SMU's November at a glance

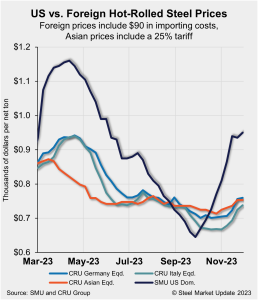

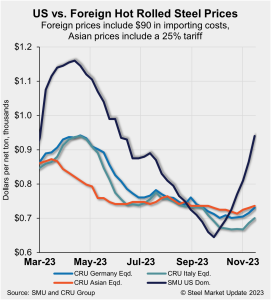

Steel prices continued to rally last month on the back of repeated mill price increases after tags reached a 2023 low of $645 per ton in late September. Hot-rolled coil (HRC) prices ended November at an average of $923 per ton ($46.15 per cwt), rising by $140 per ton during the month. The SMU Price […]