Market Segment

November 16, 2023

Plate Report: Quiet Turning to Sluggish?

Written by David Schollaert

The US plate market has been relatively quiet over the past few weeks since Nucor Corp. caught many off guard with a $140-per-ton price cut late in October.

Many sources have categorized demand as stable at best, with even prompts from mill representatives going quiet. Not surprisingly, mills’ willingness to negotiate lower spot plate pricing shot up, according to SMU’s most recent survey data.

But that hasn’t led to much buying, sources told SMU, even as the price gap between hot-rolled coil (HRC) and plate reached a seven-month low. While HRC prices increased by another $75 per ton this past week, spurred on by repeated mill hikes, US plate prices have been relatively flat for much of this year, eroding only more recently over the past three weeks.

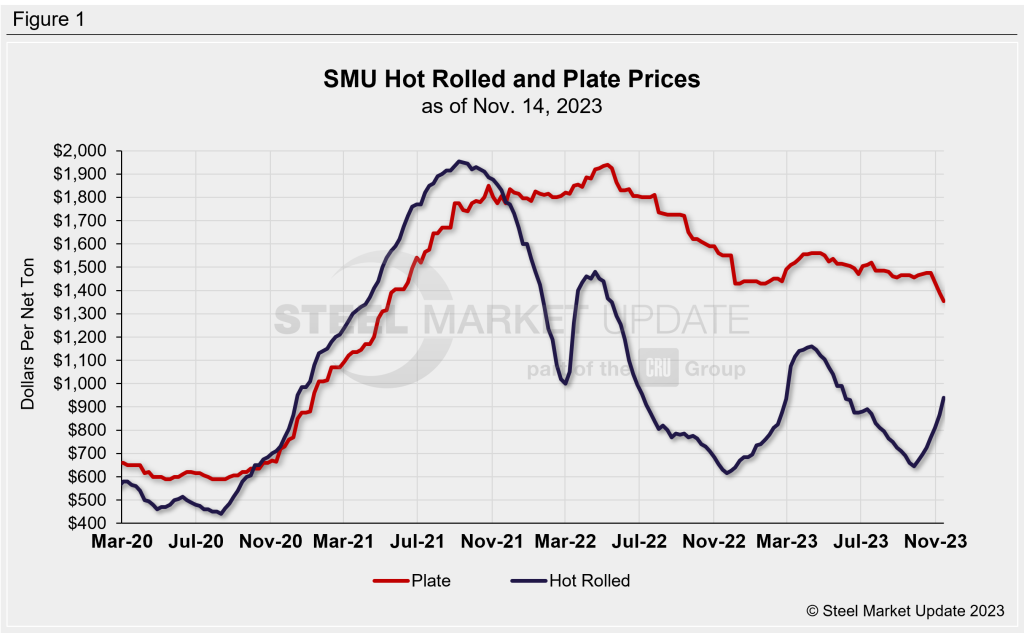

Case in point: SMU’s plate price stands at $1,355 per ton ($67.75 per cwt) on average, down $35 per ton from last week and down $165 per ton from a recent high of $1,520 per ton in mid-July (Figure 1). Our HRC price is $940 per ton, up $75 per ton from last week and up $295 per ton since reaching a recent bottom of $645 per ton at the end of September.

Market Reaction

While there is apparent price stability now, many speculate that plate tags could move lower before the end of the year. Thus, sentiment is still mixed on where demand is at present and in the short term.

And with little in the way of spot demand, some expect the next pricing announcement could be down again. But with scrap moving higher, some suspect tags could hold for now.

SMU spoke with several plate market participants about the current state of the market.

“Plate is not the most exciting product market right now; that title goes to HRC,” said one source.

“Not much has happened since Nucor’s announced decrease to get them more in line with where the market was already at,” said another source. “We have seen SSAB and Cliffs get in line with the Nucor number but haven’t seen the other regional players move much at all.”

“Nucor’s pricing is still the benchmark, but distributors are still probably discounting as much or more than other mills in plate,” said a third source.

“Mills know this time of year dropping their prices isn’t going to get them any more business,” commented another source.

What’s Ahead?

The trend we’ve seen for much of the year is expected to continue: Limited spot activity and mills leaning heavily on contract business.

But as some had suggested when Nucor first cut prices back in late October, the burden would be placed most significantly on competitors and service centers alike.

“Resale prices are below Nucor’s new FOB mill price,” said a source. “Service centers are in a rush to get rid of anything currently on the floor.”

“Mills waited way too long and now their order books are suffering,” added another source. “There should be some year-end deals to try and fill the mill’s order book and then possible attempts for an increase circa recent HRC activity.”

Despite the added pressure and potentially even lower plate prices in Q4, most agree that the new year will bring about renewed price hikes.

“I fully expect an increase in early Q1. Let’s see what support follows from all directions,” said a source. His sentiment was echoed by others.

“In December they will increase the prices back up for Q1 2024 delivery orders, saying demand has been improved or something like that,” another source commented.

“Not a fun plate time for sure, maybe things will turn Q1…” noted a third source.

“Things are pretty much what they are going to be for the next 45 days,” another source said. “Things are fine all things considered. Don’t panic anyone.”

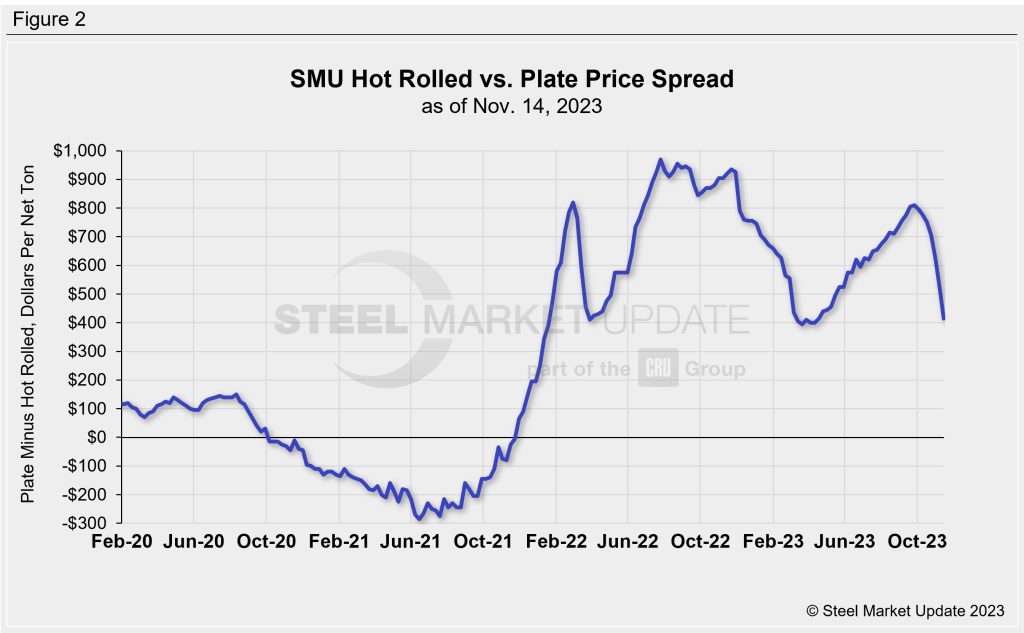

HRC-Plate Spread

It’s been nearly two years now since plate prices decoupled from HRC (Figure 2). We saw the spread between plate and HRC reach as high as $970 per ton in the summer of 2022. It currently sits at $415 per ton, a seven-month low.

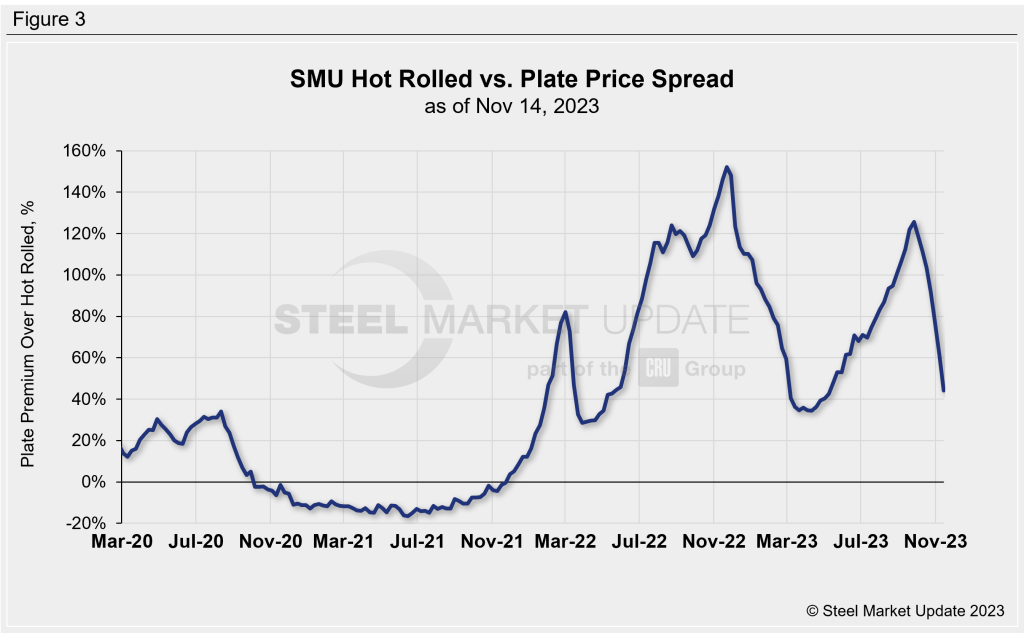

As a percentage basis, plate’s premium over HRC had ballooned to 126% in late September (Figure 3), reaching a 10-month high, not far from the all-time high of 152% in November 2022. But with HRC prices surging and plate tags declining, the premium is down to just 44%.

The Takeaway

With plate demand spotty, sellers have been discounting and undercutting published mill prices. That trend is still expected. And with increased imports arriving in Q1, there is some speculation that further plate price erosion is likely even with higher scrap costs.

Most are still focused on controlling order books; another price cut could highlight that trend. But if lower tags don’t attract some buying, others expect little change between now and the New Year.

Imports are still attractive. Offshore product is running well below $1,300 per ton at depots. Plate for early Q1 delivery from South Korea and Thailand is sub-$1,200 per ton, according to several sources.

It’s important to keep an eye on discrete plate lead times. While they had inched a bit in late October, the latest data suggest they are below six weeks on average and trending lower – nearing five weeks or less.