Market Data

February 15, 2024

January service center shipments and inventories report

Written by Estelle Tran

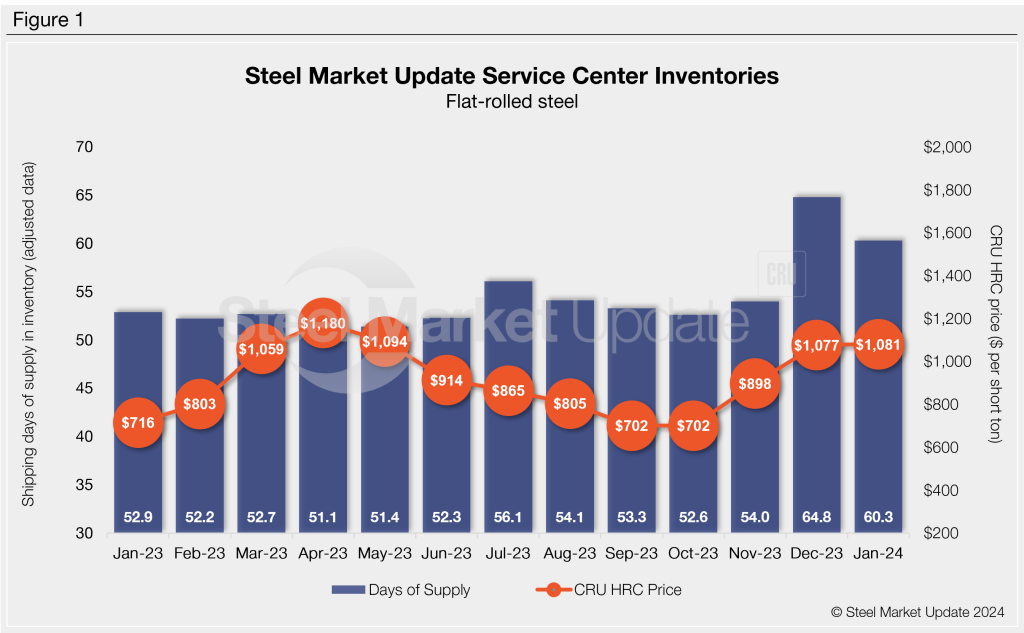

Flat Rolled = 60.3 Shipping Days of Supply

Plate = 63.4 Shipping Days of Supply

Flat Rolled

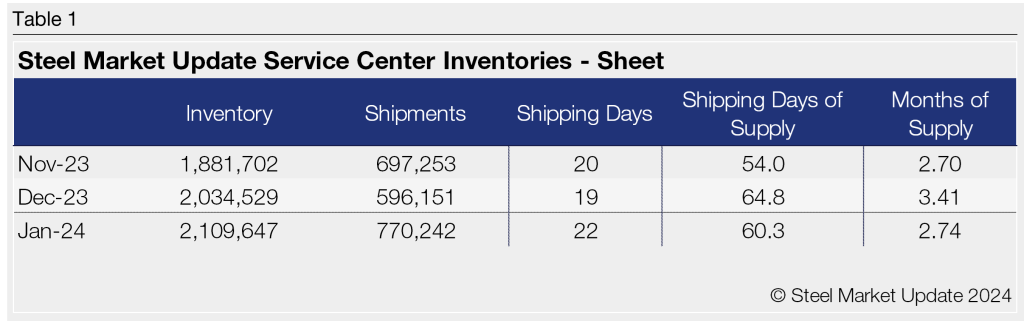

US service center flat-rolled steel supply declined in January, though less than expected because of a weaker-than-normal seasonal increase in shipments to start the year. At the end of January, service centers carried 60.3 shipping days of supply on hand, according to adjusted Steel Market Update data. This is down from 64.8 shipping days of supply in December.

In terms of months on hand, service centers carried 2.74 months of supply in January, down from 3.41 months of supply in December. By contrast, service centers carried 52.9 shipping days of supply or 2.52 months in January 2023.

The months-of-supply calculation can be skewed by the number of shipping days. January 2024 had 22 shipping days, while December had 19. January 2023 had 21 shipping days. We anticipated elevated inventory levels of flat rolled because of the high amount of material on order late last year, as service centers sought to place large-volume, opportunistic deals ahead of mill price increases. An 8.3% y/y drop off in the daily shipping rate in January kept inventories at high levels.

With ample supply at service centers, mill lead times have contracted. The SMU survey published Jan. 31 showed hot-rolled coil (HRC) lead times at 5.16 weeks, down from 6.26 weeks at the beginning of the month.

The amount of flat-rolled steel on order declined significantly in January. Despite the m/m decline of flat-rolled steel on order, it was still notably higher than January 2023. This suggests service centers will continue to minimize new orders, especially if seasonal demand remains weaker than normal.

Buyers remain hesitant to place orders with prices falling rapidly. We expect the material on order figure, which is bolstered partially by imports and delays from certain mills, to continue to fall in February.

Plate

US service center plate supply fell in January, though like sheet, shipments for plate also had a historically weaker start to the year. At the end of January, service centers carried 63.4 shipping days of plate supply, down from 66.4 on an adjusted basis in December. Plate supply on hand represented 2.88 months of supply in January, down from 3.49 months in December.

The daily shipping rate for plate was down 9% y/y in January. Plate demand has been subdued to start the year, and market contacts have said that despite an increase in quoting activity, they are unsure if or when demand will pick up. The lower shipping rate also caused a spike in intake, which reached its highest level since June 2023.

The amount of plate on order was fairly steady m/m in terms of supply. With the higher daily shipping rate in January, the number of shipping days of plate supply on order fell back slightly. At the end of January, material on order represented as percentage of plate inventories declined vs. December. Compared with total material on order in January 2023 though, the material on order in January 2024 was down 2.7%.

Meanwhile, mill lead times have also been flat at 5.8 weeks recorded for plate at the beginning and end of January. With short lead times and uncertain demand outlooks, buyers have been content to limit new orders, especially as Nucor brings its new Brandenburg plate mill up to consistent production levels. Service center plate inventories run the risk of becoming bloated if demand does not increase.