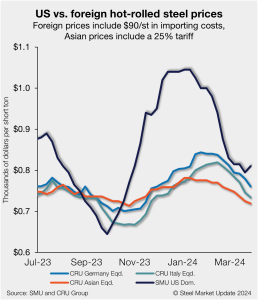

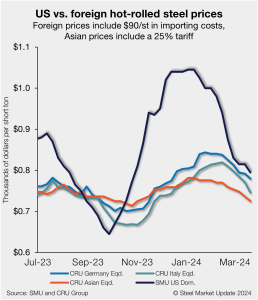

US HR prices rebound, no longer near parity with imports

US hot-rolled coil and offshore hot band moved further away from parity this week as stateside prices have begun to move higher in response to mill increases.

US hot-rolled coil and offshore hot band moved further away from parity this week as stateside prices have begun to move higher in response to mill increases.

Numerous mid-sized export yards in California and in Baja Mexico had little to no inventory on the ground last week because most had sold forward in the falling March market. Looking to secure their margins, they dropped prices across the scale. That resulted in lower-than-normal flows. “I’m sold out through mid-April and even longer if the flow doesn’t pick up” one yard owner said. That turned out to be the position of numerous West Coast suppliers.

I can’t really define “Bidenomics” because it is so filled with contradictions. It seems to aim to increase manufacturing output in the United States. But not all increases are created equal.

Metalformers are expecting business conditions to remain steady over the next few months, according to the March Business Conditions Report from the Precision Metalforming Association.

Galvanized buyers reported solid demand and balanced inventories this week and were anticipating the sheet price increase announced by Cleveland-Cliffs on Wednesday.

A container ship collided with the Francis Scott Key Bridge in Baltimore on March 26, causing it to collapse. This has blocked sea lanes into and out of Baltimore port, which is the largest source of US seaborne thermal coal exports. The port usually exports 1–1.5 million metric tons (mt) of thermal coal per month. It is uncertain when sea shipping will be restored. But it could be several weeks or more. There are coal export terminals in Virginia, though diversion to these ports would raise costs.

SMU’s sheet prices firmed up modestly this week, even as CME hot rolled futures declined. What gives? My channel checks suggest that demand remains stable and that buyers have returned to the market following new HR base prices announced by mills earlier this month. I’m looking forward to seeing whether lead times, which have stabilized, will start extending. SMU will have more to share on that front when we release updated lead time figures on Thursday. As for HR futures, what a reversal! As David Feldstein wrote last Thursday, bulls expected mill price increase announcements. And we briefly saw the May contract climb as high as ~$1,000 per short ton (st).

Sheet prices reversed course and moved higher this week, while plate priced remained flat, according to our latest canvas of the market.

Rio de Janeiro-based metals and mining conglomerate Vale could potentially build a new plant for the production of iron ore briquettes in the US.

With the help of a large government grant, SSAB may soon expand its operations in the US – including constructing a fossil-fuel-free green ironmaking facility in Mississippi.

Domestic raw steel production slipped for the second consecutive week, and is now at a seven-week low, according to the most recent data from the American Iron and Steel Institute (AISI).

Bull Moose Tube (BMT) CEO Tom Modrowski passed away suddenly and unexpectedly on March 18. BMT said current CFO John Krupinski has been named interim CFO and CEO.

Cleveland-Cliffs Inc. has plans to replace the blast furnace at its Middletown Works in Ohio with a direct-reduced iron (DRI) plant and two electric melting furnaces (EMFs).

There’s that concept from Adam Smith we all learn about in our Econ 101 classes: The Invisible Hand. A simple Google search will provide a refresh, but if memory serves I would classify it as something akin to “the market is magic” or “the market’s gonna market.” Today, obviously, we live in a mixed environment. There are a lot of hands out there, and they’re not too difficult to see. In this election year of 2024, one of the most visible hands out there probably belongs to the federal government.

World steel output slipped in February according to World Steel Association’s (worldsteel) latest monthly report. With the exception of January’s surge, monthly production levels have declined ten out of the past eleven months.

The LME 3-month aluminum price resumed moving lower on the morning of March 22 and was last seen trading at $2,290 per metric ton. The price was unable to break through an important resistance level at $2,300/mt on March 21. EGA to acquire European recycler Emirates Global Aluminium of the UAE has signed a binding […]

North American rig count activity declined this week, according to the latest data from Baker Hughes. The number of active rigs in the US eased from last week’s 6-month high, while Canadian activity continued to wind down.

Worthington Steel is taking a pause on M&A activity as it focuses on progressing its electrical steel expansions in Mexico and Canada.

Prices for pig iron in Brazil have increased despite efforts by US-based buyers to lower them.

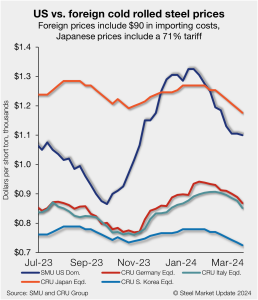

Foreign cold-rolled (CR) coil remains notably less expensive than domestic product even with repeated tag declines across all regions, according to SMU’s latest check of the market.

APAC steel prices are likely to bottom out in the near term as seasonally higher demand coupled with production cuts may support prices. In the EU, prices are likely to remain under pressure, while fresh price increases are expected in the US. APAC steel prices are likely to bottom out in the near term In […]

As the month of March goes into the second half, the scrap community is trying to cope with the large drop in ferrous scrap earlier this month.

With Earth Day almost a month away, the world’s attention often turns to the manufacturing sector with calls for greener production processes.

I’ve had questions from some of you lately about how we should think of the spread between hot-rolled (HR) coil prices and those for cold-rolled (CR) and coated product. Let’s assume that mills are intent on holding the line at least at $800 per short ton (st) for HR. The norm for HR-CR/coated spreads had been about $200 per short ton (st). That would suggest CR and coated base prices should be ~$1,000/st. Good luck finding anyone offering that.

US hot-rolled coil (HRC) remains more expensive than offshore hot band but continues to move closer to parity as prices decline further. The premium domestic product had over imports for roughly five months now remains near parity as tags abroad and stateside inch down.

SMU caught up with Barry Zekelman, executive chairman and CEO of Zekelman Industries, on Wednesday’s Community Chat. As one of the largest independent steel pipe and tube manufacturers in North America, his company is also one of the largest steel buyers in the region. This year alone, the Chicago-based company will buy roughly 2.8 million tons of steel. As such, Zekelman provides a great perspective on the steel industry and the markets it serves.

North American auto assemblies edged down in February vs. the prior month, according to LMC Automotive data. While assemblies did fall month on month (m/m), they are up nearly 3% year on year (y/y).

Varsteel, a Canadian steel and pipe service center, has announced the acquisition of Pacific Steel in Laval, Quebec.

Earlier this week SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to imports and evolving market chatter.

US light-vehicle (LV) sales rose to an unadjusted 1.25 million units in February, up 9.6% vs. year-ago levels, the US Bureau of Economic Analysis (BEA) reported. The year-on-year (y/y) growth in domestic LV sales was boosted by a 6% month on month (m/m) gain.