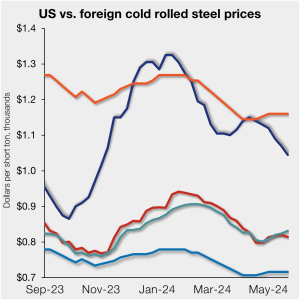

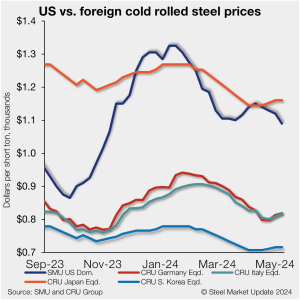

Offshore cold-rolled (CR) coil prices remain significantly cheaper than domestic product. That remains the cause even as US CR coil prices continued to tick lower. All told, US CR prices are now 17.6% more expensive than imports. While still high, that premium is down from 19.4% last week and down from 31.5% in early January.

Steel sheet prices across most regions of the world were little changed this week. European buyers remain cautious regarding their outlook towards end-use demand and largely remained out of the market. A similar trend was seen across Asia, although skepticism on real estate stimulus measures in China led to w/w price falls. In the US, […]

Week over week, the futures curve saw minimal change.

Steel imports jumped from March to April and are looking nearly as strong for May, according to updated Census data released earlier this week.

The US OCTG Manufacturers Association (USOMA) announced that the US Customs and Border Protection (CBP) agency made an initial affirmative determination of duty evasion practices.

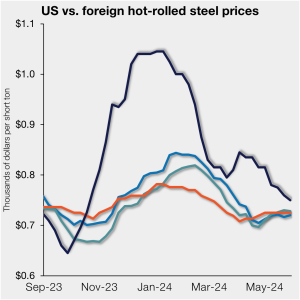

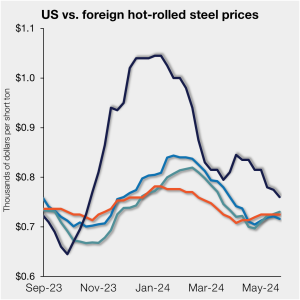

US hot-rolled (HR) coil prices ticked down further this past week, moving closer to parity with offshore hot band prices on a landed basis. This week, domestic HR coil tags were $750/st on average based on SMU’s latest check of the market on Tuesday, May 28.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to imports and evolving market chatter.

Sheet prices slipped again this week on a combination of moderate demand, increased imports, and higher import volumes.

Let's take a collective deep breath ::in:: and ::out::... And we're back. But where exactly are we? Are steel prices going up or down? Is demand really decelerating or is it an illusion? How is the market navigating the new mill pricing mechanisms?

In conjunction with President Biden’s visit to Vietnam in September 2023, Vietnam’s government petitioned the US Department of Commerce (DOC) for “market economy” treatment. This would be a major trade concession, as DOC has recognized for years that Vietnam’s economy does not operate according to market principles. However, graduating Vietnam to market economy status would […]

Here’s something I didn’t expect to see this week: SMU’s Current Buyers’ Sentiment Index dropped to its lowest point since August 2020.

Offshore cold-rolled (CR) coil prices remain a cheaper option over domestic product, even as US CR coil prices tick lower, according to SMU’s latest check of the market.

US hot-rolled (HR) coil prices declined again and now stand nearly even with offshore hot band on a landed basis.

Tenaris is blaming unfairly traded OCTG imports flooding the US market for its decision to lay off approximately 170 employees.

The CRU US Midwest hot-rolled (HR) coil index is a dominant and established price benchmark in the US. Many steel-buying contracts are linked to ‘the CRU,’ as it’s commonly called. But how does it work?

The free market operates best when it is freest. But all governments intervene in markets in response to conditions that threaten peaceful progress. President Biden decided last week that market intervention was justified. He approved a report from the US Trade Representative (USTR) that recommended continuing the “Section 301” tariffs on Chinese imports into the United States.

The USMCA should be strong enough to handle trade disagreements on steel between the US and Mexico, according to the American Iron and Steel Institute’s (AISI’s) Kevin Dempsey.

Non-refillable steel cylinder imports from India are subject to new antidumping and countervailing duties (AD/CVD).

President Biden announced an increase in tariffs this week on Chinese EVs, semiconductors, batteries, solar cells, steel, and aluminum.

The recent decline in US hot-rolled (HR) coil and longs prices has further restricted demand for imported material. Despite the decline in US sheet prices, CR coil and HDG imports remain attractive. While demand for imports of longs products has been limited, buyers have increased imports of wire products to avoid wire rods’ higher tariffs. […]

US hot-rolled (HR) coil prices saw further declines this week, while foreign prices were steady to slightly higher in the three regions we monitor

Following the announcement earlier this week that the US will hike import tariffs on Chinese goods, including steel and aluminum, Canada’s steel industry called on its government to consider similar tariffs.

SMU surveyed our market contacts this week about steel prices, demand, and the overall marketplace. Below are some of the buyers' responses in their own words to help you get a feel for current and future market conditions. Demand is a big topic of discussion currently. Is it steady, falling, or on the upswing with summer construction heating up? As you can see from the answers below, it depends on who you ask. One buyer’s response sums it up pretty well: “I still see the marketplace as soft/stable with some segments busy, while others tread water.”

Cleveland-Cliffs’ Lourenco Goncalves thinks trade measures announced by the US government on Tuesday against China were just the opening salvo in a series of trade actions. Case in point: The Biden administration targeted China’s “unfair” trade policies with additional tariffs on an array of Chinese-made goods - including steel, aluminum, and EVs.

Our spot price is little changed this week after moving sharply lower last week on the heels of Nucor’s unexpected price cut. Here’s one thought on that trend: Nucor's weekly HR price (aka, its “Consumer Spot Price” or CSP) has to date functioned almost more like a monthly price.

The Biden administration announced a series of actions on Tuesday targeting China’s "unfair" trade policies. These actions will, among other things, make imports of steel and aluminum from the Asian nation even more prohibitive.

What's the tea in the steel industry this week? Here's the latest SMU gossip column! Just kidding... kind of. Yes, some of the comments we receive in our weekly flat-rolled market steel buyers' survey are honestly too much to put into print. Some make us laugh. Some make us cringe. Some are cryptic. Most are serious. We appreciate them all. Below are some highlights from our survey results this week. Some of the comments that we can share with you are also included, in italics, in the buyers' own words, with minimal editing on our part.

Offshore cold-rolled (CR) coil prices remain much less expensive than domestic product, even as domestic prices have slipped to a six-month low, according to SMU’s latest check of the market.

The Mexican federal government backed down on the application of tariffs on raw non-alloyed and alloyed aluminum decreed on April 22.