Analysis

October 31, 2023

Final Thoughts

Written by Michael Cowden

Sheet prices are getting back into very lofty territory. That’s assuming you can find spot tons available for the balance of 2023 – and some of you say you can’t.

It shouldn’t come as a total surprise. We’ve seen lead times stretch out, mills enforcing sheet price increases – and that was before the United Auto Workers (UAW) strike ended (pending ratification votes).

Some of you tell me the prospect of increased consolidation in sheet, should U.S. Steel be sold, has also played a role.

If I had to place a bet, I’d put it on an announcement sometime between Nov. 1 and Dec. 1. That said, I don’t know anything beyond the same rumors you’ve probably heard. And the automotive sector is already opposing any Cliffs/U.S. Steel merger.

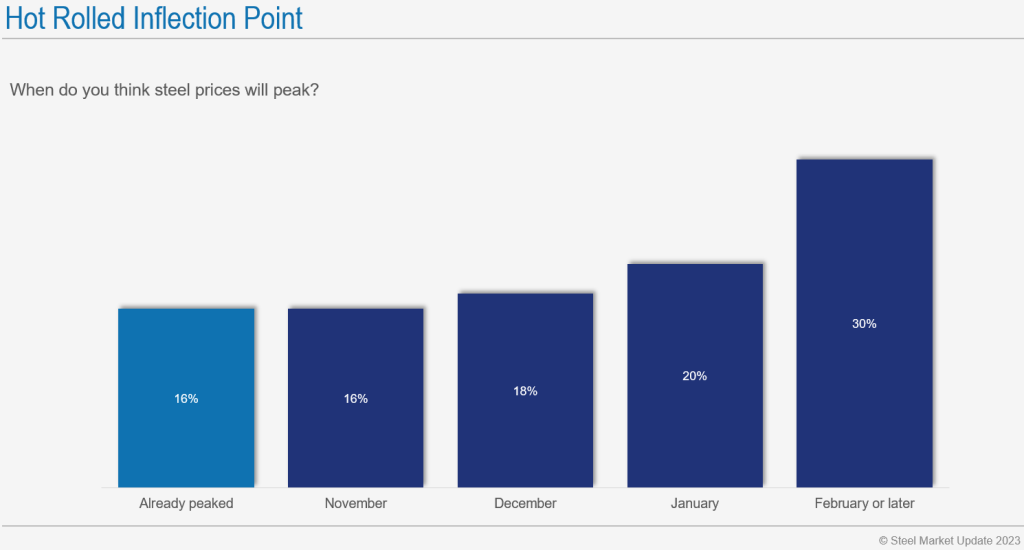

But I digress. Back to sheet prices. When will they peak?

Half of respondents to our last survey said not until January or February:

That squares with what I’ve heard talking to some of you in recent days. Almost all mills have closed December books for cold rolled and coated products – and increasingly for hot-rolled coil as well.

Mills might not be quoting January yet. I’m assuming they’re going to do that sometime in the next week – once they have a handle on what their contract tonnages are and how much spot they have available.

If the spot market is as strong as it seems to be at the moment, I wouldn’t be shocked if mills close out January within a week or so of opening books for the month.

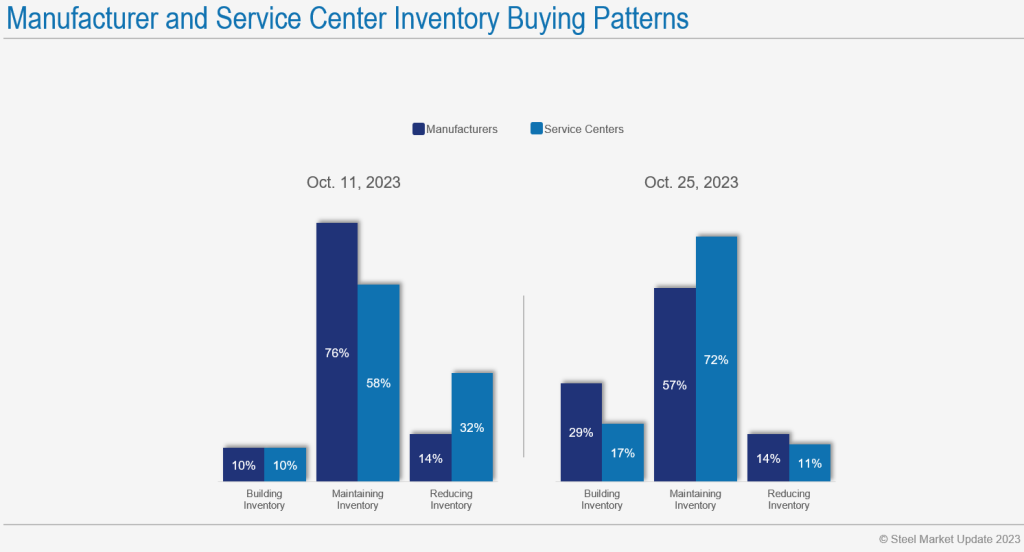

Why is that? Here is one reason. We saw a notable shift in our last survey – with more steel buyer respondents reporting building inventory than reducing it for the first time in months:

We know some big buyers loaded up on steel in September. Now it appears that others are as well.

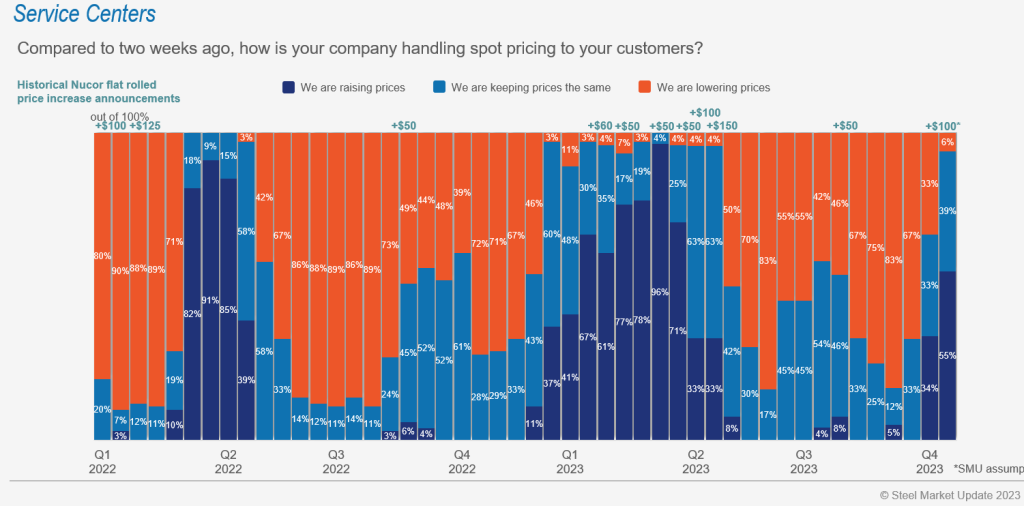

Also, service centers are no longer being shy about pushing higher prices along to their customers.

Approximately 94% are increasing prices or at least keeping them steady, up from just 17% in September:

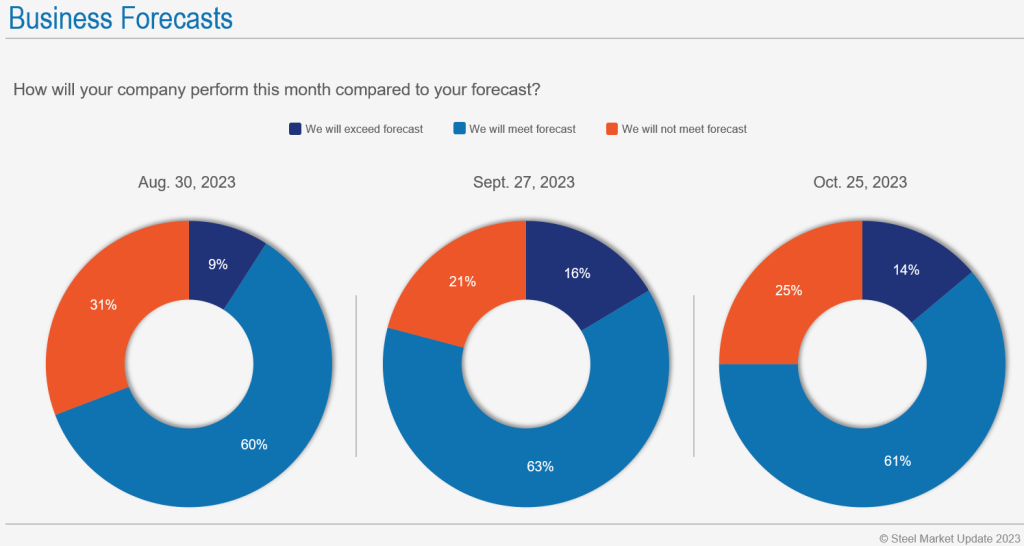

And, as we’ve noted for some time, approximately 70-75% percent of buyer respondents tell us they continue to meet or exceed forecast – a trend that was durable throughout the six-week UAW strike.

That said, some of you also think that an end to the current price upcycle is within sight.

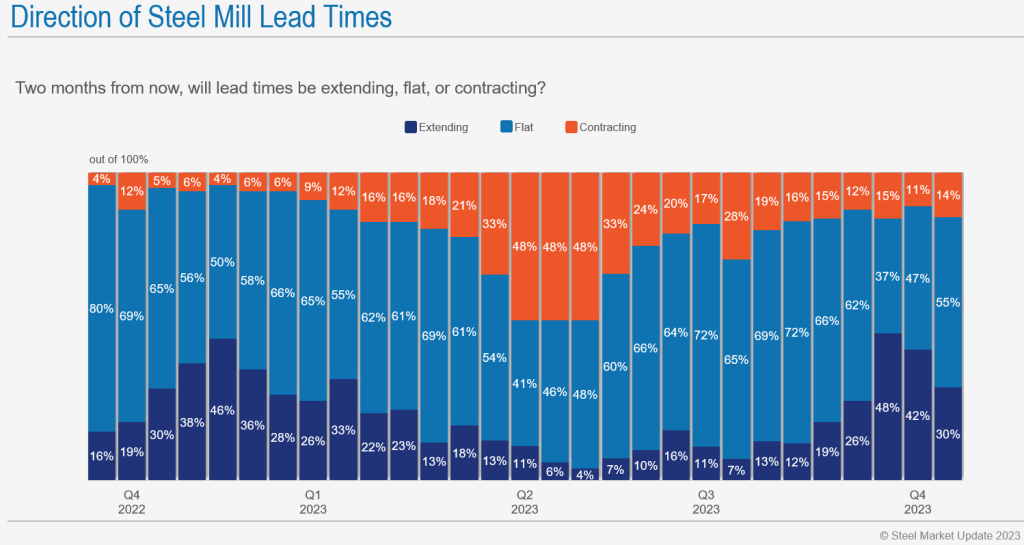

One example: where steel buyers think mill lead times will be in two months. That can be a leading indicator of lead times, which can themselves be leading indicator of prices:

Approximately 30% of people think lead times will still be extending in two months, down from 48% in late September. Note that the jump in people expecting lead times to rise coincided with sheet prices bottoming in late September.

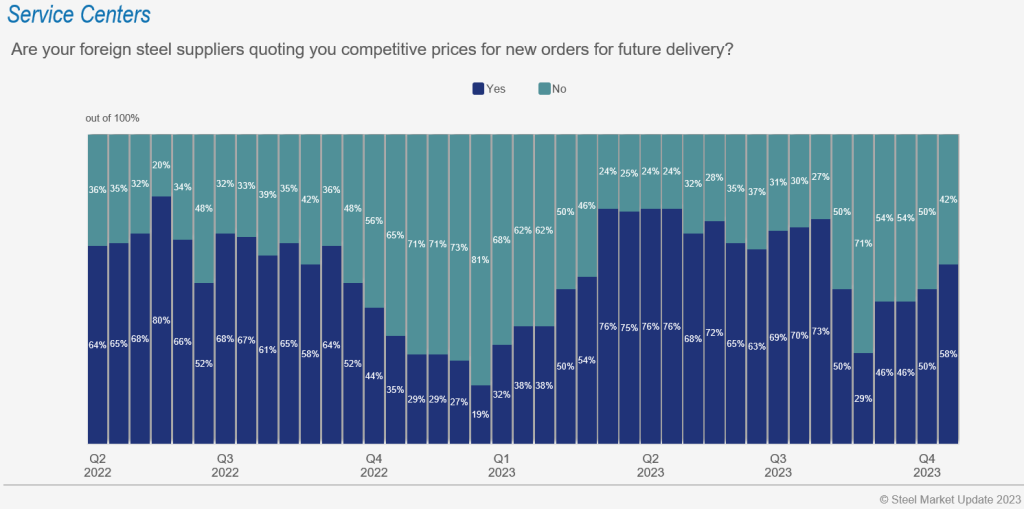

That roughly tracks with another trend that we’re seeing – more service centers expressing interest in imports.

Approximately 60% of service centers respondents to our latest survey reported that they found imports attractive – up from only ~30% in late August.

But, as I’ve noted before, imports ordered now might not arrive until late in Q1’24. So where do the increases stop: Is it the $900/ton announced over the last week by at least two domestic mills? Is it $1,000/ton? Because, in the meantime, what’s there to slow US prices from rising?

Let me know your thoughts.

SMU Community Chat

Don’t miss our next Community Chat webinar on Nov. 8 at 11 am ET with Wiley trade attorney Alan Price. You can register here.

We’ll talk about the US-EU trade deal that wasn’t, whether Section 232 (and retaliatory EU measures) might be re-imposed, as well as carbon and the future of US trade policy.

And we’ll take your questions too!

PS – Happy Halloween to all the parents, kids, and kids at heart from all of us at SMU!