Prices

August 18, 2022

Hot Rolled Futures: Peak Summer Pause?

Written by Jack Marshall

The following article on the hot-rolled coil (HRC), scrap and financial futures markets was written by Jack Marshall of Crunch Risk LLC. Here is how Jack saw trading over the past week:

Hot Rolled

Weekly changes in the value of spot HR have continued to drop an average of about $30/net ton but it should be noted that quite a few folks were surprised by the latest price drop. The latest spot index was $768/ton.

Recent announcements of HR price increases do not seem to have registered any bite which is likely due to the light volume of physical flat rolled that has been transacted. Many participants in the HR contract have described a very quiet physical market as the reason for reduced futures activity or it is just as likely a quiet summer period of plant furloughs.

Is this a typical quiet August market or has Fed watching kept many sidelined as inflationary and Covid headwinds continue to give mixed signals? Historically, HR prices are still above longer term averages, giving pause. Soft economic data out of China, potential Covid shutdowns, and recession worries are continuing to have a dampening effect. MSCI data points to healthy service center inventories and little-changed mill lead times do not signal any major supply concerns.

This month HR futures are trading at an average daily volume of just over 18,000 tons, of which over 83% has been in calendar 2022 months. Open interest in HR futures has barely moved this month, sitting at 23,619 contracts as of Aug. 17.

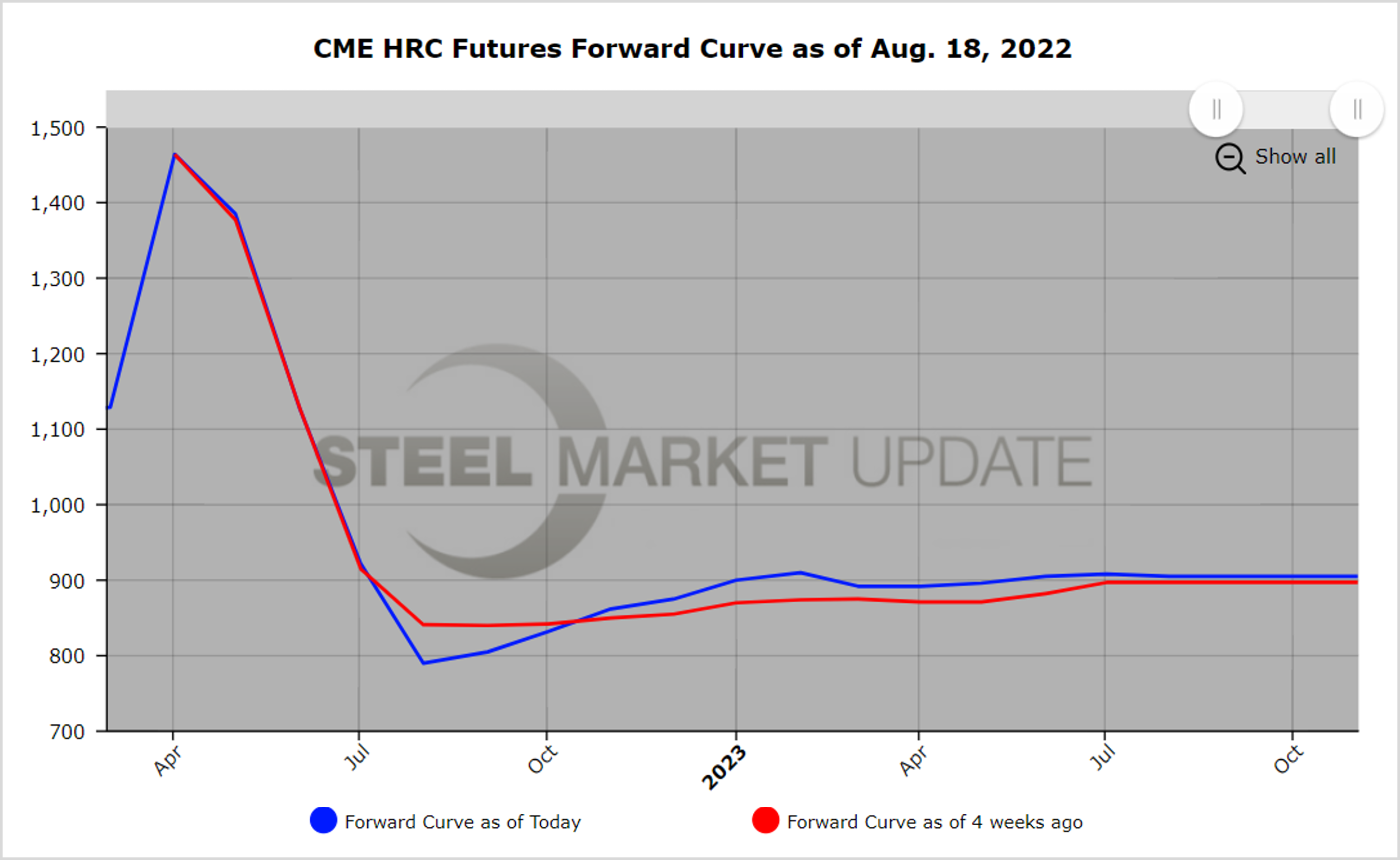

The shape of the futures curve reflects the spot drop in the near dates (-$60/ton) and the Q4’22 has declined roughly $25/ton, trading just above the mid $800/ton level. The curve continues to reflect the expectation that HR prices will push higher going into calendar 2023.

Below is a graph showing the history of the CME Group HR futures forward curve. You will need to view the graph on our website to use its interactive features. You can do so by clicking here. If you need assistance with either logging in or navigating the website, please contact us at info@SteelMarketUpdate.com.

Scrap

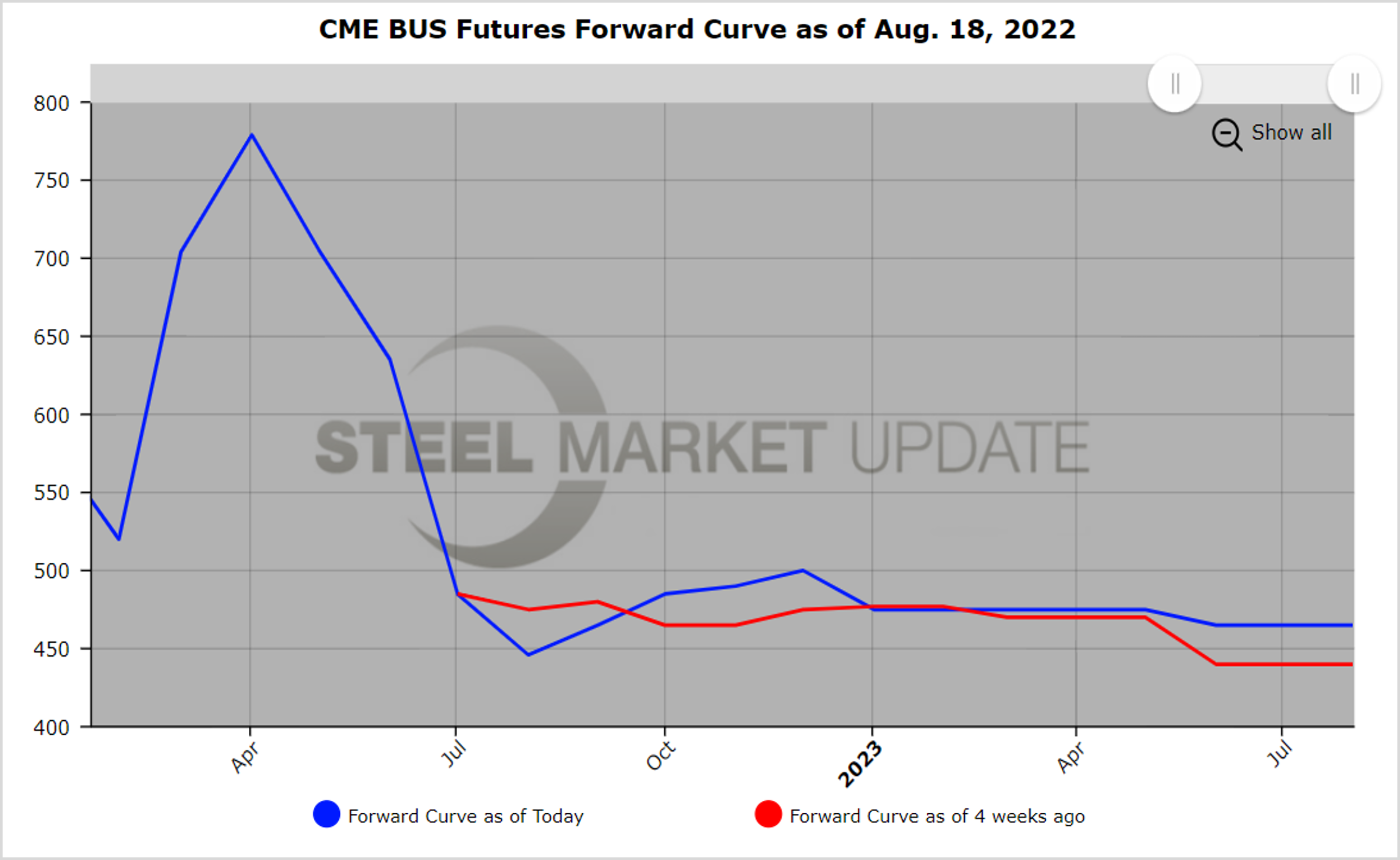

BUS declined $55/gross ton to $446/gross ton for August settlement. Month-to-date (Aug. 17) the settlement curve for BUS reflects about a $15/gross ton decline in value for calendar ’23 with values in the calendar ’22 months barely changed.

Latest Sep’22 BUS traded at $460/gross ton, which is only $5/gross ton below its value as of Aug 1.

Metal margin (HR-BUS) month-to-date Q4’22 has contracted just over $40/ton to $355/ton based on settlements Aug. 1 versus Aug. 17, while calendar ’23’s average metal margin has risen about $14/ton for the same period.

Below is another graph showing the history of the CME Group busheling scrap futures forward curve. You will need to view the graph on our website to use its interactive features. You can do so by clicking here.

By Jack Marshall of Crunch Risk LLC