Analysis

April 30, 2024

Final thoughts

Written by Michael Cowden

Hot rolled prices held roughly steady this week after slipping for much of April. I don’t have any spicy quotes to offer about mostly flat prices.

Besides, a lot of the questions I’ve gotten recently have been about demand. Some of you tell me that it’s still stable or improving. Others tell me that it’s suddenly dried up.

It’s hard to quantify anecdotal comments. So I went back through our steel market surveys to see if there was any evidence to support the notion that demand might be slowing down – or at least not overheating.

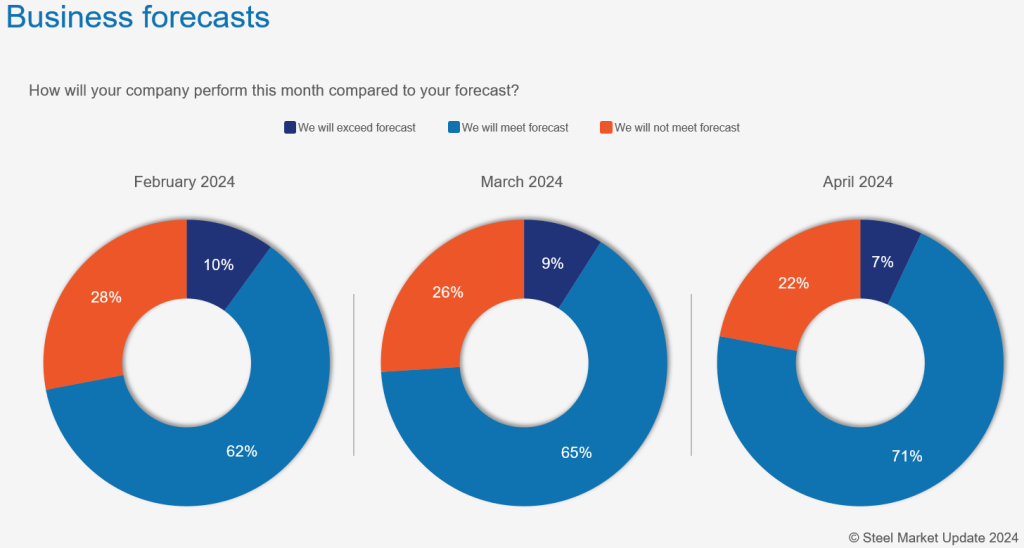

Demand is not bad (but not great either)

Here is where things stood over the last three months:

No big changes. Most people (60-70%) said they were meeting forecast. Around 7-10% said they were exceeding forecast. And about 20-30% said they were missing forecast.

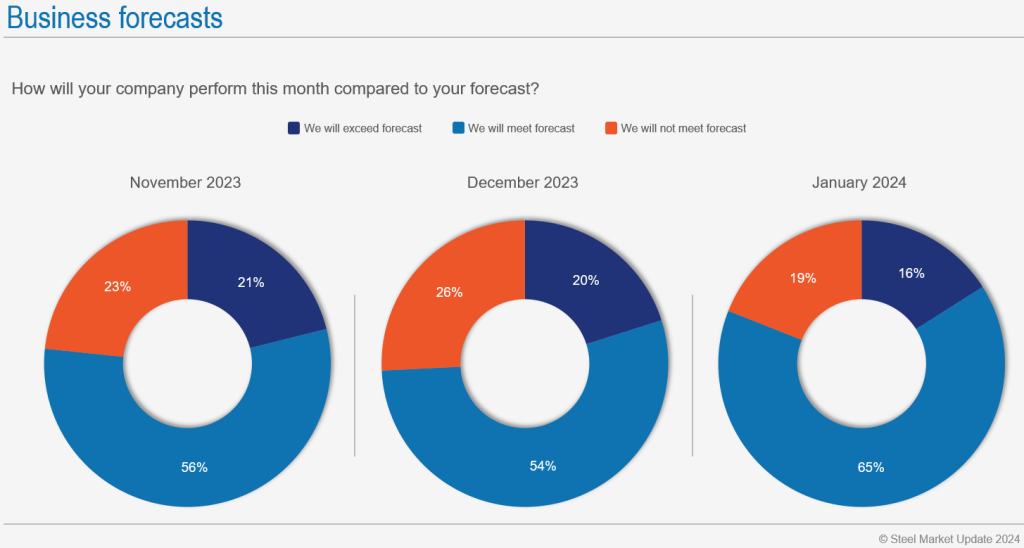

Compare that to the late 2023 and early 2024:

That’s where we see some change. The number of folks missing forecast (~20-30%) hasn’t budged. But the number of people exceeding forecast was higher last year and through the start of this year (~15-20%).

Also, some of you who are meeting forecast tell me that you’ve adjusted forecasts a little lower. So, based on our survey data and comments like that, I think there might be something to the idea that demand has moderated.

There is also a range of outside data to support that notion. The Architectural Billings Index (ABI) fell to its lowest point since December 2020. The Chicago business barometer fell to its lowest point since November 2022. And service center’s sheet inventories are running a little high, especially with lead times stagnant.

Imports could remain high in April

Also, flat-rolled steel imports could remain elevated this month. The US was licensed to import 796,526 metric tons (mt) through April 23. That was the most recent data available when I filed this article on Tuesday evening.

That amounts to 34,632 mt per day. Or, theoretically, another 242,420 mt for the last week of the month. That gets us, in theory, to an April total of approximately 1.04 million mt.

That would be higher than the 950,426 mt of flat-rolled steel that arrived in March, according to preliminary government figures. And recall that the March figure was the highest since nearly 975,000 mt in August 2022.

I’m not saying it’s a slam dunk that April flat rolled will exceed 1 million mt. Import data can be lumpy. And there can be big gaps between license data and preliminary figures. Still, I’d also be surprised if April flat rolled imports turned out to be significantly lower than March.

And all else being equal, more supply and steady demand typically equates to lower prices. Or at least not sharply higher ones.

Normal is OK

That said, I’m not in the camp that’s singing the economic blues. Wages are rising. That might make life tricky for the Fed as it tries to tame inflation. Or for a stock market hoping for rate cuts.

But it’s not bad for consumers. One fun anecdote: When I was at the ISRI (ahem, ReMA) conference in Vegas earlier this month, the Strip was packed during the middle of the week. Not exactly a sign of an impending recession, that.

Here’s my best shot at squaring what I’ll call the doom-and-gloom camp and the steady-Eddie camp. Demand is stable. Maybe down a tick. And after several years of record prices and profits, normal might not feel so great. But that doesn’t mean there’s anything wrong with it.

What do you think? Let us know at info@steelmarketupdate.com.

SMU Steel Summit

Our hotel blocks for this year’s Steel Summit – Aug. 26-28 at the Georgia International Convention Center (GICC) in Atlanta – are going fast. Don’t miss your chance to get discounted hotel rates on the GICC campus, register now!