Steel imports strengthen through April licenses

March 2024 represents the third highest monthly steel import rate seen over the prior year.

March 2024 represents the third highest monthly steel import rate seen over the prior year.

US announces new import duties on aluminum extrusions The US Department of Commerce has placed preliminary antidumping (AD) duties of 2-600% on imports of aluminum extrusions from 14 countries. The rates are: “[The findings] show just how widespread dumping practices are globally and highlight the importance of strongly enforcing the antidumping laws to shield US […]

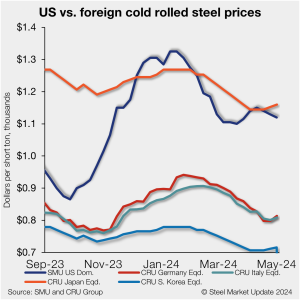

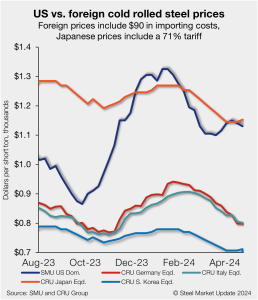

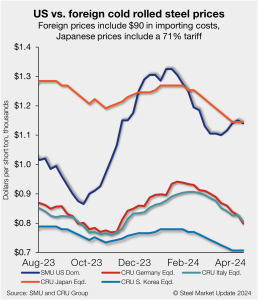

Foreign cold-rolled (CR) coil remains much less expensive than domestic product even as domestic prices continue to decline, according to SMU’s latest check of the market.

Brazil’s chamber of foreign trade, Camex, has approved quotas on imports of 11 steel products and a 25% levy on shipments 30% above a product’s average import volume between 2020 and 2022.

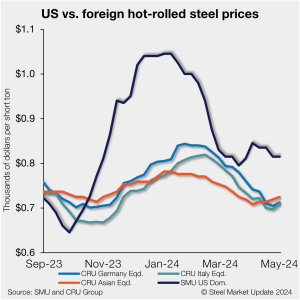

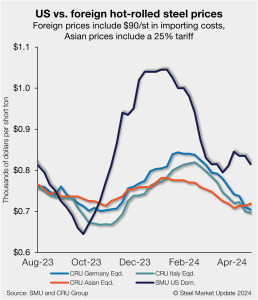

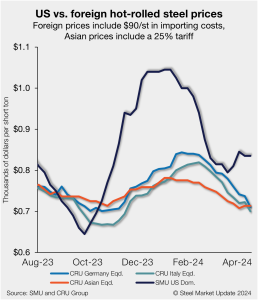

US hot-rolled (HR) coil price premium over offshore hot band has tightened on the back of lower domestic tags, though stateside HR coil remains markedly more expensive than imports.

On Monday and Tuesday of this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to imports and evolving market chatter.

Hold-rolled (HR) prices held roughly steady this week after slipping for much of April. I don’t have any spicy quotes to offer about mostly flat prices. Besides, a lot of the questions I’ve gotten recently have been about demand. Some of you tell me that it’s still stable or improving. Others tell me that it’s suddenly dried up.

What a difference a month makes. In late March, it seemed like the US hot-rolled (HR) coil market was poised to cycle upward. Large buyers had re-entered the market and placed big orders earlier in the month. Several outages were underway or upcoming. And expectations were that lead times would continue to extend. Cliffs said […]

Constellium reported its latest quarterly results for Q1'24. Adjusted Ebitda came in at €137 million (USD$147 million), down 8.6% year over year (y/y) amid revenue of €1.7 billion (USD$1.8 billion), down 12% y/y. Shipments totalled 380,000 metric tons (mt) in Q1, representing a drop of 2% y/y.

Foreign cold-rolled (CR) coil remains much less expensive than domestic product, according to SMU’s latest check of the market.

Hot-rolled coil and plate lead times contracted this week, with most other products remaining flat, according to SMU's most recent survey data. Cold-rolled products, however, saw lead times extend 0.1 weeks to an average of 7.5 weeks vs. two weeks earlier. Hot rolled and plate lead times both contracted 0.3 weeks from our last market check.

I’ve gotten some questions lately about whether the huge gap between domestic hot-rolled coil (HR) prices and those for cold-rolled (CR) and coated is sustainable. I remember being asked similar questions about the wide spread between HR and plate that developed in early 2022. I thought at the time that there was no way that spread could hold. Turned out, I was wrong. That was humbling. And so I’m not going to make any bold predictions this time.

Destocking at service centers and a downturn in steel pricing impacted Ternium’s shipments in Mexico in the first quarter of the year.

Steel imports held steady in March, up just 1% from February according to preliminary Census data released earlier this week.

US hot-rolled (HR) coil remains more expensive than offshore hot band, though with a tighter premium as prices stateside and abroad have ticked lower in recent weeks.

We've used the word "unprecedented" a lot over the last four years to describe steel price volatility. Over the last two months – despite earlier predictions of a price surge - we've seen unprecedented stability.

Steel Dynamics Inc.'s (SDI's) earnings fell in the first quarter of 2024 as the company cited steel order volatility early in the quarter and lower scrap prices.

Nucor executives explained their recently introduced hot-rolled (HR) coil consumer spot price (CSP) is a way to serve their customers and deal with market volatility.

ArcelorMittal plans to build a new electrical steel manufacturing facility near its AM/NS Calvert joint-venture mill in Alabama.

Last week gave us a glimpse into the effect of the 2024 election campaign on trade policy. In a major announcement, the Biden administration pressed the US Trade Representative (USTR) to triple certain Section 301 tariffs on steel and aluminum. It’s a lot to unpack. You can find the full text of the announcement here. […]

Steel sheet prices in many regions of the world were steady week over week in the week ended April 17.

Foreign cold-rolled (CR) coil remains less expensive than domestic product, according to SMU’s latest check of the market.

Here’s a roundup of the latest news in the global aluminum market from our colleagues at CRU. Biden calls for tripling of Chinese steel and aluminum tariffs President Joe Biden is calling on the US Trade Representative (USTR) to consider increasing the existing section 301 import duty on Chinese steel and aluminum three-fold. The current […]

US hot-rolled (HR) coil has become gradually more expensive than offshore hot band in recent weeks, as stateside prices have stabilized while imports moved lower.

The Biden administration on Wednesday announced measures to support the domestic steel industry.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to imports and evolving market chatter.

The steel market appears to be finding a new, higher normal with the shocks of the pandemic and the Ukraine in the rearview mirror. The good news: a more profitable and consolidated post-Covid US steel industry has been able to invest in operations. That includes efforts to decarbonize. The bad news: That “new normal” could be tested. Because it’s not just domestic sheet prices that have been volatile. Geopolitics are too.

Last week was a newsy one for the US sheet market. Nucor’s announcement that it would publish a weekly HR spot price was the talk of the town – whether that was in chatter among colleagues, at the Boy Scouts of America Metals Industry dinner, or in SMU’s latest market survey. Some think that it could Nucor's spot HR price could bring stability to notoriously volatile US sheet prices, according to SMU's latest steel market survey. Others think it’s too early to gauge its impact. And still others said they were leery of any attempt by producers to control prices.

Total domestic aluminum mill products orders in March were up 0.2% compared to March 2023, according to the latest “Index of Net New Orders of Aluminum Mill Products” released by the US Aluminum Association (AA). This is much lower than the growth of 9.3% year over year (y/y) reported in February.

The Department of Commerce (DOC) has issued new rules to combat evolving "unfair" trade practice — including the unfair trade of steel products. They go into effect on Wednesday, April 24.