SMU price ranges: Sheet and plate prices retreat from recent highs

Steel prices slipped again this week, with all five of SMU’s sheet and plate indices trending lower for the second week in a row.

Steel prices slipped again this week, with all five of SMU’s sheet and plate indices trending lower for the second week in a row.

Four out of every five steel buyers who responded to our latest market survey say domestic mills are unwilling to negotiate on new order spot pricing. Mills have shown little flexibility on pricing for nearly two months.

After a multi-week increase, buyers responding to our market survey this week reported that lead times are stabilizing or marginally declining for each of the sheet and plate products we track.

Steel prices were stable to higher this week for the second consecutive week across the sheet and plate products tracked by SMU. Three of our price indices increased from the previous week, while two held firm.

Steel prices climbed across the board this week, with every steel product tracked by SMU rising to multi-month highs.

Steel mill negotiation rates have declined in each of our last two surveys; this week’s rate is the lowest recorded since March 2024.

SMU’s steel price indices rose across the board this week. Sheet prices increased as much as $35 per short ton (st) compared to last week, while our average plate price ticked up by$10/st.

The majority of steel buyers we canvassed this week continue to report that mills are willing to negotiate prices on new spot orders, though not as much as they were in early-January.

Steel prices have remained relatively stable in recent weeks, though they have generally trended downward since October.

SMU's price indices saw minor fluctuations on sheet products this week, while our plate and Galvalume indices held steady.

SMU’s flat-rolled steel prices were mixed this week with slight declines across most products and a modest increase in prices for cold-rolled coil.

SMU price indices declined again this week for all products other than hot-rolled sheet. Our indices have trended lower across October, falling as much as $75 per short ton (st) in that time.

Three out of four of our market survey respondents report that steel mills are open to negotiating new order prices this week, a slight decline compared to our previous market check.

SMU’s sheet price was largely flat this week, an unusual sight for the better part of the past four months. The same trend was seen for tandem products and plate as well.

SMU’s sheet price ranges slid again this week. But the declines were more pronounced on tandem products whereas prices for hot-rolled coil held roughly steady.

Cleveland-Cliffs’ earnings tumbled in the second quarter as the company cited weak demand and pricing.

Sheet steel buyers continue to report that mills are willing to talk price on new orders, according to our most recent survey data collected this week.

Steel mill lead times remain short according to our latest market canvass of steel service center and manufacturer buyers. Of the sheet and plate products SMU tracks, production times for all materials are nearing historical lows not seen in months or years.

There are just 40 days left until the 2024 SMU Steel Summit gets underway on Aug. 26 at the Georgia International Convention Center (GICC) in Atlanta. And I’m pleased to announce that it's official now: More than 1,000 people have registered to at attend! Another big development: The desktop version of the networking app for the event has officially launched!

SMU’s hot-rolled coil price fell to $640 per short ton (st) on average on Tuesday. That’s down $10/st from last week and marks the lowest point for HR prices since December 2022, according to our pricing archives. SMU’s HR price is now $5/ton below 2023’s low of $645/st, which occurred against the backdrop of a United Auto Workers (UAW) union strike.

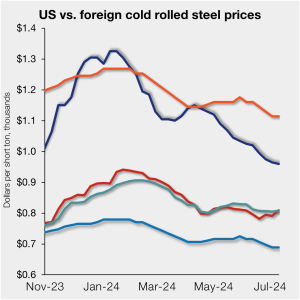

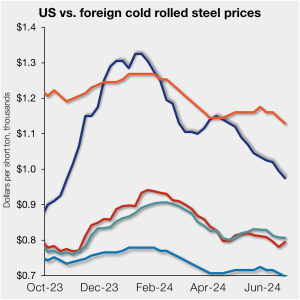

Offshore cold-rolled (CR) coil remains cheaper than domestic product. The gap continues to tighten, however, as US CR coil prices slip to a nine-month low. Domestic CR coil tags averaged $960 per short ton (st) in our check of the market on Tuesday, July 9, down $5/st from the week before. CR tags are now […]

We’ve taken some time to supply you with some handy-dandy production figures for 2024 presented in a unique way.

Flat-rolled steel prices have been largely falling since the beginning of the year. Even after a slight bump in early April when mills tried to halt the downtrend, the decrease resumed.

US sheet prices saw a similar pattern this week, customary for much of the year – new week, lower prices. Domestic tags moved lower this week, aligning with the typically slower summer period – but maybe a further indication of dwindling demand.

Following April’s eight-month high, May represents the second-lowest export rate of the year, only greater than January’s 771,000 st level.

Steel mill lead times remain near some of the lowest levels witnessed in months, according to our latest market canvass to steel service centers and manufacturers.

US sheet prices moved lower again this week, continuing a trend seen since early April. The slowdown aligns with the typical summer doldrums, when lax demand and shorter lead times often take center stage. The current market is also characterized by ample supply and concerns about restocking – especially with few signs of a bottom […]

Low global sheet demand continued to weigh on prices around the world this week. In the US, mills were forced to remain aggressive to secure orders during this period of demand weakness. And compounded by recent new capacity ramp-ups, has forced US hot rolled (HR) coil prices down closer to levels seen in offshore markets. […]

Offshore cold-rolled (CR) coil remains cheaper than domestic product pricing even as US CR coil prices slip to an eight-month low. Domestic CR coil tags stood at $975 per short ton (st) on average in our check of the market on Tuesday, June 25, down $20/st from the week before. Domestic CR prices are, on […]

Following a relatively stable first quarter, steel imports climbed in May to levels not seen in over two-years, according to preliminary Census data released earlier this week. Projected June license data suggests imports could ease from May, though still strong in comparison to levels witnessed over the past year.