Prices

May 30, 2019

Hot Rolled Futures: A "Tail" of Hope

Written by Gaurav Chhibbar

SMU contributor Gaurav Chhibbar is a partner at Metal Edge Partners, a firm engaged in Risk Management and Strategic Advisory. In this role, he and his firm design and execute risk management strategies for clients along with providing process and analytical support. In Gaurav’s previous role, he was a trader at Cargill spending time in Metal and Freight markets in Singapore before moving to the U.S. You can learn more about Metal Edge at www.metaledgepartners.com. Gaurav can be reached at gaurav@metaledgepartners.com for queries/comments/questions.

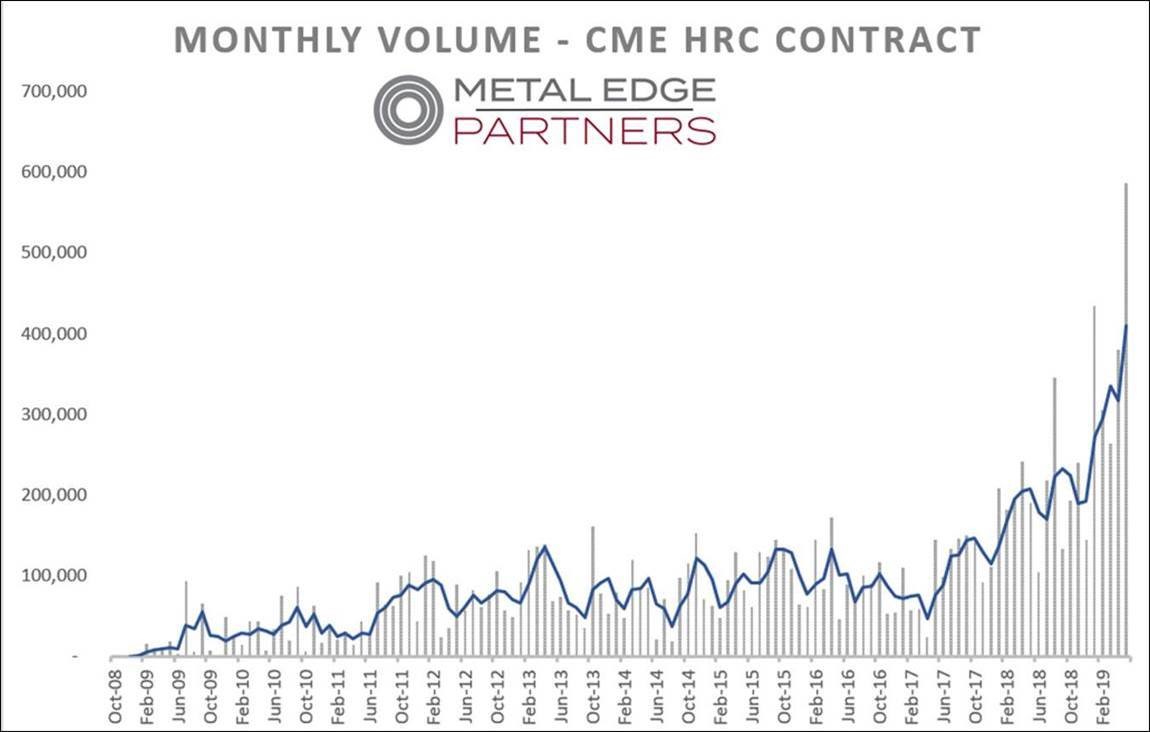

HRC Futures have seen a very active past few weeks (chart below). There are many trying to manage their steel exposure. There are participants hedging inventory risk, OEMs locking in forward pricing, traders rolling their short positions forward, etc. As uncertainty grows, there are manufacturers and stockists prudently reducing their naked long (or short) exposure.

*The month of May data is not complete yet, however the pace is indicating what might be the biggest month of exchange cleared trade.

In these four weeks, the picture on the shape of the curve has changed remarkably. The Q3 ’19 has lost considerable value as pressure on physical prices remains high. In a market with falling index level, the buyers of M-2 (July) are asking for a heavy discount! They anticipate further drops in the benchmark index. From the beginning of May to now the July contract has shaved over $60. This has pushed the curve into a steeper carry (contango) than just two weeks ago. The contango is reflective of near-term aggression in spot HRC prices, but also reflects the relative lack of offers for months further out. I call it the “tail of hope” where the market prices an expectation of a rebound.

As I’ve mentioned in the past updates, the futures market reflects the information that the market participants have or anticipate. So, what has changed in the past month that sellers got so aggressive on the spot? Tariffs on Turkey (excluding AD, CVD) have gone from 50 percent to 25 percent; Canada and Mexico don’t have to pay 25 percent from the Section 232 tariffs anymore; and buyers in the U.S. are sitting on the sidelines, reluctant to buy steel when they believe the price is likely to be cheaper tomorrow.

What is surprising is that this bearish sentiment for HRC is pervasive despite the international raw material market singing a different tune.

Iron ore prices continue to move higher squeezing mill margins in China. What this chart below fails to capture is the added pain the Chinese mills feel due to a stronger dollar and weaker RMB. As steel prices in China come lower and mills face a stronger dollar and higher ore, the margins deteriorate at a faster pace.

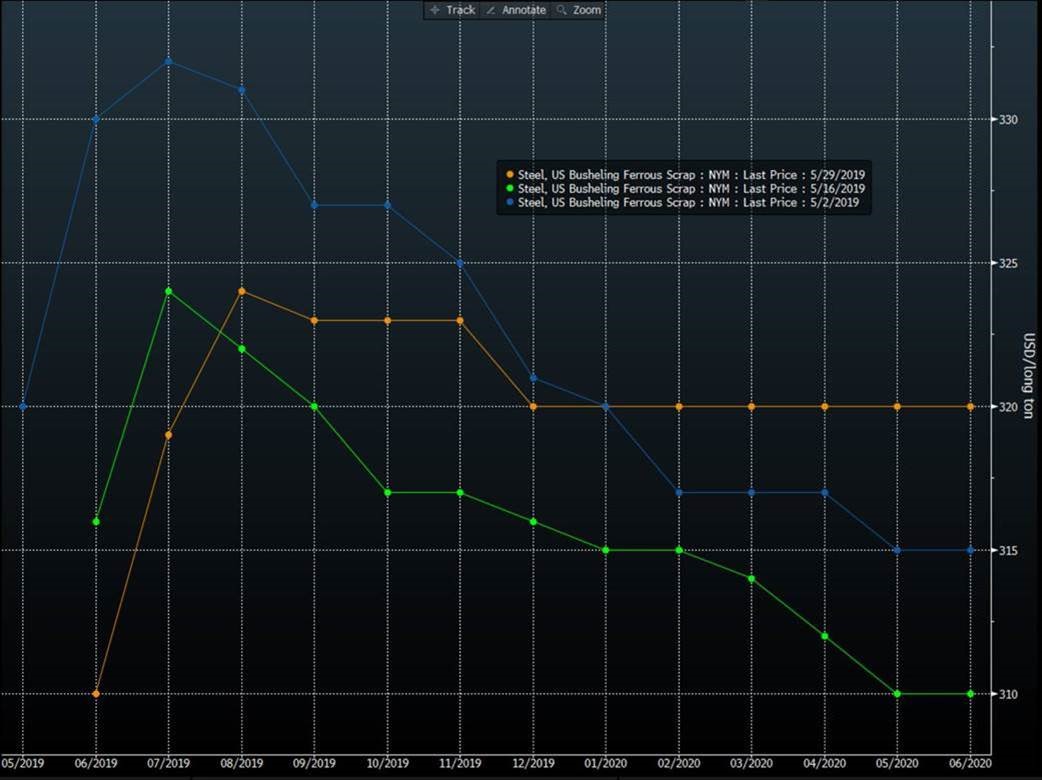

This situation in China (and Asia) has directed people’s attention to the relatively inexpensive price of scrap. Scrap prices took a beating in the U.S. in the last month of trading, however the futures curve now shows a recovery in the cards. This recovery in part is reflective of increased support for scrap as long as ore prices stay well bid.

Some of you have messaged us asking to include a strategy/guidance on what is the best move to make in any market. We unfortunately cannot make any suggestions without having a deeper look into your total business exposure. However, I will include some general to-do’s that are important for any good trading strategy going forward. For now, the best I could suggest is for people to identify pockets within your business where there exists any price risk. A good trading strategy does well to segment and classify price risks on the sales and purchases you make or plan to make.

Disclaimer: The information in this write-up does not constitute “investment service”, “investment advice”, or “financial product advice” as defined by laws and/or regulations in any jurisdiction. Neither does it constitute nor should be considered as any form of financial opinion or recommendation. The views expressed in the above article by Metal Edge Partners are subject to change based on market and other conditions. The information given above must be independently verified and Metal Edge Partners does not assume responsibility for the accuracy of the information