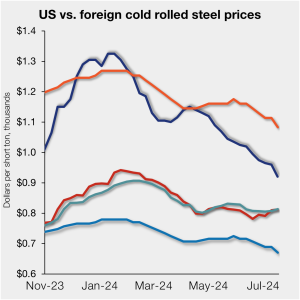

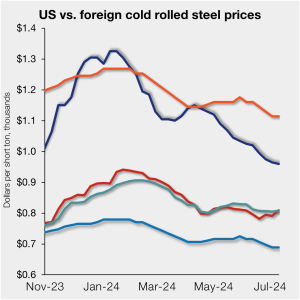

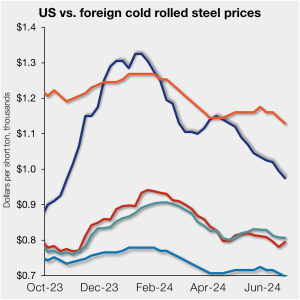

Final thoughts

They say a picture is worth a thousand words. Well, when you add in some commentary from respected peers in the steel industry to those pictures, that may shoot you up to five thousand words, at least. In that spirit, we’ve added some snapshots from our market survey this week, along with some comments from market participants.