Prices

January 28, 2024

HRC futures: Changing futures dynamics

Written by Bradley Clark & Gaby Ain

What a difference a few weeks make…. As this is our first column after the new year, it is quite interesting to observe how different the steel world looks at the end of January vs. the end of December.

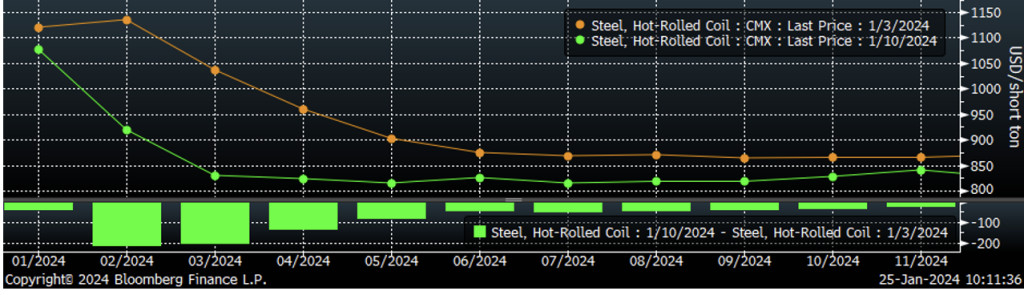

The first few days of 2024 on the futures market provided bulls with the much expected “new year exuberance” bounce, with prices along the curve pushing up substantially. Well, that optimism was dashed as the first week of the year wore on, with sellers entering the market throwing cold water on sentiment, plunging prices by over $200 per short ton (st) over the next week. Subsequently, we have seen the worst of that subside, with February and March both rallying since then.

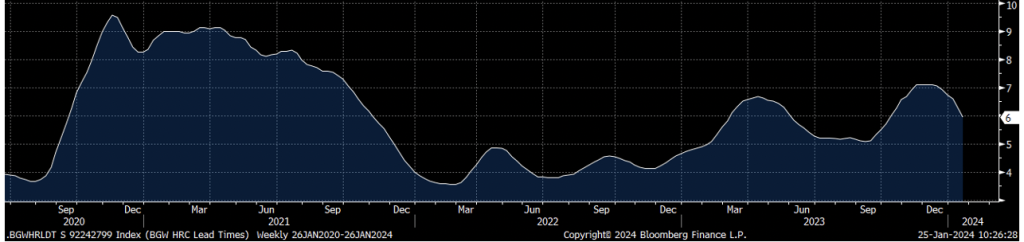

While the physical market looked to shore up pricing levels in these first few weeks of the year, apparent demand failed to materialize as inventories began to be reported as higher than expected. In addition, lead times appeared not to be as solidly far out as it seemed before the holidays. It was a case of the tail wagging the dog with futures prices plummeting driving negative sentiment in the cash market.

Chatter in the paper market during this time indicated a split market with many in the industry not seeing physical as bad as futures prices started to suggest, while some financial players seemed to be more skeptical. As the curve moved into a strong backwardation from spot into the next few trading months, a familiar refrain of “while prices may be softening, the curve is undervalued” could be heard mumbled throughout the market. This sets up a classic trap in trading.

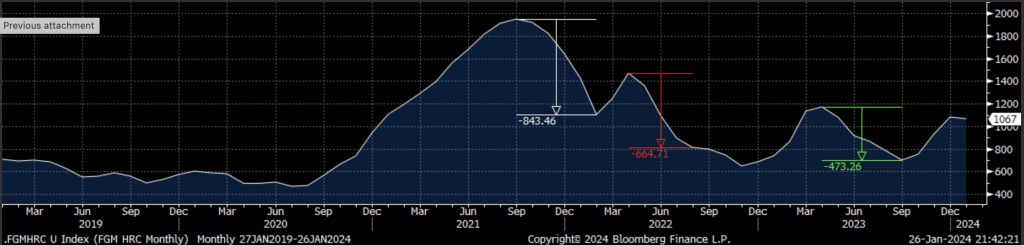

It seems now that physical and futures sentiment are converging as the price action in futures over the past week has stabilized. It feels like we are back to the physical market dictating where paper goes from here, the dog wagging the tail, for the time being. Interesting to note, if we look over the past five years, the peak-to-trough price movements throughout the cycles has fallen a minimum of a $450/st move.

If the spot peaked around $1,100 a few weeks ago, and history repeats itself, the curve might not be as undervalued as some believe.

About Flack Global Metals

In 2010, Flack Global Metals (FGM) was founded with the mission to reinvent how metal is bought and sold. Over 13 years later, the company has evolved into a hybrid organization combining an innovative domestic flat-rolled metals distributor and supply chain manager, a hedging and risk management group supported by the most sophisticated ferrous trading desk in the industry known as Flack Metal Bank (FMB), and an investment platform focused on steel-consuming OEMs called Flack Manufacturing Investments (FMI). Together, these entities deliver certainty and provide optionality to control commodity price risk in the volatile steel industry.

Disclaimer: The content of this article is for informational purposes only. The views in this article do not represent financial services or advice. Any opinion expressed by Flack Global Metals or Flack Metal Bank should not be treated as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of his opinion. Views and forecasts expressed are as of date indicated, are subject to change without notice, may not come to be and do not represent a recommendation or offer of any particular security, strategy or investment. Strategies mentioned may not be suitable for you. You must make an independent decision regarding investments or strategies mentioned in this article. It is recommended you consider your own particular circumstances and seek the advice from a financial professional before taking action in financial markets.

Bradley Clark

Read more from Bradley Clark