Prices

May 5, 2022

Hot Rolled Futures: Can Energy and Auto Save Us?

Written by Tim Stevenson

SMU contributor Tim Stevenson is a partner at Metal Edge Partners, a firm engaged in Risk Management and Strategic Advisory. In this role, he and his firm design and execute risk management strategies for clients along with providing process and analytical support. In Tim’s previous role, he was a Director at Cargill Risk Management. Prior to that, he led the derivative trading efforts within the North American Cargill Metals business. You can learn more about Metal Edge at www.metaledgepartners.com. Tim can be reached at Tim@metaledgepartners.com for queries/comments/questions.

Equity and bond market volatility has been getting a lot of attention these days. So how have HRC futures performed over the past week?

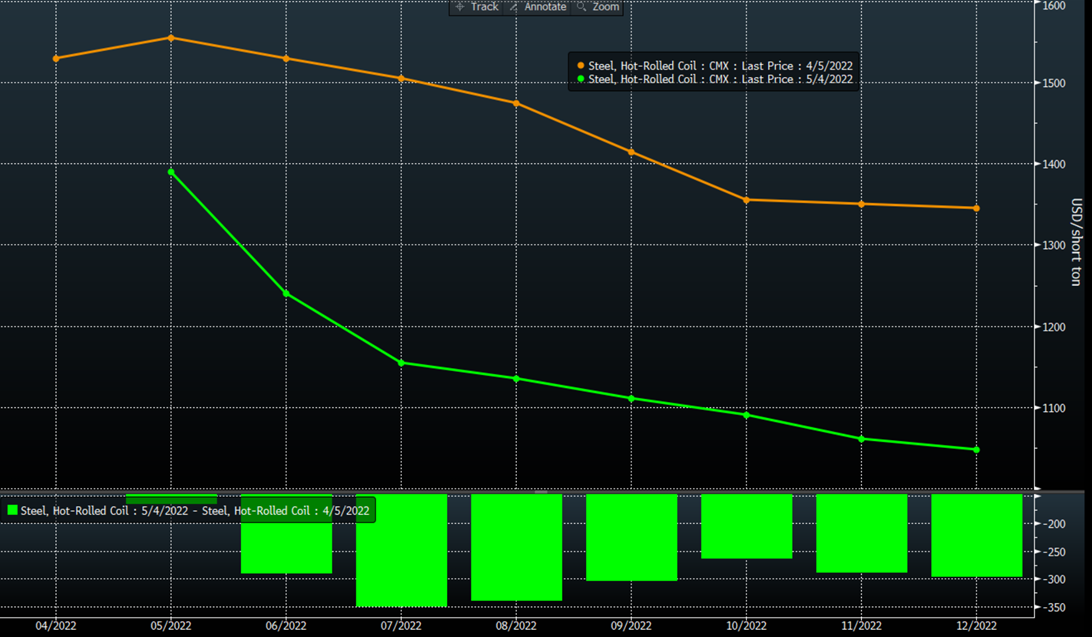

How about up slightly? This may be a bit surprising given what we read in the news, and there certainly has been a significant pullback in futures from the highs. Below is a chart showing the change in prices from one month ago. This might be more in line with what you would expect given recent events.

What might be causing the relative stability we have seen in HRC futures over the past week? Scrap may offer clues. You can see by the curve below that busheling futures have had a decent rise in the past few days, which may be part of the reason more buying pressure has been coming into the HRC market. It’s worth noting that we are now coming into the time period where new capacity will be ramping up, which should be supportive of scrap demand in the second half of the year.

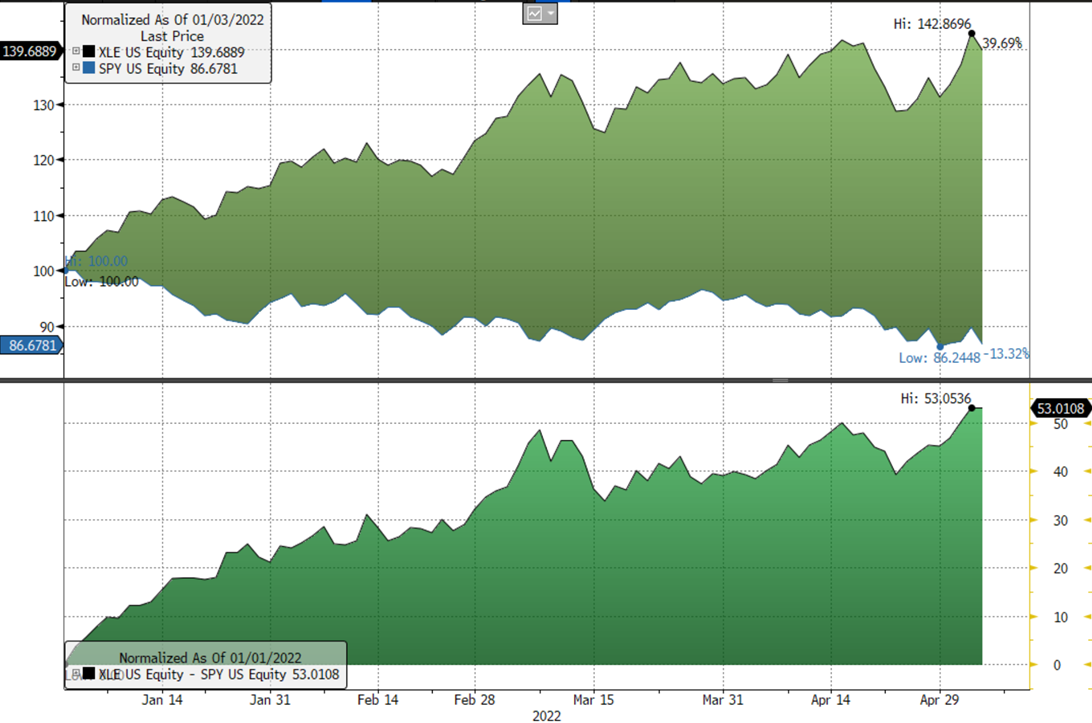

In addition, the energy sector has been seeing new life here in the US. The chart below shows the performance of the XLE vs the S&P 500 (SPY). The XLE is an exchange-traded fund that tracks the performance of the energy sector. The key part of the chart is the bottom panel, which shows that the energy sector has outperformed the S&P 500 by over 50% YTD. Certainly, the S&P has been under pressure, which makes it easier to outperform. But underlying energy sector fundamentals are improving with the elevated price of crude oil, and many energy companies gave bullish outlooks on their recent earnings calls. While the correlation of oil and steel prices has broken down over the past few years from what it used to be, high oil is generally a positive for steel prices.

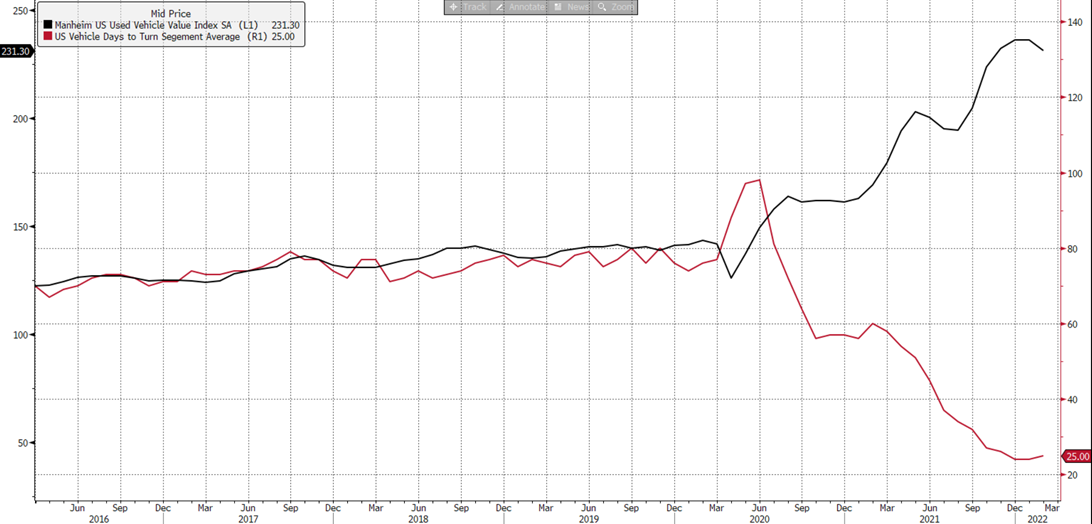

Auto-related steel demand has also gotten a lot of press. The chip shortage and other supply chain issues have wreaked havoc on production schedules and have resulted in less steel consumption. However, the lack of vehicles on dealer lots should, all else equal, means that there is pent up demand if/when some of the supply chain issues get worked out. We have no idea when this may occur. But the chart below has the Manheim used vehicle price index on it, as well as dealer inventories in terms of days on hand. At some point we will need to replenish these inventories, and car prices are at all-time highs, indicating that demand is still solid.

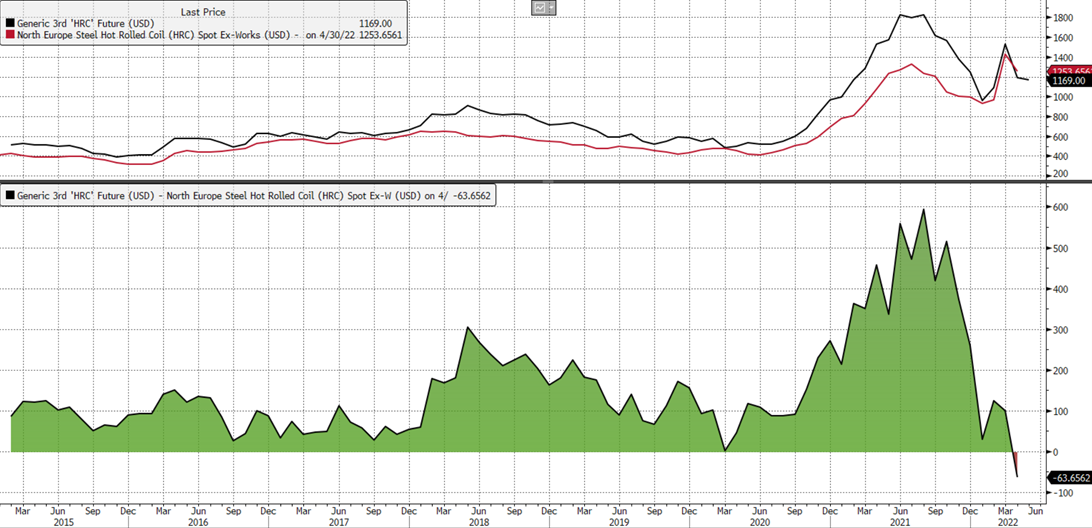

Also of note is the spread between European spot prices and the US 3 month future. It has now gone negative, which is not normal. In most markets, US prices trade at a premium to Europe, but that is no longer the case. Usually, US prices trade at a higher level since we need imports to balance our market. However, given the cost increases in Europe, and the new capacity additions here in the US – maybe this is the first sign that this premium may no longer be reasonable to expect?

So, maybe some better scrap pricing in the futures curve, very strong energy-related demand, and the possibility of better auto-related demand has traders thinking that the curve has dropped too far, too fast.

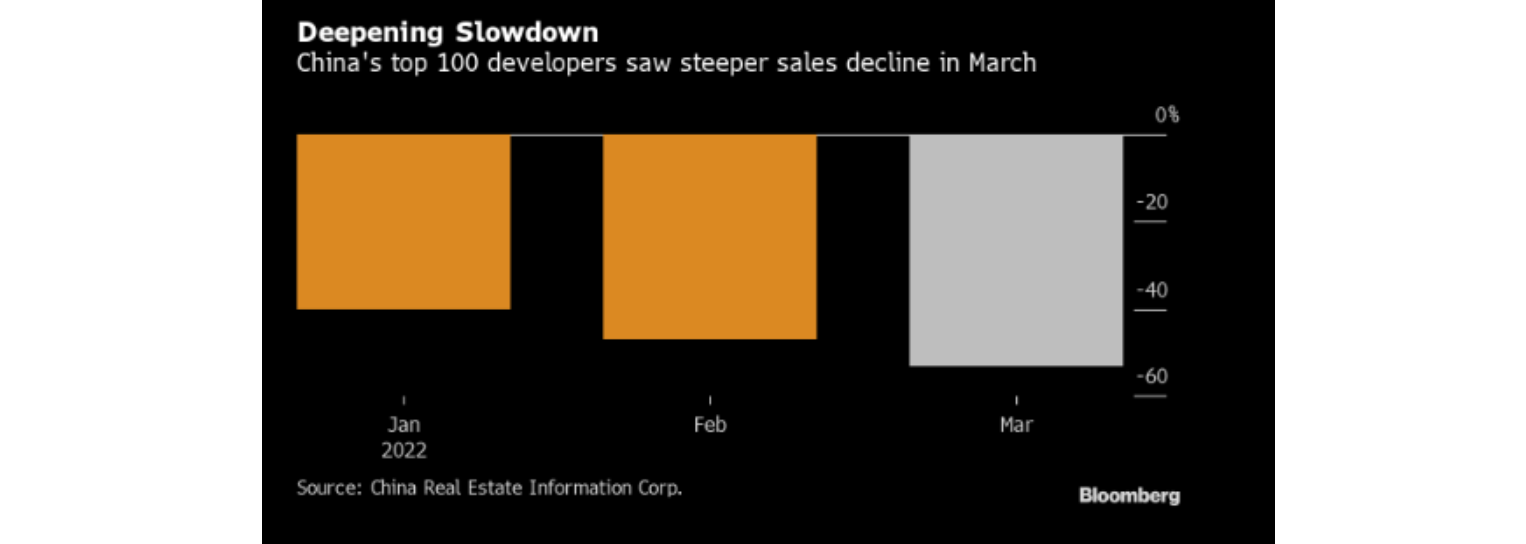

There remains plenty to worry about. Covid-related shutdowns in China will exacerbate supply chain problems. And while Beijing continues to talk about supporting the economy post shutdowns, there growing concerns about China’s property sector. See the chart below, which shows sales levels for the top 100 real estate developers in China. Sales declines are accelerating, and it remains to be seen whether stimulus and fiscal policy tools can right the ship.

With that, we will close for this week. Thanks for reading!

Disclaimer: The information in this write-up does not constitute “investment service”, “investment advice”, or “financial product advice” as defined by laws and/or regulations in any jurisdiction. Neither does it constitute nor should it be considered as any form of financial opinion or recommendation. The views expressed in the above article by Metal Edge Partners are subject to change based on market and other conditions. The information given above must be independently verified, and Metal Edge Partners does not assume responsibility for the accuracy of the information