Big River Steel updates galvanized coating extras

Big River Steel (BRS) made upward revisions to most of its galvanized coating extras this week, with new extras going into effect July 6.

Big River Steel (BRS) made upward revisions to most of its galvanized coating extras this week, with new extras going into effect July 6.

The CRU US Midwest hot-rolled (HR) coil index is a dominant and established price benchmark in the US. Many steel-buying contracts are linked to ‘the CRU,’ as it’s commonly called. But how does it work?

Nucor upped its published consumer spot price (CSP) this week.

The free market operates best when it is freest. But all governments intervene in markets in response to conditions that threaten peaceful progress. President Biden decided last week that market intervention was justified. He approved a report from the US Trade Representative (USTR) that recommended continuing the “Section 301” tariffs on Chinese imports into the United States.

President Biden announced an increase in tariffs this week on Chinese EVs, semiconductors, batteries, solar cells, steel, and aluminum.

The spread between hot-rolled coil (HRC) and prime scrap prices narrowed this month, according to SMU’s most recent pricing data.

Roughly halfway through Q2, flatbed rates are holding firm, currently showing no change from April to May and a slight increase quarter-over-quarter (q/q).

The recent decline in US hot-rolled (HR) coil and longs prices has further restricted demand for imported material. Despite the decline in US sheet prices, CR coil and HDG imports remain attractive. While demand for imports of longs products has been limited, buyers have increased imports of wire products to avoid wire rods’ higher tariffs. […]

Earlier this month, steelmakers entered the scrap market at mixed pricing. The prevailing price for obsolescent grades fell $20 per gross ton (gt). However, some notable districts decided to only drop $10/gt.

The last time we were together on April 18, the June hot-rolled coil (HRC) future was sitting around the $800 support level where the May future found a bottom in mid-February.

US hot-rolled (HR) coil prices saw further declines this week, while foreign prices were steady to slightly higher in the three regions we monitor

Veteran StoneX futures broker Spencer Johnson will be the featured speaker on the next SMU Community Chat on Wednesday, May 29, at 11 am ET. You can register here. Note that the live webinar is free for all to attend. A recording will be available only to SMU members.

Domestic scrap prices this month are flat for prime material, but down for HMS and shredded, scrap sources told SMU.

SMU surveyed our market contacts this week about steel prices, demand, and the overall marketplace. Below are some of the buyers' responses in their own words to help you get a feel for current and future market conditions. Demand is a big topic of discussion currently. Is it steady, falling, or on the upswing with summer construction heating up? As you can see from the answers below, it depends on who you ask. One buyer’s response sums it up pretty well: “I still see the marketplace as soft/stable with some segments busy, while others tread water.”

Cleveland-Cliffs’ Lourenco Goncalves thinks trade measures announced by the US government on Tuesday against China were just the opening salvo in a series of trade actions. Case in point: The Biden administration targeted China’s “unfair” trade policies with additional tariffs on an array of Chinese-made goods - including steel, aluminum, and EVs.

Steel Market Update is pleased to share this Premium content with Executive members. For information on how to upgrade to a Premium-level subscription, contact info@steelmarketupdate.com. Flat Rolled = 57.8 shipping days of supply Plate = 58.3 shipping days of supply Flat Rolled US service center flat-rolled steel supply edged lower in April, though shipments continue to […]

Our spot price is little changed this week after moving sharply lower last week on the heels of Nucor’s unexpected price cut. Here’s one thought on that trend: Nucor's weekly HR price (aka, its “Consumer Spot Price” or CSP) has to date functioned almost more like a monthly price.

Steel prices were overall mixed this week, according to our latest check on the market. Sheet prices were flat to down, while plate prices inched up. SMU indices on hot rolled, cold rolled, and galvanized are now down to the lowest levels seen since November.

Prices for hot-rolled (HR) coil in recent weeks have been declining faster than those for galvanized sheet, resulting in a growing price spread between the two steel products.

Wolfe Research Managing Director Timna Tanners cautioned clients about the darkening clouds of a brewing steel sheet storm in the company's Basic Materials Weekly Webcast on Monday. “This one we’ve been talking about for a while, and we feel like the theme is coalescing here,” she said.

What's the tea in the steel industry this week? Here's the latest SMU gossip column! Just kidding... kind of. Yes, some of the comments we receive in our weekly flat-rolled market steel buyers' survey are honestly too much to put into print. Some make us laugh. Some make us cringe. Some are cryptic. Most are serious. We appreciate them all. Below are some highlights from our survey results this week. Some of the comments that we can share with you are also included, in italics, in the buyers' own words, with minimal editing on our part.

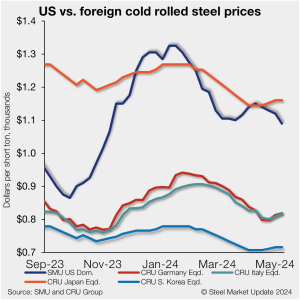

Offshore cold-rolled (CR) coil prices remain much less expensive than domestic product, even as domestic prices have slipped to a six-month low, according to SMU’s latest check of the market.

The Mexican federal government backed down on the application of tariffs on raw non-alloyed and alloyed aluminum decreed on April 22.

In this Premium analysis we cover North American oil and natural gas prices, drilling rig activity, and crude oil stock levels.

Steel Market Update’s Steel Demand Index fell eight points, and back into contraction territory, an indication demand might be slipping as prices have trended lower, according to our latest survey data.

The latest SMU market survey results are now available on our website to all premium members. After logging in at steelmarketupdate.com, visit the pricing and analysis tab and look under the “survey results” section for “latest survey results.” Historical survey results are also available under that selection. If you need help accessing the survey results, or if […]

Japanese steelmaker JFE Holdings will invest abroad as part of a drive to lift income, says group president Yoshihisa Kitano.

Last week we wrote about a brief lull in price movement, labeling it a period of wait and see. It did, in fact, turn out to be pretty brief. This week... things are little bit different. Perhaps right now we are more in a period of "hope and pray" or "Here we go, hold on to your hats."

Steel prices trickled lower across the month of April for both sheet and plate products.

Stelco reported a positive start to 2024 in its first-quarter earnings report on Thursday. And with steady demand and a stable market, the Canadian flat-rolled steelmaker is optimistic for the remainder of the year.