Analysis

November 28, 2023

Final thoughts

Written by Michael Cowden

I want to address a few things in this ‘Final thoughts’: the latest SMU survey results, the plate market, and the potential sale of U.S. Steel.

So, without further ado, here we go.

Steel Market Survey

The “right now” is what you would expect: Lead times continue to extend. Mills are not willing to negotiate lower sheet prices. (No shock with Nucor seeking $1,100 base for HRC.) Sentiment is bullish too.

But it’s a little murkier when it comes to 2024.

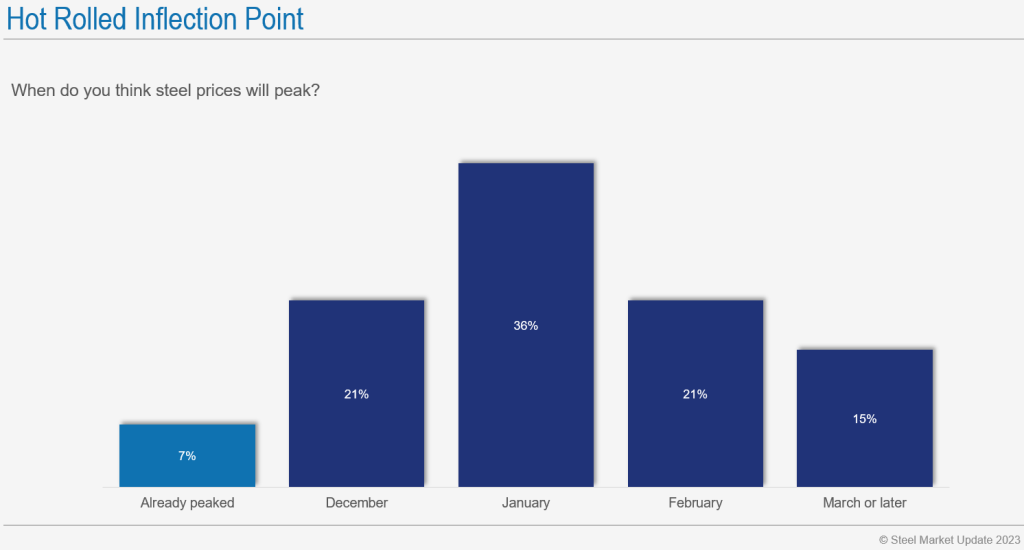

Check out the chart below. We asked people when they thought sheet prices would peak:

Thirty-six percent of survey respondents think sheet prices will peak in January, up from 21% in our last check of the market.

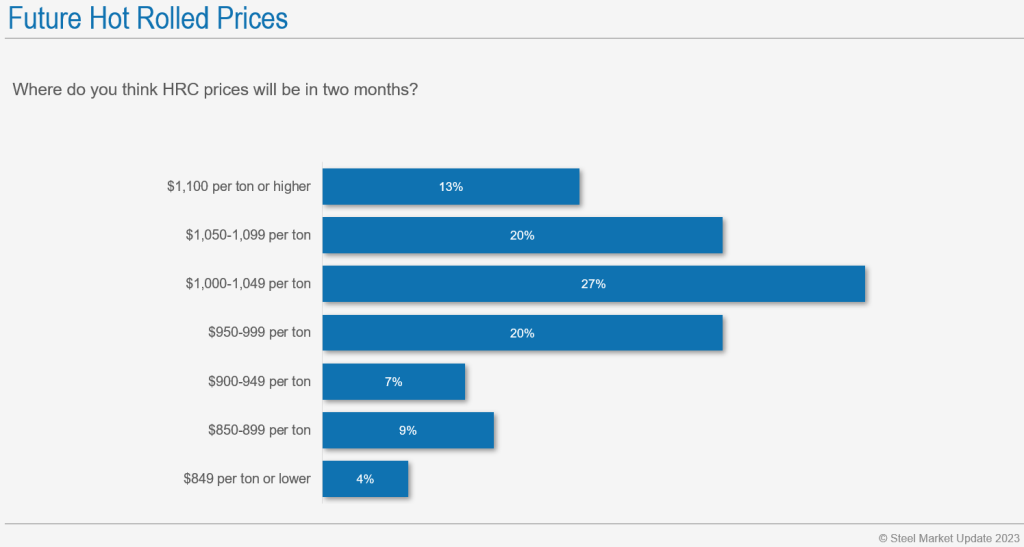

There is also more variation in this survey than in past ones as to where prices will be in two months:

While 13% think HRC will be at or above $1,100 two months from now – or what Nucor is seeking – an equal number think HRC prices will be below $900 per ton in late February.

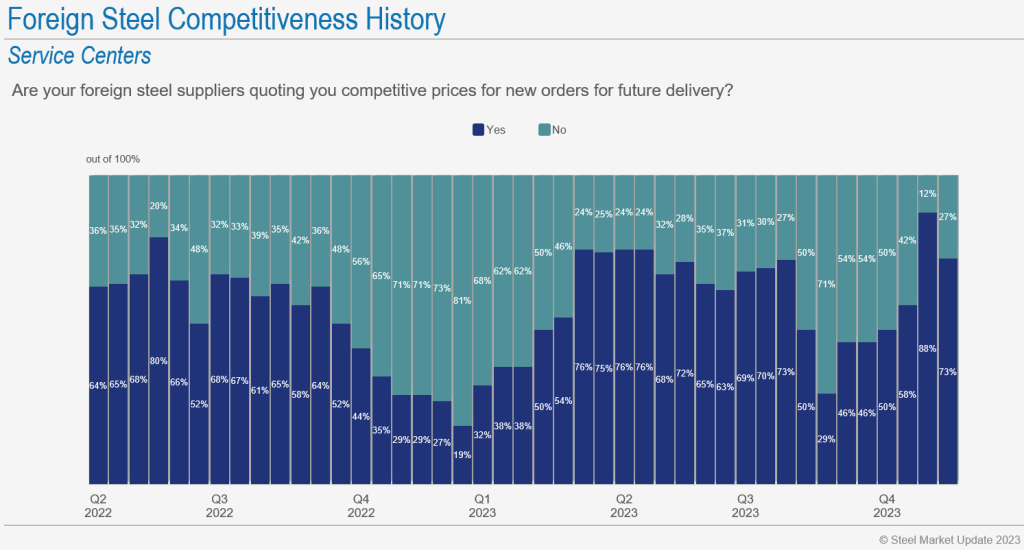

What gives? One theory: Could we see a significant increase in imports in 2024? I ask that because of the chart below:

Seventy-three percent of service center respondents say imports are competitive, up from 29% in late Q3 – when US sheet prices hit what will almost certainly prove to be a 2023 low.

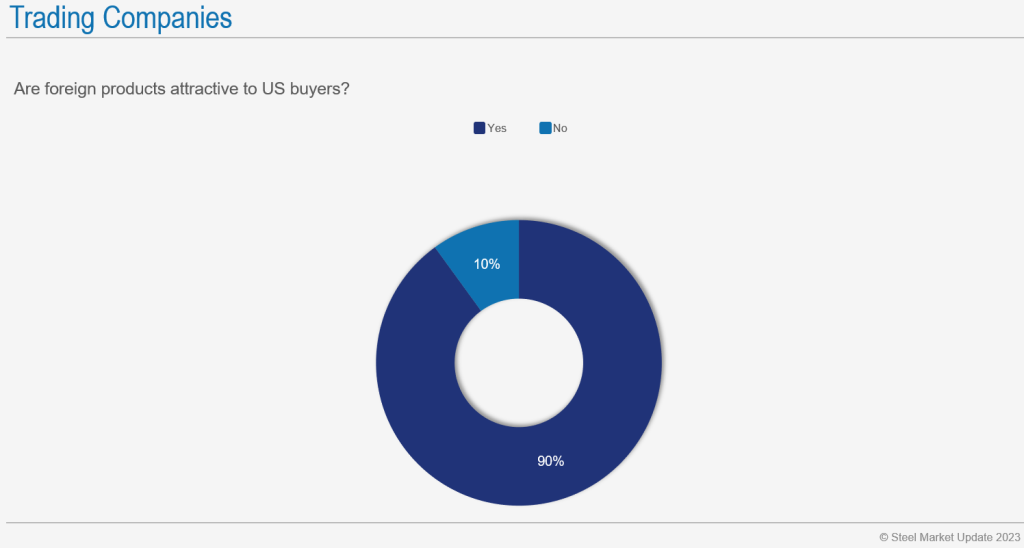

Also, 90% of trader respondents say foreign offers are attracting US buyers:

And I should note that the trend of imports being more attractive is not a recent one. If you want to dig deeper into our survey, go here. You’ll see the survey respondents thinks that foreign hot-rolled and coated products are among the most appealing items from a price standpoint.

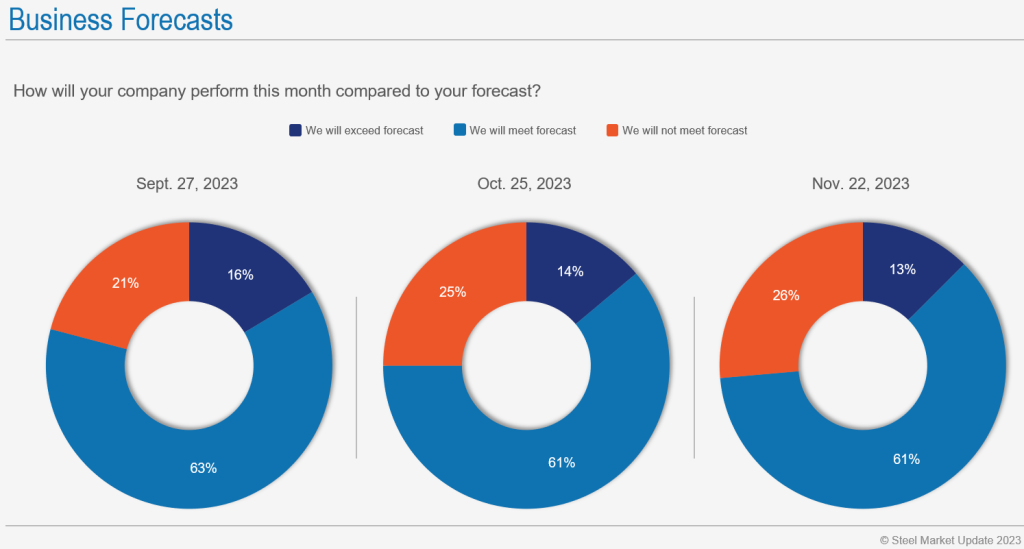

The good news? Demand remains on stable footing. It’s the sauce that makes all this uncertainty palatable:

Seventy-four percent of survey respondents say they will meet or exceed forecast in November – consistent with results we’ve seen since late September.

PS: Want to make sure your company’s experience is reflected in our survey results, contact us at info@steelmarketupdate.com to become a participant.

What’s up with plate?

Plate fell to $1,350 per ton on average this week. That seems like a very healthy number to me. I can remember when it fell into the $500s per ton in the early days of the pandemic. Still, it’s the lowest number for plate since May 2021.

I can also remember times when plate prices would fall below sheet prices. We haven’t seen that since early 2022, when plate eclipsed sheet, established a huge premium to it, and maintained that premium for the rest of 2022 and throughout 2023 to date.

HRC and plate used to move, broadly speaking, in tandem. Is there a fundamental reason why that relationship has changed? Or have the last roughly two years been an outlier? Nucor, for example, had cut plate prices while aggressively raising sheet prices. Will we see the relationship between sheet and plate move back to a more normal level?

I ask that partly because we’ve seen some big offshore wind projects delayed, scaled back, or cancelled in the US. Some of those had been expected to be an important new source of demand. Do the challenges in offshore wind pose a material challenge to plate as well?

I don’t have answers to some of those questions. But Algoma Steel CEO Michael Garcia should have good insights. He’ll be the guest speaker on our Community Chat on Wednesday at 11 am ET. It’s not too late to register!

U.S. Steel sale announcement close?

U.S. Steel announced on Tuesday that it was indefinitely idling “primary operations” at its Granite City Works near St. Louis. That was a surprise but not necessarily a shock.

The company announced an initial, temporary idling in September – the UAW strike, which was then ongoing – never rang true to some of you who noted that Granite City was not nearly as heavily tilted toward automotive as Gary Works in northwest Indiana.

Also, this is not the first time Granite City has been idled. Its furnaces were idled in December 2015 and its hot-strip mill in 2016. U.S. Steel at the time pinned the move on difficult market conditions, excess global capacity, and competition from imports. It then announced in March 2018, more than two years later, that it would restart a furnace at Granite City thanks to Section 232 tariffs.

What might happen this time around? And if the assets are restarted, whose ownership might they be under? I ask that because some of you have told me that the winning bidder (or bidders) for part or perhaps all of the iconic Pittsburgh-based steelmaker could be announced in the coming days.

When do the fireworks begin: Over the weekend? (Recall that the sale was initially and messily disclosed on a Sunday in August.) Early next week? Or are we getting too worked up about rumors?

As always, let me know your thoughts. And thanks to all of you from all of us at SMU for your continued business.